The global markets today are abuzz with the rapid rise of US benchmark treasury yields. Market pundits are keeping a keen eye on 10-year yield, which, given its present momentum, is poised to touch 5% level. All eyes will also be on how traders react at this critical psychological level. Simultaneously, anticipation is building around Fed Chair Jerome Powell’s forthcoming speech at the Economic Club of New York. It’s widely expected that he will reiterate the stance on maintaining “higher for longer” interest rates in response to inflationary pressures. However, it’s crucial to understand that this ascent in yields isn’t restricted to the US alone. Germany’s 10-year yield has climbed to levels not seen since 2011, while Japan’s 10-year JGB yield has touched its highest point since 2013.

In the realm of currency markets, Australian Dollar and New Zealand Dollar are bearing the brunt of market shifts, emerging as the day’s weakest performers. While disappointing employment figures are an added burden for Aussie, Kiwi remains under the shadow of yesterday’s CPI revelations. British Pound is also under duress, particularly against Euro and Swiss Franc, placing it as the day’s third weakest currency. On the other end of the spectrum, Yen, Franc, and Euro are vying for the top positions, with Dollar lagging slightly behind, struggling to keep up the pace with 10-year yield.

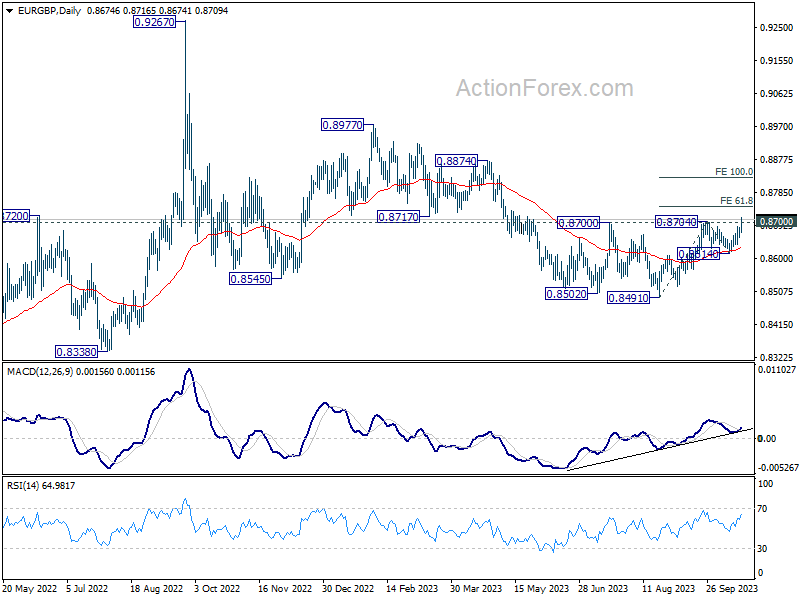

Technically, EUR/GBP’s break of 0.8700/4 resistance zone confirms resumption of rise from 0.8491. More importantly, the development suggest strengthens the case that corrective pattern from 0.9267 has completed with three waves down to 0.8941. Next near term target is 61.8% projection of 0.8419 to 0.8704 from 0.8614 at 0.8746. Decisive break there could prompt upside acceleration to 100% projection at 0.8827 next. A major question is whether this rally in EUR/GBP can inject vitality into EUR/USD, propelling it beyond 1.0639 resistance and heralding a stronger rebound.

In Europe, at the time of writing, FTSE is down -1.00%. DAX is down -0.19%. CAC is down -0.60%. Germany 10-year yield is down -0.008 at 2.922. Earlier in Asia, Nikkei fell -1.91%. Hong Kong HSI fell -2.46%. China Shanghai SSE fell -1.74%. Singapore Strait Times fell -1.18%. Japan 10-year JGB yield rose 0.0391 to 0.847.

US initial jobless claims fell to 198k, vs exp 210k

US initial jobless claims fell -13k to 198k in the week ending October 14, below expectation of 210k. Four-week moving average of initial claims dropped -1k to 206k.

