The financial markets were jolted last week by data confirming the stall in disinflation progress in the US. This development prompted traders to quickly revise their expectations regarding Fed’s monetary policy, withdrawing bets on a June rate reduction. This shift in sentiment led to strong rise in treasury yields and corresponding deep decline in stock markets, reflecting heightened investor caution and risk aversion.

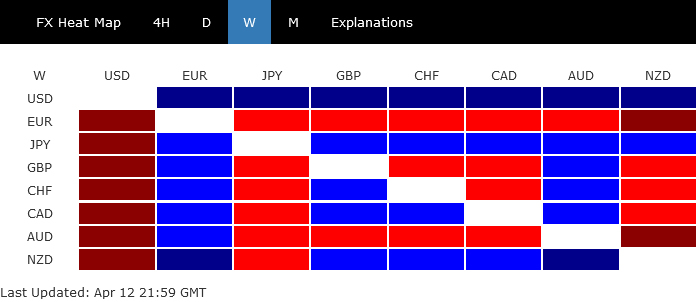

In the currency markets, Dollar was the primary beneficiary of these shifts, as it capitalized on the confluence set bullish factors including Fed rate expectations, rally in treasury yields, and a broad movement toward risk aversion. These factors collectively propelled Dollar to finish the week as the runaway winner.

There is ample room for last week’s movements in the stocks, bonds, and Dollar to continue. Recent bull runs in industrial metals and oil prices are likely the make the last mile of disinflation even harder. Increasing geopolitical tensions in the Middle East is another wild card that could further sink market sentiments.

In the broader currency markets, Euro ended the week as the weakest performer, as it encountered additional downward pressure due to late selloff against Swiss Franc and Sterling. The Australian Dollar also struggled, ranking as the second weakest currency, dragged down by its underperformance against other commodity-linked currencies.

Persistent Inflation Adjusts Fed Rate Cut Expectations, Shaking US Stock Markets

The markets seemed to have abandoned hope for a June rate cut by Fed after stronger than expected March US CPI data. Core CPI unchanged from February’s reading at 3.8%. More importantly, it was down just marginally from 4.1% six months ago. The decline in core inflation has been very gradual, and clearly, the path to 2% inflation is not assured.

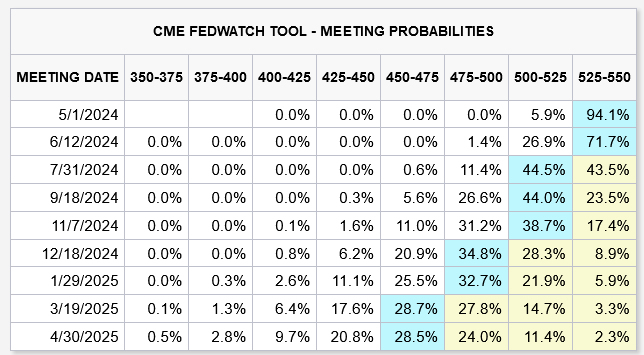

Fed fund futures now reflect a recalibrated outlook, with the probability of a rate cut in September falling to 76.5%. The prospects for more aggressive monetary easing within the year have also diminished, evidenced by only a 62.8% chance of a cumulative 50 basis points cut by year’s end. This more conservative forecast suggests that while the market still largely anticipates one rate cut from Fed in 2024, the possibility of a second cut is now viewed with greater skepticism.

