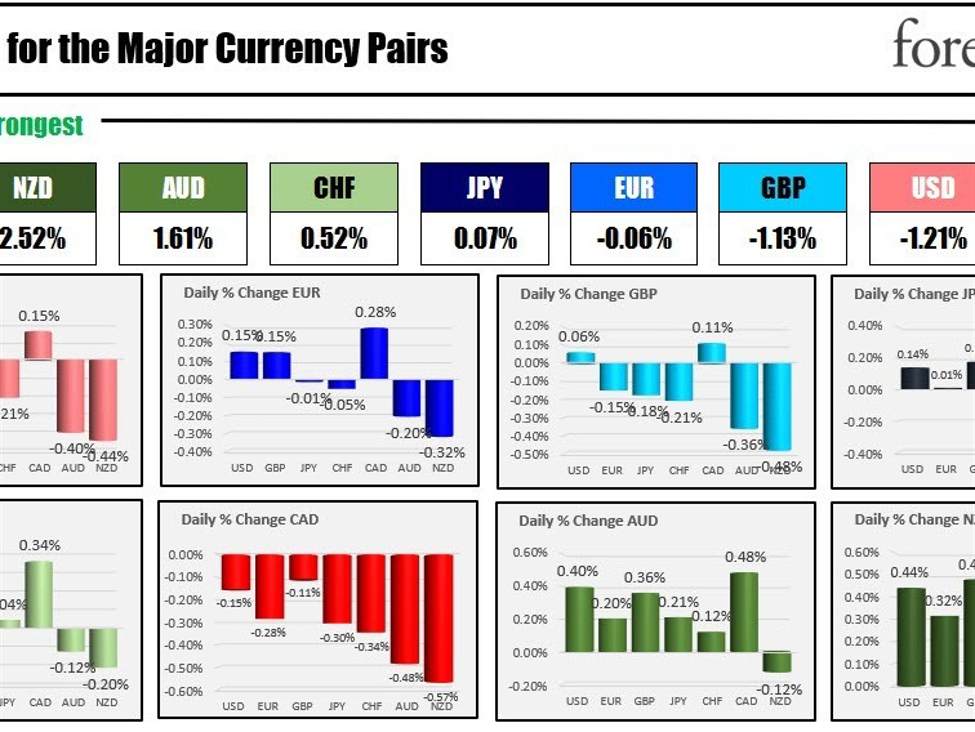

The strongest to the weakest of the major currencies

As the North American session begins, the NZD is the strongest and the CAD is the weakest. The USD is lower as yields dip modestly in early US trading.

It is one more sleep until the BLS releases their latest US jobs report for September with expectations of a gain of 170K versus 187K last month. Yesterday the ADP employment report came in weaker than expected at 89K. However, the correlation between it and the nonfarm payroll report can be sketchy. The US unemployment rate is expected to dip to 3.7% from 3.8% last month (which was the highest level since March 2022). Average hourly earnings are expected to rise by 0.3% MoM/4.3% YoY. Today the weekly initial jobless claims are expected to rise modestly to 210K versus 204K last week. The jobless claims have dipped back down toward the 200K area after peaking near 260K in May and June this year. The JOLTs job openings surprised the market this week when it rose unexpectedly to 9.61M vs 8.8M estimate

Meanwhile, as the US auto strike continues without meaningful results, talks between Kaiser Permanente and unions representing over 75,000 workers have stalled, leading to the largest healthcare sector strike in U.S. history. Although Kaiser claimed a tentative agreement on some issues, unions are awaiting a meaningful response. The unions demand better pay and more staff to address staffing shortages. A three-day work stoppage is in effect, involving various healthcare professionals in five U.S. states and Washington D.C., impacting approximately 13 million patients. Kaiser assures that its hospitals and emergency facilities will remain open, yet the trend of strikes continues to increase inflation trends and rate fears.

Yesterday oil prices moved sharply lower. Although the weekly oil inventory data showed a bigger than expected draw, the gasoline inventories showed a significant build indicating the slower demand after the summer holiday season. The price of crude oil fell -5.61%, it’s worse one-day decline since September 2022. The sharp decline came despite OPEC+ confirming that Saudi Arabia and Russia would maintain reduced output levels.

A snapshot of the markets as the NA session gets underway shows:

- Crude oil is trading down $-1.48 or -1.73% at $82.76

- Spot gold is trading down $0.11 or 0.01% $1821

- Spot silver is trading up $0.08 or 0.39% at $21.07

- Bitcoin is trading at $27,753. At this time yesterday the price was trading at $27,588.

In the US premarket for US stocks, futures are implying a mixed opening

- Dow Industrial Average futures are implying a fall of – 22.55 points after yesterday’s 127.17 point rise

- S&P index futures are implying a fall of 2.50 points after yesterday’s gain of 34.30 points

- NASDAQ futures are implying a rise of 32 points after yesterday’s 176.54 point rise

In the European equity markets, the major indices are trading higher:

- German DAX, +0.15%

- France’s CAC, +0.16%

- UK’s FTSE 100, +0.57%

- Spain’s Ibex, +0.67%

- Italy’s FTSE MIB, -0.06% (10 minute delay)

In the US debt market, yields are modestly lower:

- 2-year yield, 5.026% -2.3 basis points. At this time yesterday, the yield was at 5.131%

- 5-year yield, 4.685% -3.6 basis points. At this time yesterday the yield was at 4.788%

- 10-year yield, 4.710% -2.5 basis points. At this time yesterday, the yield was at 4.776%

- 30-year yield, 4.860% -1.7 basis points at this time yesterday, the yield was at 4.896%

- The 2 – 10 year spread is trading at -31 basis points as he continues to work off its negative yield curve. At this time yesterday, the spread was at -35 basis points.

In the European debt market, benchmark 10-year yields are trading mixed/little-changed:

European benchmark 10 year yields