Yen displayed impressive strength in Asian session, following hawkish remarks from BoJ Governor Kazuo Ueda over the weekend. Speculation is rife that the central bank is laying down preparations to exit negative rates early next year, with sustained wage growth being a key prerequisite, as echoed by various BoJ officials.

Meanwhile, both Australian and New Zealand Dollars are seeing a revival, largely supported by rebound in Chinese Yuan. This bounce back was facilitated by the PBoC’s stronger-than-expected daily fixing by a record margin. Reinforcing its stance on currency stability, the Chinese central bank declared its commitment to “correct one-sided and pro-cyclical activities,” vowing to stave off undue currency risks and speculatory behaviors that might disrupt the foreign exchange market’s orderly operations.

On the other hand, Dollar is trading generally lower as it undergoes a consolidation phase, absorbing some of the gains from last week. The greenback is poised to engage in more consolidative trading as markets anticipate the release of Wednesday’s US CPI data. In Europe, Euro presents a mixed picture, with investors keenly awaiting the ECB’s rate decision scheduled for Thursday.

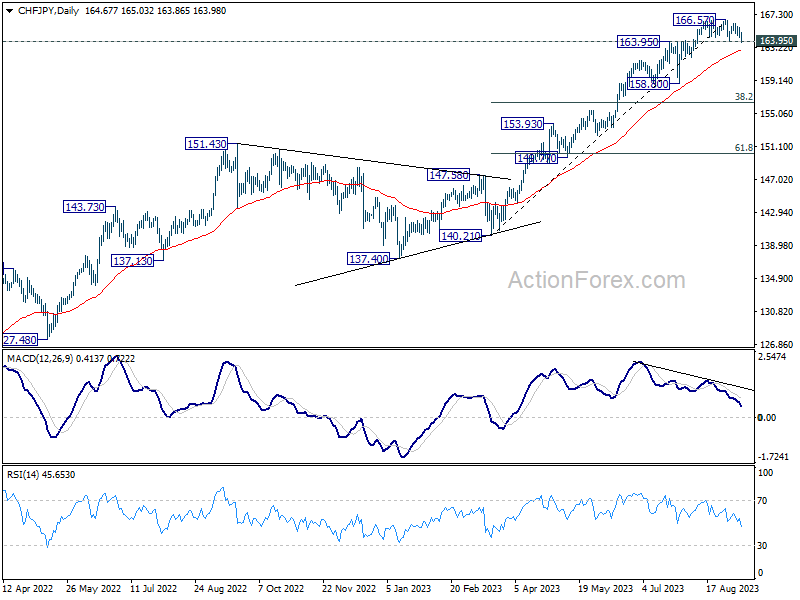

From a technical standpoint, CHF/JPY’s breach of 163.95 resistance-turned-support, combined with bearish divergence observed in D MACD, indicates the possibility of a more extensive correction on the horizon. Near term attention has shifted towards 55 D EMA (now at 162.81). Sustained trading below this EMA might instigate a steeper decline towards 38.2% retracement of 140.21 to 166.57 at 156.50. Nonetheless, robust rebound from the EMA would maintain near-term bullish outlook, paving the way for an extension of the recent upward trend, sooner rather than later.

In Asia, at the time of writing, Nikkei is down -0.48%. Hong Kong HSI is down -0.77%. China Shanghai SSE is up 1.13%. Singapore Strait Times is up 0.09%. Japan 10-year JGB yield is up 0.0550 at 0.706.

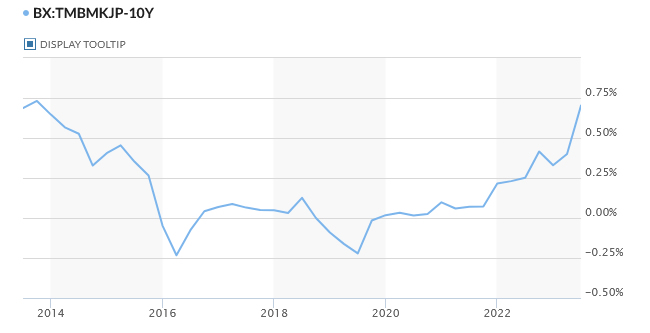

10-year JGB yield hits 9-year high on BoJ Ueda, Yen rebounds

Yen saw a notable uptick in Asian session, buoyed by hawkish sentiments by BoJ Governor Kazuo Ueda. Concurrently, 10-year JGB yield scaled its highest level in nine years, breaching 0.7% mark.

