Trading activity slowed notably today as the markets turned relatively quiet. Dollar attempted a rebound from its losses earlier this week but struggled to gain momentum after worse-than-expected PPI and jobless claims data. Despite being one of the weaker performers this week, Dollar has managed to stay above last week’s lows against all major currencies. The brief breakout against British Pound also quickly reversed, bringing Dollar back within its established range.

Japanese Yen has been the weakest performer this week. Attention now shifts to the upcoming BoJ monetary policy decision. While no changes in interest rates are anticipated, there is speculation that BoJ may begin tapering its monthly purchases of JGBs. Due to opposition from some BoJ board members, BoJ might only offer vague language about reduction in future bond buying rather than a detailed plan.

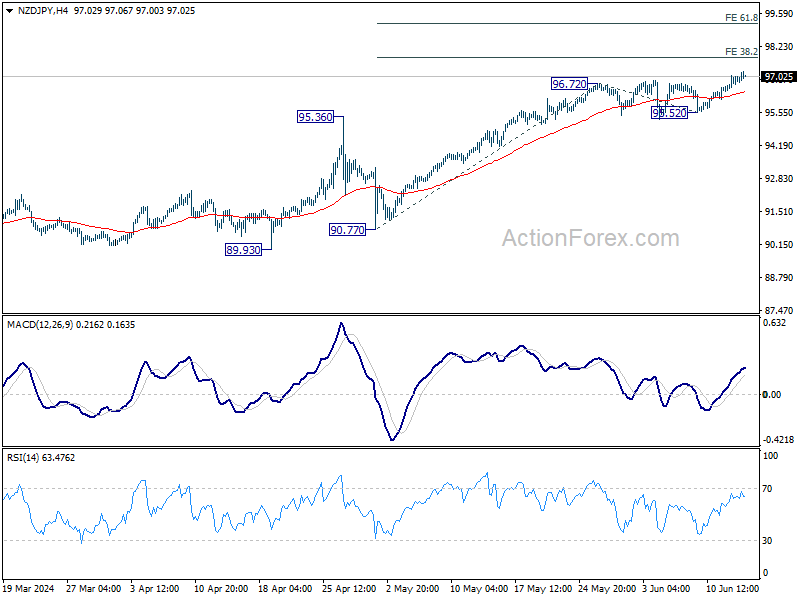

In the broader forex market, Euro is currently the third weakest performer. New Zealand Dollar continues to lead as the strongest currency, followed by Australian Dollar and British Pound. Swiss Franc and Canadian Dollar are positioned in the middle.

Technically, NZD/JPY’s up trend resumes this week and further rise is now expected to 38.2% projection of 90.77 to 96.72 from 95.52 at 97.79. Considering overall sluggishness in Yen’s decline, NZD/JPY’s upside could be capped by 97.79 on first attempt. Nevertheless, firm break there would pave the way to 61.8% projection at 99.19 next.

In Europe, at the time of writing, FTSE is down -0.36%. DAX is down -1.155%. CAC is down -1.25%. UK 10-year yield is up 0.0297 at 4.161. Germany 10-year yield is up 0.0008 at 2.532. Earlier in Asia, Nikkei fell -0.40%. Hong Kong HSI rose 0.97%. China Shanghai SSE fell -0.28%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield fell -0.0174 to 0.972.

US PPI at -0.2% mom, 2.2% yoy in May.

US PPI for final demand fell -0.2% mom in May, below expectation of 0.2% mom rise. PPI goods fell -0.8% mom, largest decline since October 2023. PPI energy fell -4.8% mom. PPI food fell -0.1% mom while PPI ex food and energy rose 0.3% mom. PPI services was unchanged. PPPI less foods, energy, and trade services was also unchanged.

For the 12-month period, PPI rose 2.2% yoy, matched expectations. final demand less foods, energy, and trade services rose 3.2% yoy.

US initial jobless claims jump to 242k, vs exp 227k

US initial jobless claims rose 13k to 242k in the week ending June 8, above expectation of 227k. Four-week moving average of initial claims rose 5k to 222k.

Continuing claims rose 30k to 1820k in the week ending June 1. Four-week moving average of continuing claims rose 8.5k to 1797k.

Eurozone industrial production down -0.1% mom in Apr, EU up 0.5% mom

Eurozone industrial production fell -0.1% mom in April, worse than expectation of 0.1% mom growth. Industrial production, decreased by -0.4% for intermediate goods. Production increased by by 0.4% for energy, 0.7% for capital goods, 0.3% for durable consumer goods, and 3.4% for non-durable consumer goods.

EU industrial production rose 0.5% mom. The highest monthly increases were recorded in Denmark (+10.4%), Greece (+7.0%) and Poland (+6.7%). The largest decreases were observed in Luxembourg (-6.7%), Latvia (-4.9%) and Ireland (-3.4%).

