The forex markets are rather subdued in today’s Asian session, with major currency pairs and crosses largely trading within yesterday’s ranges. Australian Dollar strengthened slightly, ignoring significantly weaker-than-anticipated job data. Instead, it’s lifted by rebound in Asian stock markets and stabilizing risk sentiment. However, the momentum behind Aussie’s rebound appears weak and limited, suggesting it may be merely in consolidation before another selloff.

Central bank commentary from both Fed and ECB has been plentiful but has yet to significantly influence market movements. ECB is widely expected to implement a rate cut in June, aligning with previous communications. In contrast, Fed would maintain its policy stance for longer, as the disinflation process in the US has shown signs of slowing down, or even stalling this year, which precludes any immediate policy loosening.

As the week progresses, the Swiss Franc leads as the strongest currency, followed by Euro and Sterling. In contrast, Yen, Kiwi, and Aussie rank as the weaker performers. Dollar and Canadian Dollar hold middle ground. A the greenback is consolidating recent strong gains, European majors are currently displaying slight advantages over their commodity-linked counterparts, reflecting ongoing vulnerabilities in global risk sentiment.

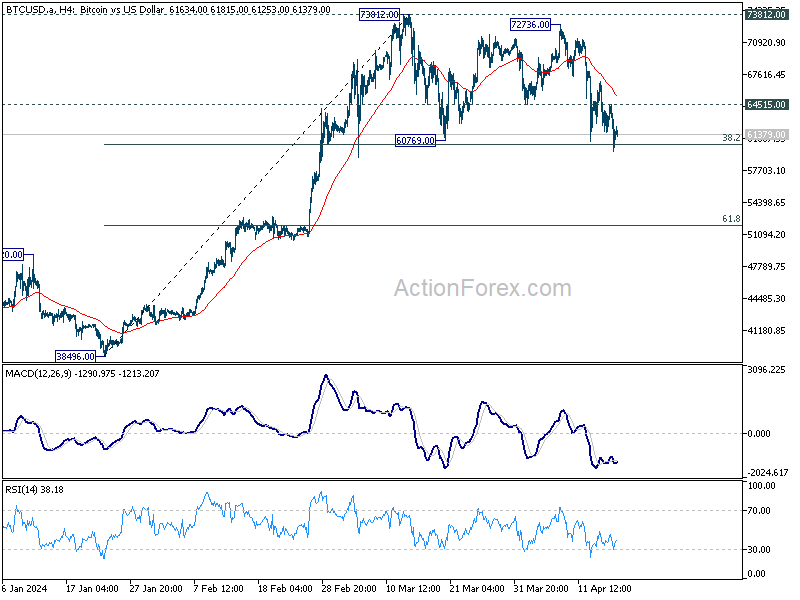

Technically, it’s probably about time Bitcoin completes its three wave sideway consolidation from 73812. Break of 64515 minor resistance will bring stronger rebound back to retest 73812 high next. Nevertheless, sustained break of 38.2% retracement of 38496 to 73812 at 60321 will bring deeper fall to 61.8% retracement at 51986 instead.

In Asia, at the time of writing, Nikkei is up 0.63%. Hong Kong HSI is up 0.89%. China Shanghai SSE is up 0.14%. Singapore Strait Times is up 1.23%. Overnight, DOW fell -0.12%. S&P 500 fell -0.58%. NASDAQ fell -1.15%. 10-year yield fell -0.074 to 4.585.

BoE’s Bailey anticipates sharp decline in inflation, stresses need for balance

BoE Governor Andrew Bailey, speaking at an International Institute of Finance conference, projected a “quite a strong drop” in next month’s inflation figures. This expectation is largely due to the unique household energy pricing system in the UK, which is set to impact the overall inflation calculations differently compared to other sectors.

However, he was quick to temper this optimistic forecast with a note of caution regarding the broader inflationary landscape. According to Bailey, underlying components of the inflation measure continue to show disparities that could complicate monetary policy response.

The Governor pointed out that while energy price inflation is currently running at minus 20%, the inflation in services remains high, around 6%. This stark contrast in inflation rates across different sectors presents an “unbalanced” picture.

“We don’t have to have every component actually at target, but you do have to have a better balance,” Bailey remarked.

ECB officials signal growing likelihood of rate cut in Jun

ECB officials have indicated a growing likelihood of a rate cut as soon as June, though decisions hinge on forthcoming economic projections and persistent inflation concerns.

Bundesbank President and ECB Governing Council member Joachim Nagel voiced cautious optimism to CNBC about the possibility of easing monetary policy, noting, “the probability is increasing” for a rate reduction, albeit with “some caveats” due to still-high core and service inflation rates.