In an interview with Yomiuri newspaper published over the weekend, Ueda hinted at the possibility that BoJ might have sufficient data by the close of the year to contemplate ending its negative interest rate policy. Such remarks from Ueda have spurred speculation among market analysts, with some interpreting them as early signals for the markets, suggesting a potential end to negative interest rates by Q1 2024. Before this step, there also are anticipations of yield curve control being phased out later this year.

On the flip side, certain analysts, referencing recent data which highlights decelerating wage growth, argue that the transition from negative rates might not be imminent. They believe Ueda’s remarks might be more of a countermeasure to Yen’s recent depreciation.

Ueda, during the interview, emphasized the need for Japan to witness a consistent rise in inflation, complemented by wage growth, before implementing changes. “If we judge that Japan can achieve its inflation target even after ending negative rates, we’ll do so,” Ueda asserted. However, he also reiterated the central bank’s stance on maintaining its ultra-loose policy for now, until there’s firm confidence that inflation will consistently hover around the 2% mark, bolstered by robust demand and wage growth.

He cautioned, “While Japan is showing budding positive signs, achievement of our target isn’t in sight yet.” Looking ahead, Ueda underscored the importance of wage trajectories in the coming year, indicating that conclusive decisions would be data-driven. “We can’t rule out the possibility we’ll get enough information and data by year-end,” Ueda added

A pivotal week with ECB, US CPI, UK GDP and employment, and Chinese data

A series of high-profile events are scheduled for the week, Euro finds itself on unstable grounds ahead of ECB’s rate decision slated for this Thursday. Dollar is staying firm as US anticipates pivotal CPI data on Wednesday. There are also substantial economic releases from UK and China.

ECB stands at a crossroads, grappling with the choice of either implementing a 10th consecutive rate hike — potentially elevating main refinancing rate to 4.50% and deposit rate to 4.0% — or pausing to assess the evolving economic and inflation development. The consensus among economists is far from unanimous, although a slightly larger faction envisages ECB holding steady.

Market stakeholders also await the new ECB staff economic projections with bated breath, keen to discern any adjustments to 2023 inflation outlook influenced by rising oil prices since June. However, the pivotal elements in shaping policy guidance remain the projections for 2024 and 2025, given the recent slowdown in the Eurozone service sector and the broader economy hinting at reduced price pressures.

For Euro, the ideal bullish outcome would be a combination of a rate hike along with significant upward revision in inflation forecasts, with growth projections taking only a minor hit. However, such outcome seems to be on the less probable side of the spectrum. Conversely, if ECB signals that the terminal rate has been reached, combined with a subdued economic outlook for the upcoming year, Euro could face a steep decline.

US market is gearing up for the critical release of August CPI data this Wednesday, a development holding notable sway over market movements. Market observers should take note Fed policymakers are placing significant emphasis on the month-on-month core inflation rate, perhaps even more so than its year-over-year counterpart.

Headline CPI could experience a significant surge, leaping by 0.6% mom. This spike can be attributed in large part to almost 10% surge in gas prices. That would translate to re-acceleration in annual headline inflation rate from 3.2% yoy to 3.6% yoy.

However, it’s worth noting that this gas-induced inflationary rise might not cause much concern among Fed officials. From their perspective, the real metric to watch is core CPI, which excludes volatile elements like food and energy prices. If core CPI maintains its steady 0.2% mom growth, this would result in an annual rate reduction from 4.7% yoy to around 4.3% yoy. Such deceleration would align with Fed’s expectation of moderating inflationary pressures.

In UK, spotlight is firmly on upcoming economic revelations including employment and GDP data, with significant implications for Sterling. Recent comments from BoE Governor Andrew Bailey about being “much nearer now to the top of the cycle” have exerted downward pressure on Pound, positioning it as the second-worst performer of the month, overtaken only by Australian Dollar.

Another BoE rate hike is still widely anticipated on September 21. However, the looming economic releases stand as potential turning points that could alter the path beyond that significantly. Slowdown in wages growth coupled with disappointing GDP figures might drastically reduce the likelihood of further monetary tightening in the aftermath of this forthcoming meeting.

Simultaneously, Australian Dollar will be influenced by both domestic employment data and a suite of economic releases from China, its largest trading partner. In particular, industrial production and retail sales data will reveal much insight into the impact of persistently sluggish exports and weak domestic demand.

Here are some highlights for the week:

- Monday: Japan M2, machine tool orders; Italy industrial production.