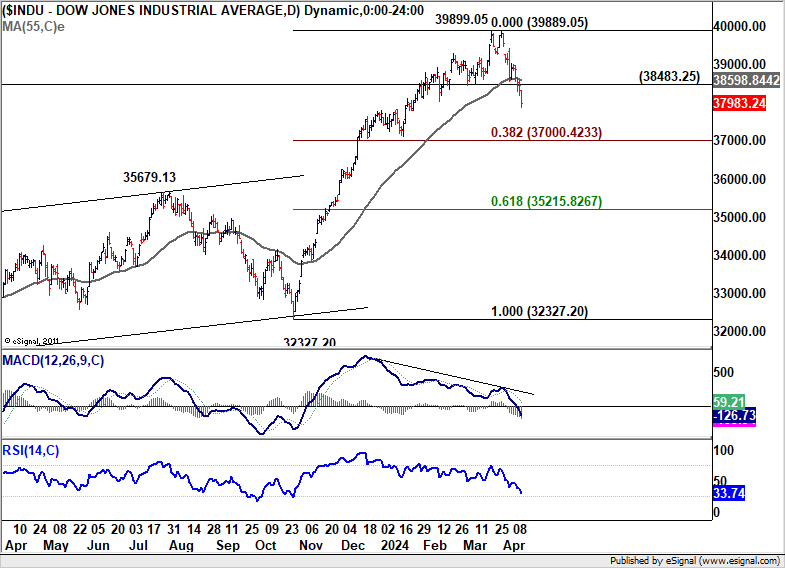

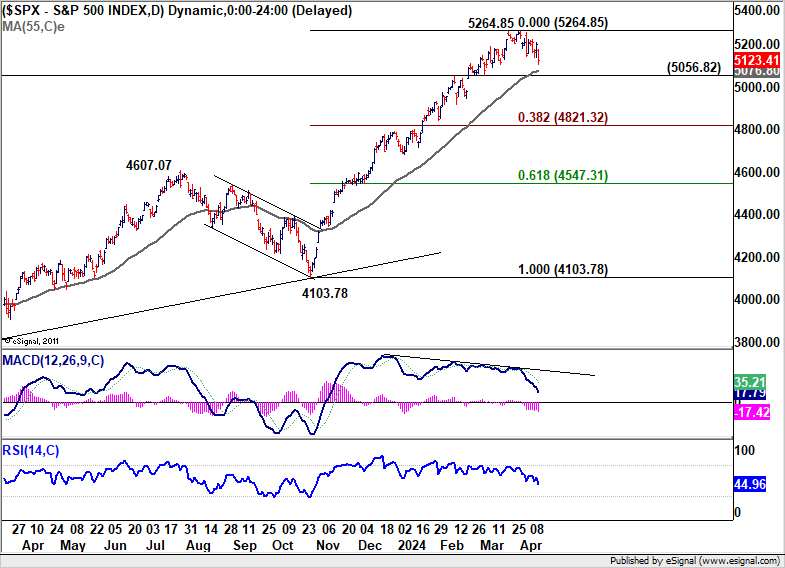

The market’s reaction to these adjusted expectations was stark, particularly in the equity sectors. Dow Jones Industrial Average bore the brunt of the downturn, plunging by -2.37% over the week. Similarly, S&P 500 and NASDAQ declined -1.56% and -0.45%, respectively.

Technically, DOW’s fall from 39889.05 is now seen as a correction to the rally from 32327.20. Deeper fall should be seen to 38.2% retracement of 32327.20 to 39899.05 at 37000.42. Strong support is expected there, at least on first attempt, to bring rebound. Meanwhile, firm break of 55 D EMA (now at 38598.84) will argue that the range of the corrective pattern could have been set already.

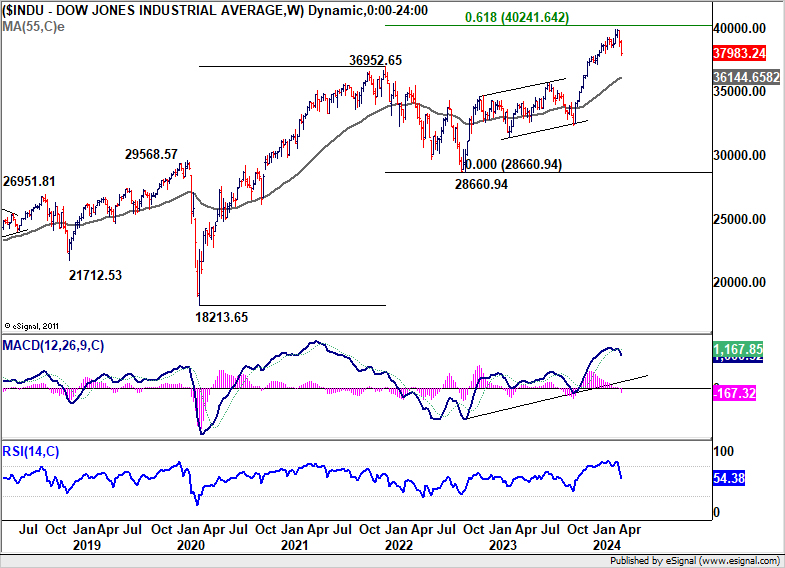

However, strong break of 37000.42 will put the second line of defense at 55 W EMA (now at 36144.65) in focus, and raise the chance of a larger correction to the up trend from 28660.94, which is currently seen as a less likely scenario.

