Dollar is slightly softer today as the financial world holds its breath for FOMC rate decision. With the market strongly anticipating a hold, eyes will turn to the dot plot for insights. The pivotal question remains: Will there be hints of another rate hike slated for this year? Furthermore, how the dot plot for 2024 maps out the anticipated timeline and pace of rate cuts will be under close observation. Complementing the dot plot, growth and inflation projections will offer a clearer lens on Fed’s viewpoint.

Across the pond, Sterling has taken a hit, emerging as the day’s weakest performer in the wake of weaker than expected consumer inflation figures. This has led the market to rapidly adjust its expectations, with the possibility of a BoE rate hike tomorrow now seeming less likely. Current swap-market data places this chance at under 50%. Historically, however, BoE’s voting in tight situations has been unpredictable. Regardless of the outcome, the consensus is that UK interest rates will probably reach their upper limit post the decision.

Elsewhere in the currency markets, Australian Dollar stands out as the top performer, closely trailed by New Zealand Dollar and then Euro. Canadian Dollar’s position is mixed, with Japanese Yen and Swiss Franc trailing behind as weaker contenders.

Looking at the technical aspects, investor sentiment toward Fed’s decision and projections would be significantly illuminated by DOW’s performance. To confirm a positive reception, DOW would need to convincingly break 34977.97 resistance level. Should this occur, it would suggest that the corrective fall from 35679.13 has concluded, paving the way for resumption of the larger uptrend. Conversely, should 34029.22 support threshold be breached, it would signify a more negative investor sentiment. As is customary, the direction of Dollar will likely move inversely to market risk sentiment.

In Europe, at the time of writing, FTSE is up 0.77%. DAX is up 0.60%. CAC is up 0.52%. Germany 10-year yield is down -0.016 at 2.726. Earlier in Asia, Nikkei dropped -0.66%. Hong Kong HSI dropped -0.62%. China Shanghai SSE dropped -0.52%. Japan 10-year JGB yield rose 0.0064 to 0.725.

Swiss SECO downgrades 2024 growth forecast, raises inflation

In the update to Swiss State Secretariat for Economic Affairs economic forecasts, a marginal upgrade has been bestowed upon Switzerland’s 2023 GDP outlook, leveraging the robust performance in the first quarter. The forecast, adjusted for sporting events, now stands at 1.3%, a slight increase from the 1.1% predicted in June.

Despite this adjustment, outlook for 2024 has experienced a cut, settling at 1.2% as opposed to the earlier estimation of 1.5%. This renders the prospects for economic growth considerably below-average for both 2023 and 2024.

Shifting focus to CPI forecasts, the estimation for 2023 have been marginally trimmed down to 2.2%, a -0.1% decrease from June forecast. Conversely, 2024 projection experiences a hike, ascending from 1.5% to 1.9%.

SECO points towards substantial economic risks looming on the horizon. A pressing concern is the international persistence of inflation. The panorama of economic challenges also encompasses escalating risks tied to the global debt scenario fluctuations in property and financial markets. Monetary policy transmission could also be stronger than assumed.

Furthermore, the evolving situations in Germany and China emerge as potent risk factors, not just for the global economy but significantly impacting Swiss foreign trade.

UK CPI slowed to 6.7%, BoE’s hike tomorrow could be the last

Sterling is facing headwinds after release of UK’s CPI inflation data, which came in lower than market forecasts. This development strengthens the speculation that BoE might be drawing curtains on its tightening cycle, with the one more hike expected tomorrow potentially being the concluding move.

The reported data illustrated deceleration in CPI from of 6.8% yoy to 6.7% yoy in August, a result that fell short of the projected escalation to 7.1% yoy. This is the lowest rate witnessed since February 2022.

A deeper dive into the components reveals that this softening of annual CPI into August 2023 emerged from six out of the 12 sectors. Notably, restaurants and hotels, along with food and non-alcoholic beverages, played a pivotal role in pulling down the numbers. However, the motor fuels category within the transport sector exerted upward pressure, somewhat counterbalancing the decline.

Furthermore, core CPI, which is calculated by excluding variables such as energy, food, alcohol, and tobacco, followed suit, decelerating from 6.9% yoy to 6.2% yoy. This stands significantly below anticipated rate of 6.8% yoy.

Breaking it down further, while CPI goods noted a slight acceleration from 6.1% yoy to 6.3% yoy, CPI services delineated a slowdown from 7.4% yoy to 6.8% yoy.

For the month. CPI rose 0.3% mom, below expectation of 0.7% mom.

Japan’s exports to China tumble further, trade with US flourishes

Japan’s economic data shows a dwindling momentum in the country’s export sector, registering a decline of -0.8% yoy to JPY 7994B in August, with a particularly notable decrease in its trading activities with China.

The continued dip in exports is largely attributed to diminishing overseas demand and the trade restrictions imposed by China, which have significantly impacted Japan’s trade balance.

A striking example is seen in the sharp -11.0% yoy decline in exports to China, to a total of JPY 1.44T. This downturn marks the third consecutive month of double-digit drops in export activities to China, severely affected by the -41.2% yoy plunge in food exports due to China’s ban on Japanese seafood.

However, a beacon of positivity trading rapport with US, which saw a growth spurt of 5.1% yoy, aggregating to a record JPY 1.62T for the month of August. This surge has been primarily fueled by a heightened demand for Japanese cars, mining, and construction machinery.

On the import front, Japan noted a considerable -17.8% yoy reduction to JPY 8925B, with imports from China dipping -12.1% to JPY 1.93T, and those from US falling -9.5% yoy to JPY 967.39B. The nation’s trade balance has consequently been reported at a deficit of JPY -930.5B.