- Tuesday: Australia Westpac consumer sentiment, NAB business confidence; UK employment; Germany ZEW;

- Wednesday: UK GDP, production, trade balance; Eurozone industrial production; US CPI.

- Thursday: Japan machine orders; Australia employment; Swiss PPI; ECB rate decision; US PPI, retail sales, jobless claims, business inventories.

- Friday: New Zealand BusinessNZ manufacturing; China industrial production, retail sales, fixed asset investment; Japan tertiary industry index; Eurozone trade balance; Canada manufacturing sales; US Empire State manufacturing, import prices, industrial production, U of Michigan consumer sentiment.

USD/JPY Daily Outlook

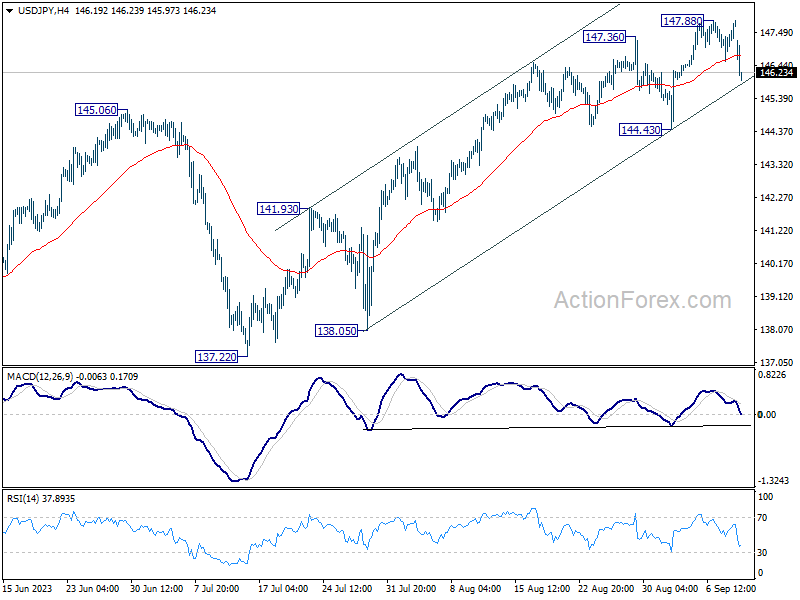

Daily Pivots: (S1) 146.93; (P) 147.40; (R1) 147.76; More…

USD/JPY dips notably today, but stays well above 144.43 support. Intraday bias remains neutral at this point, as consolidation from 147.88 could extend. But outlook remains bullish with 144.43 support intact. On the upside, above 147.88 will resume larger rise from 127.20, to retest 151.93 high.

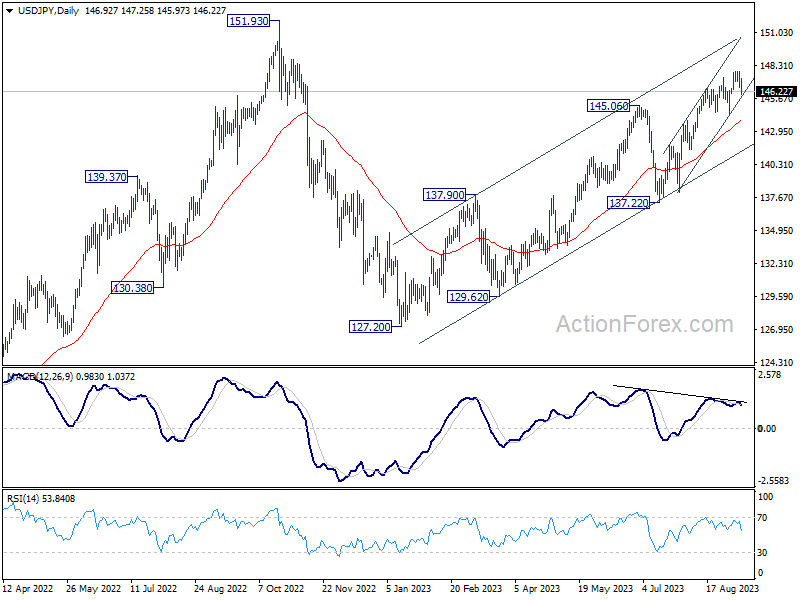

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jul | 2.50% | 2.50% | 2.40% | 2.50% |

| 06:00 | JPY | Machine Tool Orders Y/Y Aug P | -19.80% | |||

| 08:00 | EUR | Italy Industrial Output M/M Jul | -0.30% | 0.50% |