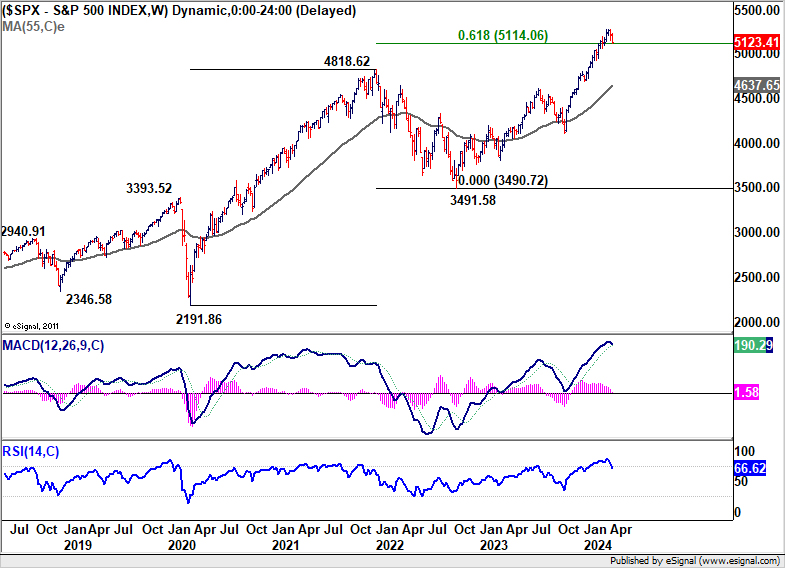

S&P 500 has been relatively more resilient, but it’s also starting to look vulnerable. Break of 5056.82 support and sustained trading below 55 D EMA (now at 5076.80) will align the outlook with DOW, and confirm each other’s. In this case, deeper fall would be seen to 38.2% retracement of 4103.78 to 5264.85 at 4821.32.

Surge in 10-Year Yield and Dollar Index

10-year yield surged sharply too to close at 4.499 after reaching as high as 4.591. There is no change in the outlook that rebound from 3.780 is the second leg of the corrective pattern from 4.990 (2023 high). The stronger than expected rise reflected the shift in market expectations for a less aggressive Fed policy easing cycle.

For now, the focus is on whether 10-year yield could sustain above 61.8% retracement of 4.997 to 3.785 at 4.534. If it does, further rally would then be seen to retest 4.997, which could be in expectation that Fed might not cut interest rates this year. Meanwhile, break of 4.307 support will indicate that 10-year yield has topped, at least for the near term.

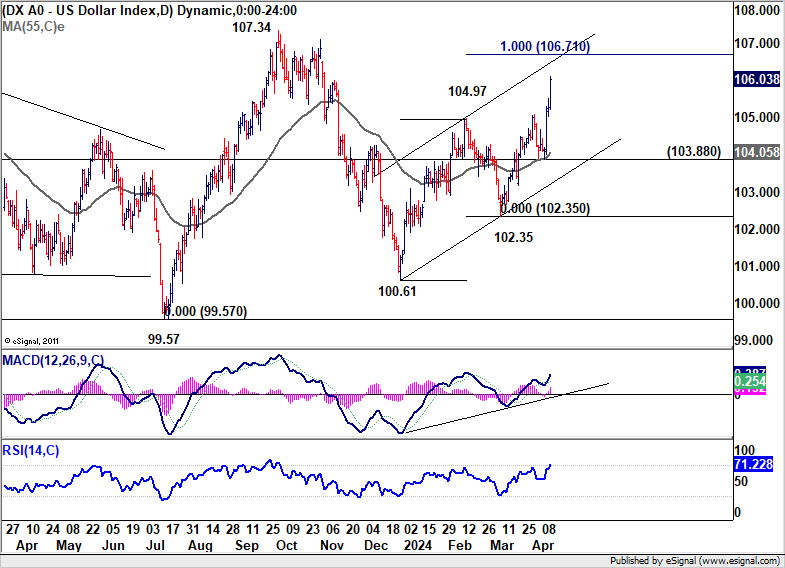

Dollar index’s rally resumed after drawing support from 55 EMA and surged to close at 106.03. Current rise from 100.61 is in progress for 100% projection of 100.61 to 104.97 from 102.35 at 106.71.

Price actions from 99.57 is currently seen as a corrective pattern with rise from 100.61 as the third leg. Break of 107.34 resistance could be seen. But upside would likely be capped by 100% projection of 99.57 to 107.34 from 100.61 at 108.38.

Euro May Begin to Falter Against Sterling and Franc

Euro is starting to appear vulnerable against its European counterparts, Swiss Franc and more so Sterling, following ECB latest communications that hinted strongly at forthcoming rate cut.

To be specific ECB articulated that, “If the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation, and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.”

ECB President Christine Lagarde emphasized the significance of this new sentence in the post meeting press conference, describing it as a “loud and clear indication” of ECB’s stance.

While the SNB has already initiated rate cut in March with another possibly on horizon in June, its policy rate at 1.50% offers related limited scope for further reductions compared to ECB’s deposit rate at 4.00%. Meanwhile, expectations for BoE have been adjusted, with market bets scaling back to two rate cuts this year, starting in September.

Technically, with last week’s steep pullback, EUR/CHF should have formed a short term top at 0.9847. Risk is mildly on the downside in the near term for 38.2% retracement of 0.9252 to 0.9847 at 0.9620. But strong support is expected from there to contain downside to bring rebound, and set the range for sideway trading.

EUR/CHF’s rally from 0.9252 would be ready to resume once clarity is obtained regarding the terminal rates of ECB and SNB in their easing cycles, given the significant interest rate disparity that is likely to persist. Bearish trend reversal in EUR/CHF is not expected unless significant geopolitical risks materialize, prompting massive safe-haven flow into Franc.

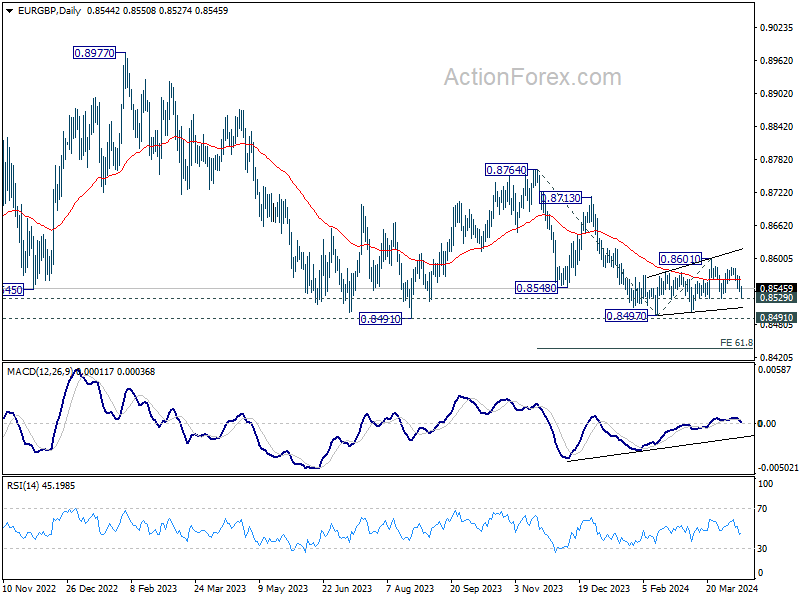

EUR/GBP might now be on the verge of resuming its medium term down trend. Break of 0.8529 support should prompt deeper decline through 0.8491/7 support zone. Next target will be 61.8% projection of 0.8764 to 0.8497 from 0.8601 at 0.8436. The downside breakout could be catalyzed by incoming data indicating that BoE is on track for only two rate cuts this year, or fewer.

Kiwi Leads Among Commodity Currencies, Aussie Lags

New Zealand Dollar ended as the stronger one among commodity currencies, bolstered by RBNZ’s decisively hawkish stance. After leaving OCR unchanged at 5.50%, RBNZ expressed “limited tolerance” for delay in bringing down inflation to target band. This clear commitment to combating inflation has reinforced expectations that RBNZ might not be ready to cut interest rates this year yet.