Nagel emphasized that ECB’s upcoming projections in June will be crucial. “For the June meeting, we will get our projections, so we will get our new forecasts and if there is a confirmation that inflation is really going down and we will achieve our target in 2025,” he explained.

In tandem, Mario Centeno, Governor of the Bank of Portugal and fellow ECB Governing Council member, described a rate cut in June as “very likely,” asserting that even with a reduction of 25 or 50 basis the ECB’s monetary policy would remain tight.

Slovenia’s central bank governor Bostjan Vasle projected that interest rates should be “much closer to 3% towards the end of the year if everything goes according to plan.” However, he also expressed concern over recent geopolitical tensions in the Middle East.

Fed’s Bowman: Inflation progress has slowed, perhaps even stalled

Fed Governor Michelle Bowman, speaking at an International Institute of Finance conference, remarked that progress on inflation has “slowed” and may have “even stalled at this point”.

Bowman elaborated that the existing levels of growth and market activity might indicate that the current policy stance may not be restrictive enough. “There is a lot of financial market activity and a lot of continued growth that we wouldn’t have expected if policy was sufficiently tight,” she commented, adding, “I think it is restrictive. I think time will tell whether it is sufficiently restrictive.”

Separately, Cleveland Fed President Loretta Mester also echoed the need for caution before making further policy adjustments. While she remains hopeful that inflation will decrease, Mester emphasized the importance of further data analysis before proceeding with any monetary policy changes. “I still am expecting inflation to come down but I do think that we need to be watching and gathering more information before we take an action,” Mester commented.

BoJ’s Noguchi: Poicy rate adjustment expected to be slow

BoJ Board Member Asahi Noguchi highlighted in a speech today the unique economic conditions facing Japan compared to other major economies. He pointed out that any changes to the policy rate are expected to occur at a slower pace than those seen in recent actions by other major central banks.

“With regard to the pace of policy rate adjustment, it is expected to be slow, at a pace that cannot be compared to that of other major central banks in recent years,” Noguchi stated. This approach reflects the central bank’s assessment that it will take considerable time for Japan to consistently achieve its price stability target of 2% inflation.

Noguchi also noted the recent significant wage increases in Japan, describing them as unprecedented. However, he cautioned that these wage hikes alone are not yet sufficient to drive up prices to the level needed for trend inflation to stabilize at the 2% target.

“It is essential for the BoJ to maintain its ultra-loose monetary policy to seek an appropriate balance in the labour supply-demand,” he added.

Australia’s employment contracts -6.6k in Mar, labor market still relatively tight

Australia’s employment figures for March revealed a slight contraction of -6.6k, worse than expectation of 7.2k growth. This downturn was primarily due to drop in part-time employment by -34.5k, partially offset by rise in full-time by 27.9k.

Unemployment rate rose from 3.7% to 3.8%, below expectation of 3.9%. Participation rate fell from 66.7% to 66.6%. Monthly hours worked rose 0.9% mom.

Bjorn Jarvis, Head of Labour Statistics at ABS, noted, “The labour market remained relatively tight in March, with an employment-to-population ratio and participation rate still close to their record highs in November 2023.” He pointed out that although there has been a modest decline of 0.4 percentage points since the highs of last November, the metrics remain substantially above pre-pandemic levels.

Australia NAB business confidence rises to -2 in Q1, cost pressures ease slightly

Australia NAB Quarterly Business Confidence rose from -6 to -2 in Q1. Business Conditions was unchanged at 10. In terms of forward-looking expectations, businesses anticipate a slight downturn in conditions over the next three months, with expectations dipping from 14 to 12. However, the outlook for the next 12 months improved, rising from 16 to 17.

According to NAB Chief Economist Alan Oster, “Consistent with our monthly business survey, today’s release shows business conditions remained resilient at above-average levels through the start of the year. Confidence remained weak but showed some improvement relative to the tail end of 2023.”

The report also highlighted easing cost pressures, although the reduction was minimal. Labor costs grew at a slightly reduced rate of 1.2%, down from 1.3% in the previous quarter, and purchase costs increased by 1.1%, down from 1.2%. Meanwhile, final product price growth remained steady at 0.7%, and retail price growth decreased marginally to 0.8% from 0.9%.

Oster noted, “There continue to be some positive signs of easing cost pressures for businesses but progress was more incremental through Q1. Importantly, forward-looking indicators of firms’ expectations for price growth suggest firms expect some further moderation.”

Looking ahead

Swiss trade balance and Eurozone current account will be released in European session. Later in the day, US will release jobless claims, Philly Fed survey, existing home sales, and leading index.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6407; (P) 0.6427; (R1) 0.6454; More…

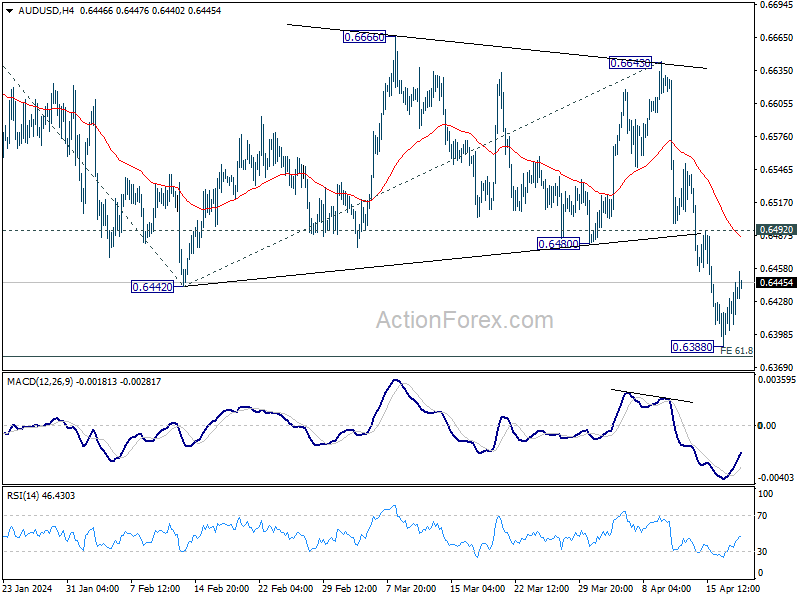

A temporary low is formed at 0.6388 in AUD/USD with current recovery and some consolidations would be seen. But upside should be limited by 0.6492 minor resistance. Below 0.6388 should resume larger fall from 0.6870 through 61.8% projection of 0.6870 to 0.6442 from 0.6643 at 0.6378 to 100% projection at 0.6215.

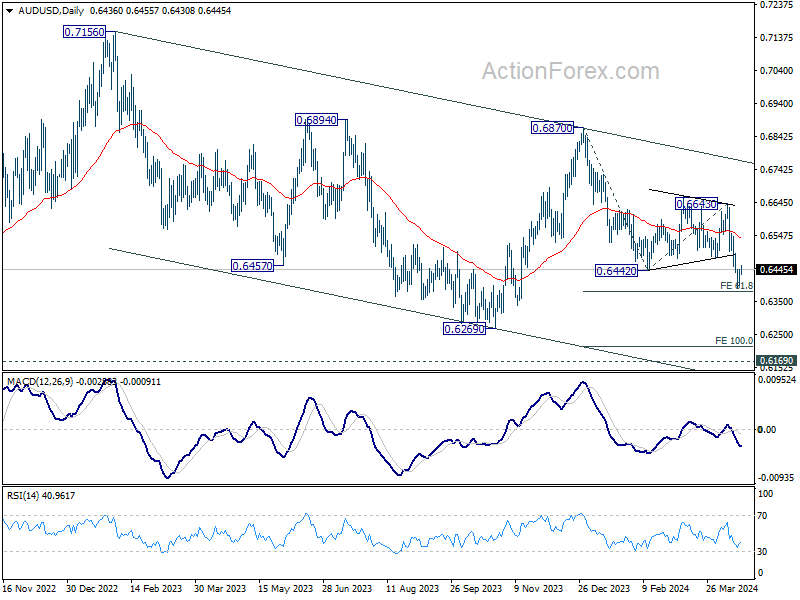

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | NAB Business Confidence Q1 | -2 | -6 | ||

| 01:30 | AUD | Employment Change Mar | -6.6K | 7.2K | 116.5K | 117.6K |

| 01:30 | AUD | Unemployment Rate Mar | 3.80% | 3.90% | 3.70% | |

| 01:30 | AUD | RBA Bulletin Q1 | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 1.50% | 0.80% | 0.30% | -0.50% |

| 06:00 | CHF | Trade Balance (CHF) Mar | 3.22B | 3.66B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Feb | 45.2B | 39.4B | ||

| 12:30 | USD | Initial Jobless Claims (Apr 12) | 214K | 211K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 0.8 | 3.2 | ||

| 14:00 | USD | Existing Home Sales Mar | 4.20M | 4.38M | ||

| 14:30 | USD | Natural Gas Storage | 54B | 24B |