Continuing claims rose 29k to 1743k in the week ending October 7. Four-week moving average of continuing claims rose 19k to 1694k.

BoJ’s regional economic report unveils broadest upgrade since mid 2022

In the Regional Economic Report released today, BoJ upgraded the economic assessment for six regions, marking the most substantial uplift since July 2022. The regions experiencing this optimistic revision include Hokkaido, Tohoku, Hokuriku, Kanto-Koshinetsu, Chugoku, and Shikoku. Conversely, the economic outlook for Tokai, Kinki, and Kyushu-Okinawa remained steady.

This comprehensive upgrade underscores the resilience and adaptability of the Japanese economy. Despite the headwinds presented by decelerating recovery in overseas economies and rising prices domestically, all nine regions delineated a narrative of an economy that is either picking up momentum or recovering at a moderate pace.

On a related note, a separate report from branch managers indicated that many companies, due to a structural labor shortage, are gearing up to continue wage increments in the upcoming fiscal year. However, the magnitude of these wage hikes will largely depend on competitor trends and upcoming price movements, especially as the spring labor unions of next year approach.

Japan’s export rose 4.3% yoy in Sep amid US and European demand

Japan saw a welcomed increase in exports in September, breaking a two-month declining trend and outpacing forecasts. Exports rose by 4.3% yoy to JPY 9198B, surpassing the anticipated growth of 3.1% yoy.

A closer examination of the trade partners reveals a contrasting scenario. Exports to China, Japan’s prominent trading partner, dipped by -6.2% yoy, marking the tenth consecutive month of decline. A staggering -58% yoy drop in food shipments contributed significantly to this contraction. Conversely, trade ties with US and Europe exhibited robustness, with exports expanding by 13.0% yoy and 12.9% yoy respectively.

On the import front, Japan reported a decline of -16.3% yoy to JPY 9136B, a steeper fall than the anticipated -12.9% yoy. Trade dynamics shifted, with Japan posting a trade surplus of JPY 62.4B.

When assessed in seasonally adjusted terms, exports went up by 7.2% mom to JPY 8910B, while imports climbed by 5.4% mom, reaching JPY 9345B. Consequently, trade deficit was reduced to JPY -434B.

Australia employment grows a mere 6.7%, unemployment rate ticks down

Australia’s job market portrayed a mixed picture in September, with a significant undershoot in employment growth countered by a lower-than-expected unemployment rate.

The country added a mere 6.7k jobs in the month, a far cry from the anticipated 20.3k. Delving deeper into the data, full-time employment took a hit, shrinking by -39.9k. However, this was partly offset by increase in part-time roles, which swelled by 46.5k.

Unemployment rate showed slight improvement, ticking down to 3.6% from previous 3.7%, despite expectations that it would remain steady. Yet, this decline could be attributed to a drop in participation rate, which receded from 67.0% to 66.7%. Meanwhile, total monthly hours worked contracted by -0.4% mom, equivalent to a reduction of 8 million hours.

Kate Lamb, ABS’s head of labour statistics, highlighted that, when considering the last two months, the average monthly employment growth stood at 35k, in line with the yearly average growth. However, Lamb also drew attention to the declining unemployment rate in September, indicating it primarily resulted from a shift of people from the unemployed category to being outside the labor force altogether.

Furthermore, she noted, “The recent softening in hours worked, relative to employment growth, may suggest an easing in labour market strength.”

Australia’s business confidence shows uptick, but inflationary concerns persist

Australian businesses are displaying signs of renewed optimism, as revealed by NAB Quarterly Business Confidence index for Q3. The index improved, moving up from -4 in the second quarter to -1 in the third. Moreover, the gauge for Current Business Conditions also indicated better sentiment, rising from 11 to 13.

However, an undercurrent of concern persisted regarding cost dynamics. Labour cost growth experienced an increase, shifting up to 1.8% from the 1.3% witnessed in Q2. On the other hand, purchase costs growth showed a modest climb, reaching 1.4% from the 1.3% seen in the previous quarter. In a positive sign, fewer businesses highlighted materials as a limiting factor, with the percentage dropping to 32% from the 36% reported in Q2.

NAB’s Chief Economist Alan Oster noted, “Price growth remained elevated in Q3. This is in line with our expectation for a reasonably strong inflation print of 1.1% for the quarter when the full Q3 CPI is released next week.”

However, he tempered the immediate inflationary concerns with a longer-term view, adding, “Still, we do expect inflation to moderate gradually as the economy slows.”

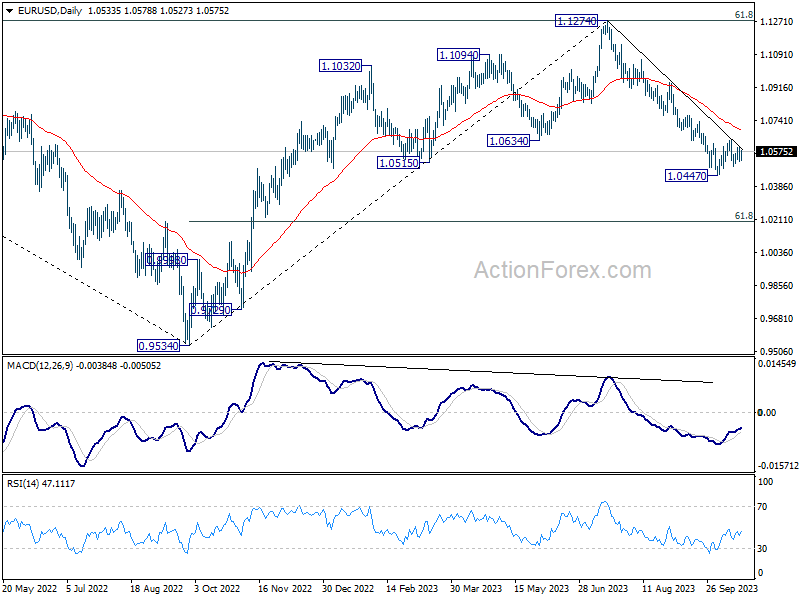

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0508; (P) 1.0551; (R1) 1.0579; More…

EUR/USD is still extending sideway trading between 1.0447 and 1.0639 and intraday bias stays neutral. Near term outlook stays bearish with 1.0639 resistance intact. On the downside, firm break of 1.0447 will resume whole fall from 1.1274 and target 1.0199 fibonacci level. On the upside, however, break of 1.0639 will resume the rebound from 1.0447 to 55 D EMA (now at 1.0692).

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0692) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Sep | -0.43T | -0.50T | -0.56T | -0.55T |

| 00:30 | AUD | NAB Business Confidence Q3 | -1 | -3 | -4 | |

| 00:30 | AUD | Employment Change Sep | 6.7K | 20.3K | 64.9K | 63.3K |

| 00:30 | AUD | Unemployment Rate Sep | 3.60% | 3.70% | 3.70% | |

| 06:00 | CHF | Trade Balance (CHF) Sep | 6.32B | 3.77B | 4.05B | 3.81B |

| 08:00 | EUR | Eurozone Current Account (EUR) Aug | 27.7B | 20.9B | 21.0B | |

| 12:30 | CAD | Industrial Product Price M/M Sep | 0.40% | 0.30% | 1.30% | |

| 12:30 | CAD | Raw Material Price Index Sep | 3.50% | 1.80% | 3.00% | |

| 12:30 | USD | Initial Jobless Claims (Oct 13) | 198K | 210K | 209K | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Oct | -9 | -6.5 | -13.5 | |

| 14:00 | USD | Existing Home Sales Sep | 3.90M | 4.04M | ||

| 14:30 | USD | Natural Gas Storage | 82B | 84B |