Meanwhile, Canadian Dollar found some relief as BoC refrained from dropping any explicit hints about a rate cut in June, contrary to what some market participants had anticipated. Australian Dollar, meanwhile, showed less enthusiastic response to the extended rise in metal prices. Despite Aussie’s recent rally seems to have exhausted its momentum, with increased risks of a downturn against its commodity currency counterparts.

Technically, AUD/NZD’s decline last week, with D MACD firmly crossed below signal line, indicates short term topping at 1.0952. Further break of 1.0860 support should confirm rejection by medium term falling trend line resistance and target 55 D EMA (now at 1.0803). Sustained trading below this EMA will indicate that the sideway pattern from 1.1085 has already started another falling leg back towards 1.0567 support.

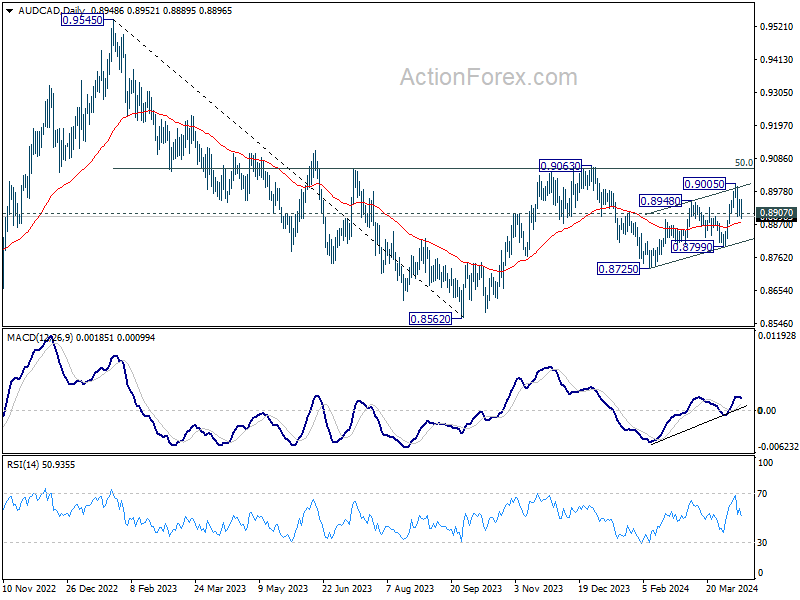

AUD/CAD’s break of 0.8907 support argues that corrective rebound from 0.8725 might have completed with three waves up to 0.9005. Sustained trading below 55 D EMA (now at 0.8878) will solidify this bearish case. Deeper decline should then be seen through 0.8725 support to resume the fall from 0.9063.