When analyzed in seasonally adjusted terms, both exports and imports showcase a month-on-month decrease, registering -1.7% mom to JPY 8267.8B and -2.1% mom to JPY 8823.6B, respectively. Thankfully, there is a silver lining as the trade deficit has slightly narrowed compared to the previous month, standing at JPY -555.7B.

Australia Westpac leading index edged up to -0.5%, growth struggles despite population boom

Westpac Leading Index for Australia indicates that the nation’s growth outlook remains subdued. The index inched up marginally from -0.56% to -0.50% in August, marking a year since it began registering negative readings. These figures suggest that the prospect of per capita GDP advancing in the coming 3–9 months appears bleak.

Westpac’s forecasts for the next year resonate with the index’s gloomy narrative, anticipating an economic growth of less than 1% for the year leading up to June 2024. Interestingly, there’s a potential silver lining: with predictions pointing to population growth surpassing 2% in 2023, this could introduce some upside risks to the otherwise somber economic projections.

However, despite this population surge, the economy is projected to trail behind, as evident from the March and June quarter results. Both quarters witnessed a contraction of -0.3% in GDP per capita, a pattern that’s predicted to persist in the forthcoming year.

Regarding next RBA rate decision on October 3, Westpac said it’s “almost certain to hold rates steady for another month”. The crucial data for the next move would be September quarter inflation report, which will not be available until the November RBA meeting.

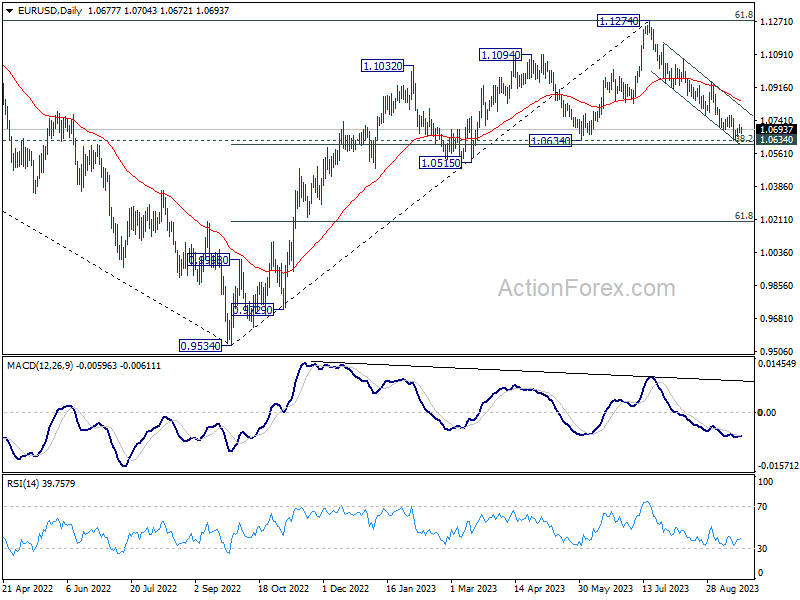

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0663; (P) 1.0691; (R1) 1.0706; More…

EUR/USD is still bounded in established range and intraday bias remains neutral. Strong rebound from current level, followed by break of 1.0767 resistance, should confirm short term bottoming. Intraday bias will be back on the upside for 1.0944 resistance. However, sustained break of 1.0609/34 support zone will carry larger bearish implication, and target 1.0515 support next.

In the bigger picture, fall from 1.1274 medium term top is seen as a correction to up trend from 0.9534 (2022 low). Strong support could be seen from 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609) to bring rebound, at least on first attempt. However, sustained break of 1.0609/0634 will raise the chance of bearish trend reversal, and target 61.8% retracement at 1.0199.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q2 | -4.21B | -4.40B | -5.22B | -4.66B |

| 23:50 | JPY | Trade Balance (JPY) Aug | -0.56T | -0.44T | -0.56T | -0.60T |

| 00:30 | AUD | Westpac Leading Index M/M Aug | 0.00% | 0.00% | ||

| 06:00 | EUR | Germany PPI M/M Aug | 0.30% | 0.20% | -1.10% | |

| 06:00 | EUR | Germany PPI Y/Y Aug | -12.60% | -12.80% | -6.00% | |

| 06:00 | GBP | CPI M/M Aug | 0.30% | 0.70% | -0.40% | |

| 06:00 | GBP | CPI Y/Y Aug | 6.70% | 7.10% | 6.80% | |

| 06:00 | GBP | Core CPI Y/Y Aug | 6.20% | 6.80% | 6.90% | |

| 06:00 | GBP | RPI M/M Aug | 0.60% | 0.90% | -0.60% | |

| 06:00 | GBP | RPI Y/Y Aug | 9.10% | 9.30% | 9.00% | |

| 06:00 | GBP | PPI Input M/M Aug | 0.40% | 0.20% | -0.40% | |

| 06:00 | GBP | PPI Input Y/Y Aug | -2.30% | -2.70% | -3.30% | -3.20% |

| 06:00 | GBP | PPI Output M/M Aug | 0.20% | 0.20% | 0.10% | 0.20% |

| 06:00 | GBP | PPI Output Y/Y Aug | -0.40% | -0.80% | -0.70% | |

| 06:00 | GBP | PPI Core Output M/M Aug | -0.10% | 0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Aug | 1.60% | 2.30% | 2.20% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 14:30 | USD | Crude Oil Inventories | -1.3M | 4.0M | ||

| 18:00 | USD | Fed Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |