While Dollar had a sharp decline following US consumer inflation data overnight, the selloff was short-lived. The greenback stabilized and recovered after FOMC projections indicated that only one rate cut is likely this year. Stock and bond markets showed little reaction to Fed’s announcement. Attention now turns to upcoming US PPI and jobless claims data for further market direction.

In the broader forex market, Japanese Yen remains the weakest currency of the week. BoJ’s policy decision tomorrow is unlikely to offer much support. However, Yen’s selloff is somewhat contained as traders remain cautious about risks of intervention. Dollar is the second weakest, followed by Euro, which continues to grapple with political instability in France and the EU.

On the other hand, New Zealand Dollar is the strongest performer this week. Australian Dollar is the second strongest, but showed little reaction to slightly better-than-expected employment data. British Pound ranks third, benefiting additionally from Euro’s weakness. Swiss Franc and Canadian Dollar are positioned in the middle.

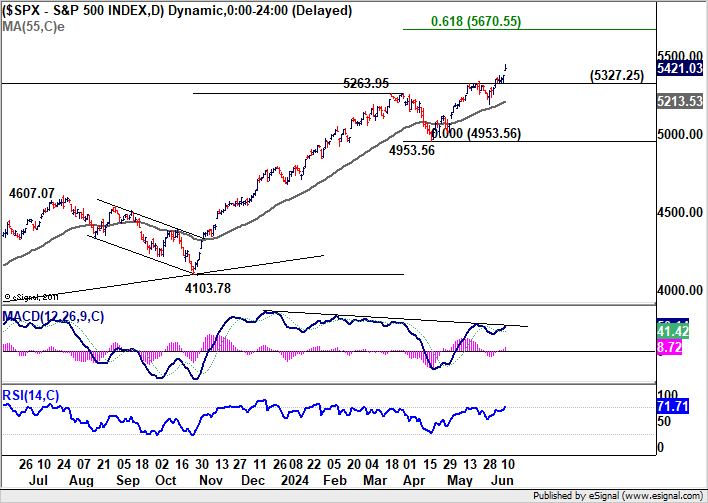

Technically, S&P 500’s up trend appears to be finally picking up momentum with yesterday’s post-CPI rise. Further rally is now expected as long as 5327.25 support holds. Next target is 61.8% projection of 4103.78 to 5263.95 from 4953.56 at 5670.55. On the downside, break of 5327.25 will bring consolidations first before staging another upmove.

In Asia, Nikkei fell -0.44%. Hong Kong HSI is up 0.40%. China Shanghai SSE is down -0.21%. Singapore Strait Times is up 0.54%. Japan 10-year JGB yield is down -0.0133 at 0.976. Overnight, DOW fell -0.09%. S&P 500 rose 0.85%. NASDAQ rose 1.53%. 10-year yield fell -0.109 to 4.295.

Fed’s balanced projections have something for both hawks and doves

S&P 500 and NASDAQ extended their record runs overnight, but that was mainly fueled by softer-than-expected May US CPI data. Market reaction to FOMC’s rate decision was indeed subdued, reflecting the balanced nature of the new economic projections and dot plot, which offered something for both hawks and doves.

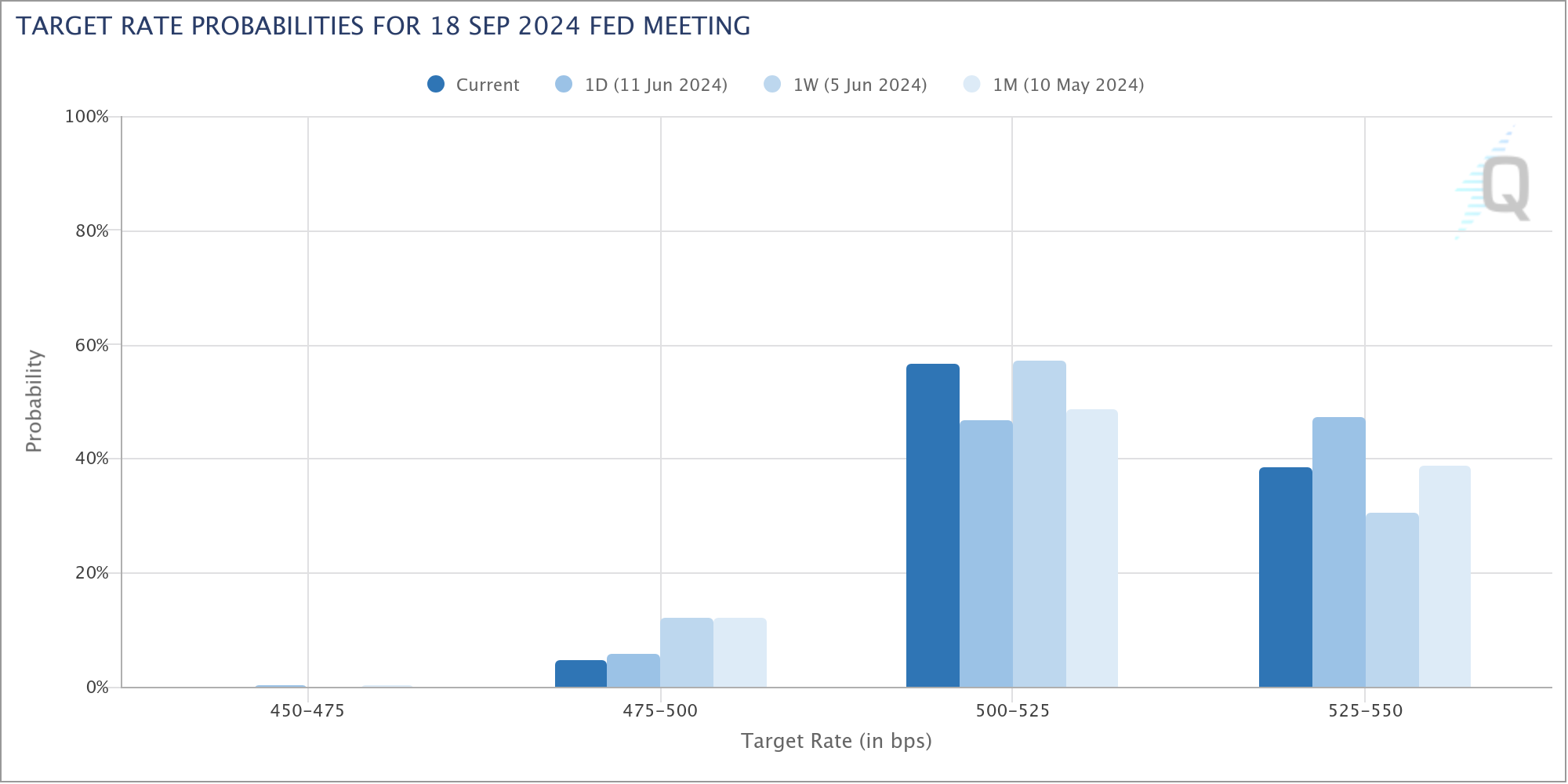

On the hawkish side, the median projection now indicates only one rate cut this year, a sharp shift from the three cuts anticipated back in March. The balance of the dot plot showed 11 members favoring one or no cuts versus 8 members advocating for two cuts, indicating a significant hurdle for those seeking more aggressive rate reductions.

Although some argue that not all FOMC members vote on policy decisions, potentially making the actual voting balance more dovish, it’s clear that Fed will require further encouraging inflation data, similar to the yesterday’s May CPI figures, before considering any policy easing.

Another hawkish signal was the increase in the long-run “neutral” rate from 2.6% to 2.8%. This rate has now risen by more than a quarter of a percentage point over Fed’s last two sets of projections. That suggests officials believe inflation will be more challenging to control in the future. However, Fed Chair Jerome Powell downplayed the significance of this increase, noting that it does not necessarily influence short-term rate projections.

On the dovish side, no FOMC members projected another rate hike, compared to two who had previously indicated the possibility of one more hike. This consensus suggests that all policymakers prefer to maintain the current interest rate level to combat inflation rather than tightening further, which should reassure most investors.

Going forward, Powell emphasized that Fed would make decisions based on the totality of incoming data rather than pre-determining future actions. He elaborated, “it’s going to be not just the inflation readings. It’s going to be the totality of the data, what’s happening in the labor market, what’s happening with the balance of risks, what’s happening with the forecasts, what’s happening with growth.”

Currently, Fed funds futures indicate a 61% chance of a rate cut in September, even lower than the 69% chance a week ago before the release of strong non-farm payroll data. The odds would likely continue to fluctuate in the current range until significant progress is seen in disinflation.

Australia’s employment rises 39.7k, labor market remains relatively tight

Australia’s labor market demonstrated resilience in May, with employment increasing by 39.7k, slightly surpassing expectations of 39.0k. Full-time jobs saw a significant rise of 41.7k, while part-time jobs experienced a slight decline of -2.1k.

Unemployment rate decreased from 4.1% to 4.0%, aligning with market forecasts. Key labor metrics, such as the employment-to-population ratio and the participation rate, remained steady at 64.1% and 66.8%, respectively. However, monthly hours worked dipped by -0.5% on a month-over-month basis.

Bjorn Jarvis, ABS head of labor statistics, highlighted that the number of unemployed people, though nearing 600k, is still about 110k fewer than in March 2020, before the pandemic.

Additionally, both the employment-to-population ratio and participation rate are significantly higher than pre-pandemic levels. Jarvis pointed out that these factors, along with sustained high job vacancy levels, indicate that the labor market “remains relatively tight, though less so than in late 2022 and early 2023.”