ECB’s Vasle: Further rate cuts possible this year if data remains favorable

ECB Governing Council member Bostjan Vasle has hinted at the possibility of further rate cuts this year, provided the baseline scenario holds and economic data supports such a move.

Speaking to Finance newspaper, Vasle said, “If the baseline scenario is realized and the data are favorable, then we can probably expect further rate cuts already this year, and then also next year.”

However, he cautioned that if the economic conditions are not as supportive, it would be prudent to “wait some more time with further steps.”

Vasle also highlighted several risks that could slow down the disinflation process, pointing to “relatively strong” momentum in wages, ongoing economic growth, and geopolitical uncertainties. These factors could impact the ECB’s decision-making process regarding future rate cuts.

Australia’s employment rises 39.7k, labor market remains relatively tight

Australia’s labor market demonstrated resilience in May, with employment increasing by 39.7k, slightly surpassing expectations of 39.0k. Full-time jobs saw a significant rise of 41.7k, while part-time jobs experienced a slight decline of -2.1k.

Unemployment rate decreased from 4.1% to 4.0%, aligning with market forecasts. Key labor metrics, such as the employment-to-population ratio and the participation rate, remained steady at 64.1% and 66.8%, respectively. However, monthly hours worked dipped by -0.5% on a month-over-month basis.

Bjorn Jarvis, ABS head of labor statistics, highlighted that the number of unemployed people, though nearing 600k, is still about 110k fewer than in March 2020, before the pandemic.

Additionally, both the employment-to-population ratio and participation rate are significantly higher than pre-pandemic levels. Jarvis pointed out that these factors, along with sustained high job vacancy levels, indicate that the labor market “remains relatively tight, though less so than in late 2022 and early 2023.”

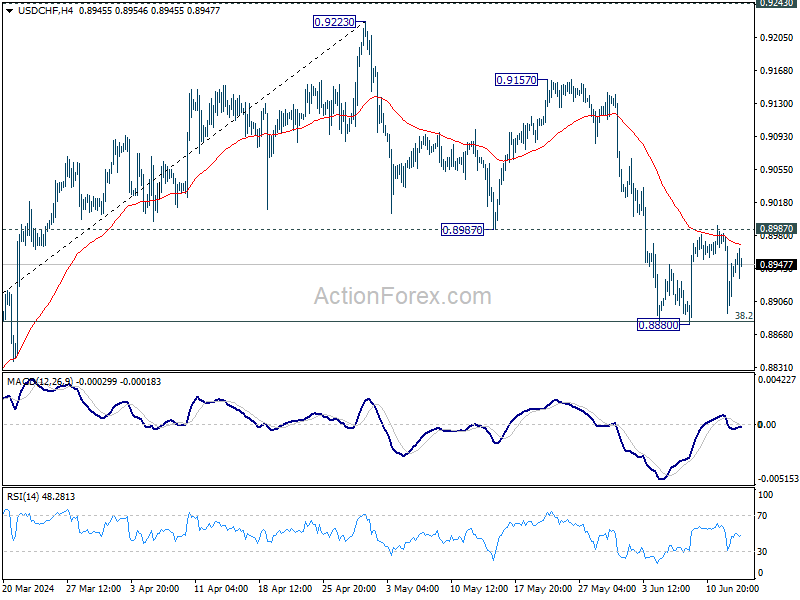

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8897; (P) 0.8940; (R1) 0.8988; More….

No change in USD/CHF’s outlook as range trading continues. Intraday bias remains neutral. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance May | -17% | -5% | -5% | -7% |

| 23:50 | JPY | BSI Large Manufacturing Index Q2 | -1 | -5.2 | -6.7 | |

| 01:30 | AUD | Employment Change May | 39.7K | 39.0K | 38.5K | 37.4K |

| 01:30 | AUD | Unemployment Rate May | 4.00% | 4.00% | 4.10% | |

| 06:30 | CHF | PPI M/M May | -0.30% | 0.50% | 0.60% | |

| 06:30 | CHF | PPI Y/Y May | -1.80% | -1.80% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | -0.10% | 0.10% | 0.60% | 0.50% |

| 12:30 | USD | PPI M/M May | -0.20% | 0.20% | 0.50% | |

| 12:30 | USD | PPI Y/Y May | 2.20% | 2.20% | 2.20% | 2.30% |

| 12:30 | USD | PPI Core M/M May | 0.00% | 0.30% | 0.50% | |

| 12:30 | USD | PPI Core Y/Y May | 2.30% | 2.30% | 2.40% | |

| 12:30 | USD | Initial Jobless Claims (Jun 7) | 242K | 227K | 229K | |

| 14:30 | USD | Natural Gas Storage | 75B | 98B |