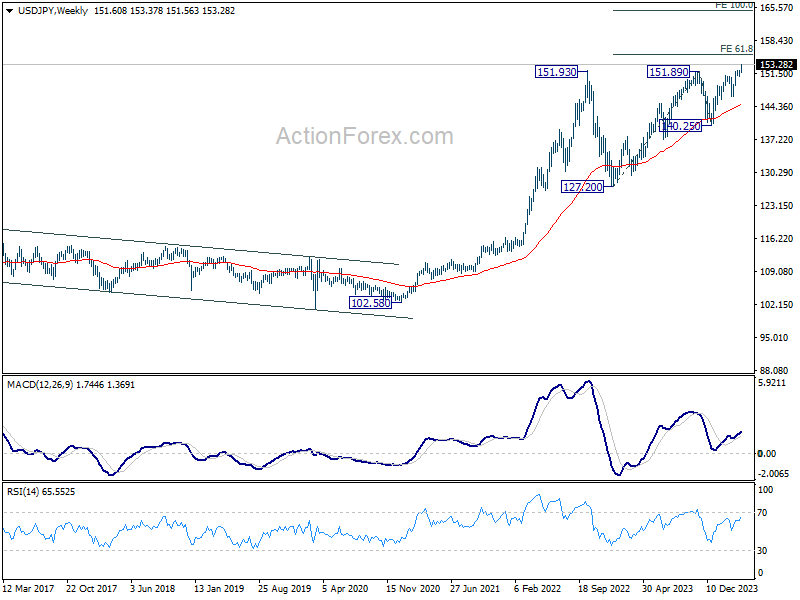

USD/JPY Weekly Outlook

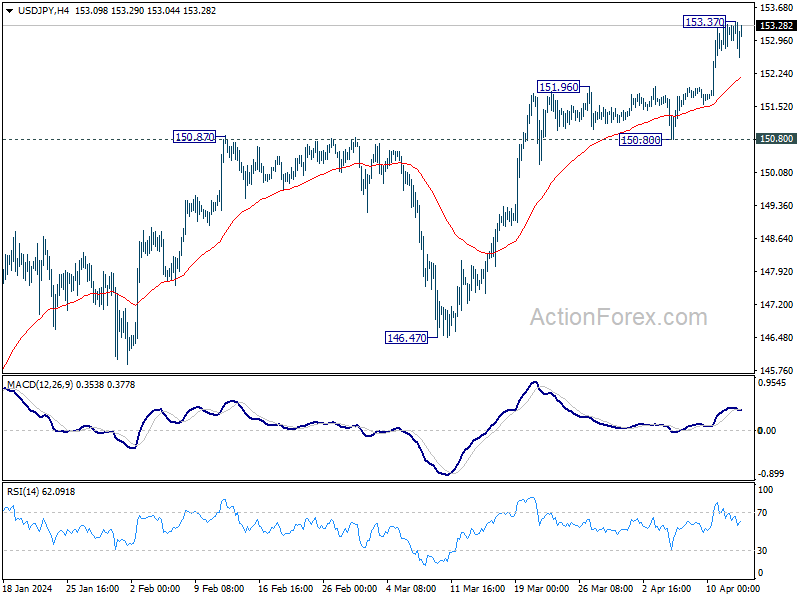

USD/JPY’s up trend resumed last week by breaking through 151.93 resistance. But it retreated after hitting 153.37. Initial bias is neutral this week for some consolidations first. Outlook will stay bullish as long as 150.80 support holds. Above 153.37 will target 155.20 fibonacci projection level next.

In the bigger picture, current rise from 140.25 is seen as the third leg of the up trend from 127.20 (2023 low). Next target is 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. Outlook will now remain bullish as long as 146.47 support holds, even in case of deep pullback.

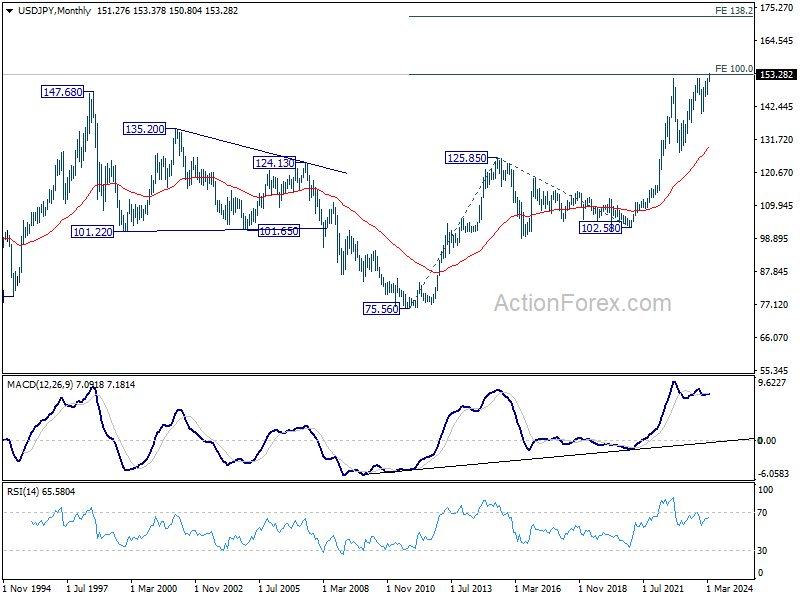

In the long term picture, as long as 127.20 support holds (2023 low), up trend from 75.56 (2011 low) is still in progress. Sustained trading above 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 102.58 at 152.87 will pave the way to 138.2% projection at 172.08. (This is a pure technical view without considering Japan’s intervention.)