Looking ahead

Swiss PPI and Eurozone industrial production will be released in European session. Later in the day, US will publish PPI and jobless claims.

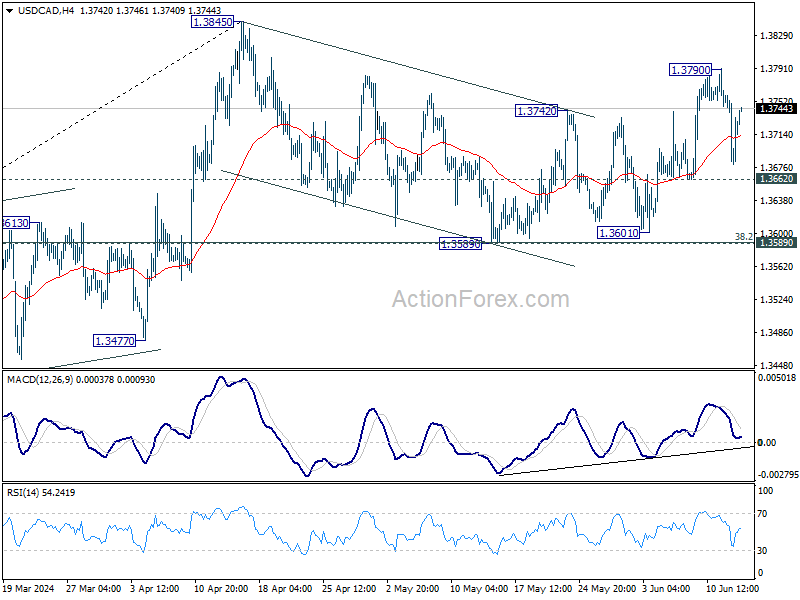

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3682; (P) 1.3722; (R1) 1.3764; More…

Despite steep retreat, USD/CAD recovered strongly ahead of 1.2662 support. Intraday bias stays neutral first. On the upside, above 1.3790 will resume the rebound from 1.3589 to retest 1.3845 high. Firm break there will resume larger rally. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

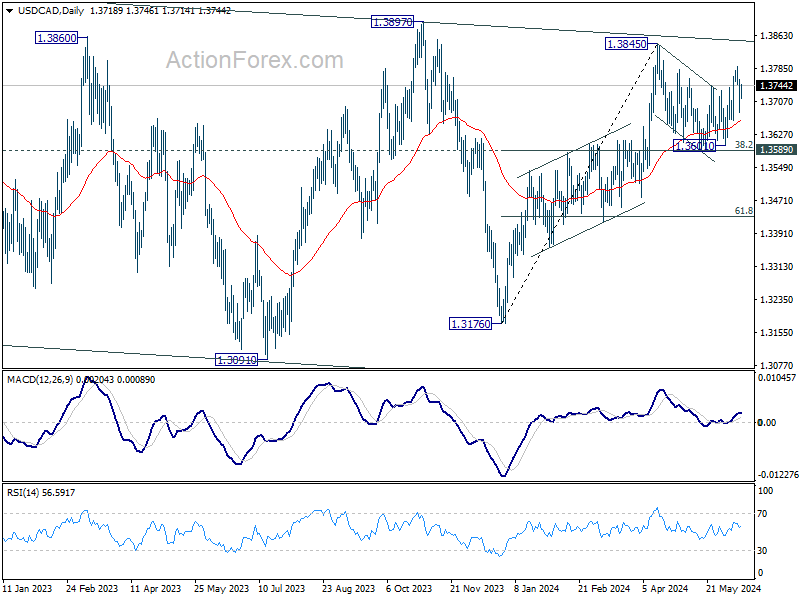

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance May | -17% | -5% | -5% | -7% |

| 23:50 | JPY | BSI Large Manufacturing Index Q2 | -1 | -5.2 | -6.7 | |

| 01:30 | AUD | Employment Change May | 39.7K | 39.0K | 38.5K | 37.4K |

| 01:30 | AUD | Unemployment Rate May | 4.00% | 4.00% | 4.10% | |

| 06:30 | CHF | PPI M/M May | 0.50% | 0.60% | ||

| 06:30 | CHF | PPI Y/Y May | -1.80% | |||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 0.10% | 0.60% | ||

| 12:30 | USD | PPI M/M May | 0.20% | 0.50% | ||

| 12:30 | USD | PPI Y/Y May | 2.20% | 2.20% | ||

| 12:30 | USD | PPI Core M/M May | 0.30% | 0.50% | ||

| 12:30 | USD | PPI Core Y/Y May | 2.30% | 2.40% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 7) | 227K | 229K | ||

| 14:30 | USD | Natural Gas Storage | 75B | 98B |