As the financial world gears up for the much-anticipated remarks from Fed Chair Jerome Powell and ECB President Christine Lagarde, market participants are treading with caution. Dollar has started to retreat, shedding some of its recent impressive gains. Simultaneously, Euro grapples to find solid ground elsewhere amidst a mixed backdrop.

Both leading central bank figures hold the potential to introduce unexpected elements in their addresses, and market stakeholders are all too aware of the volatility this could trigger. The spotlight on Powell will shine particularly on his interpretation of the juxtaposed trends of softening headline inflation and the persistence of service sector prices. Additionally, the consequences of robust consumer spending will be keenly observed.

In the European context, the grapevine is abuzz with speculation. Following the recently revealed PMI data, which fell well short of market expectations, rumors are rife that Lagarde might hint at a monetary policy pause in September. Such a move, if communicated or even hinted at, could instigate significant market shifts as the week concludes.

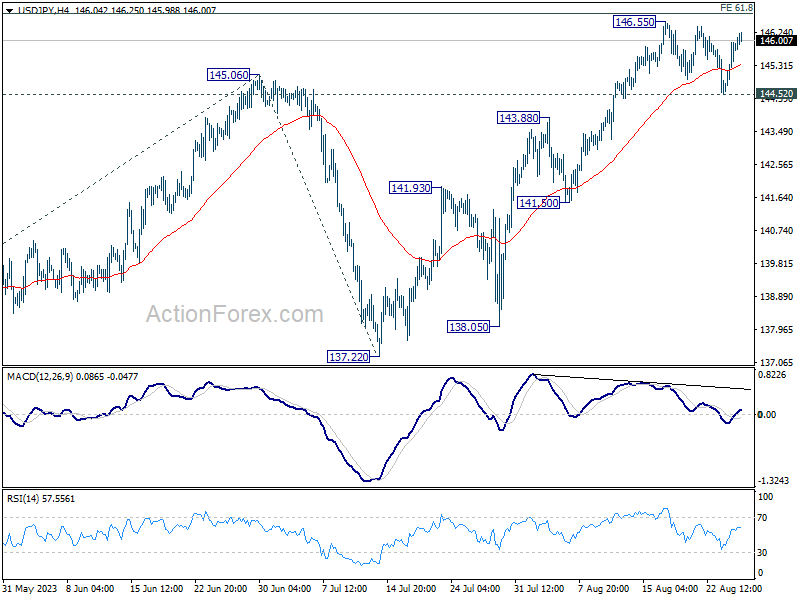

Technically, to indicate a near term bearish reversal in Dollar, 1.0929 resistance in EUR/USD, 1.2799 resistance in GBP/USD, 0.8758 support in USD/CHF will need to be taken out decisively Meanwhile, for Dollar to confirm underlying bullish momentum, UUSD/JPY and USD/CD should break through 146.55 and 1.3602 resistance respectively with ease. The market awaits these developments with bated breath.

In Europe, at the time of writing, FTSE is up 0.66%. DAX is up 0.65%. CAC is up 0.88%. Germany 10-year yield is up 0.0368 at 2.553. Earlier in Asia, Nikkei dropped -2.05%. Hong Kong HSI dropped -1.40%. China Shanghai SSE dropped -0.56%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield rose 0.0110 to 0.660.

German Ifo business climate sinks for fourth month, economy faces uphill battle

Germany’s economic outlook has dimmed yet again, as indicated by the Ifo Business Climate Index which registered its fourth consecutive monthly drop. In August, the index tumbled from 87.4 to 85.7. The downward trajectory was visible across both Current Situation Index, which slid from 91.4 to 89.0, and Expectations Index, which descended from 83.6 to 82.6.

A sectoral breakdown of the data highlighted broad-based concerns. Manufacturing saw a decline from -13.9 to -16.6. Meanwhile, Services sector took a more significant hit, plummeting from a modest 1.0 to a concerning -4.2. Trade and Construction sectors also continued their downward spiral, recording readings of -25.5 and -29.3 respectively, from their previous standings of -23.7 and -24.6.

Ifo’s commentary on the data was stark. They noted, “Assessments of the current situation fell to their lowest level since August 2020.” The institution also flagged a growing pessimism among companies regarding the forthcoming months, adding, “The German economy is not out of the woods yet.”

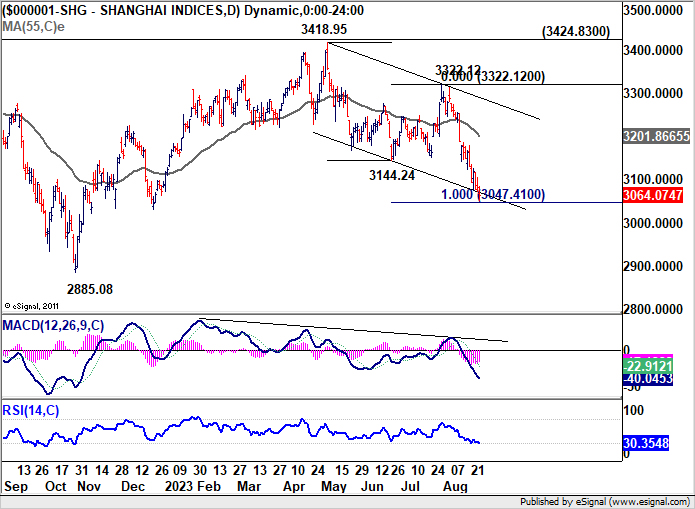

Chinese stocks falter despite efforts to boost confidence

In a bid to shake off the lethargy that has seen Chinese stocks on a decline for three consecutive weeks, authorities have taken notable measures. Yet, the efforts seem to have fallen short. Reports suggest that the Chinese government is contemplating a reduction in stamp duty on stock trading by up to 50%. This is seen as a move to rejuvenate waning investor confidence.

The China Securities and Regulatory Commission also made an endeavor to put concerns at bay. The regulatory body convened a virtual meeting with multiple global financial institutions, emphasizing the resilience and potential of China’s economic landscape. But these overtures seem to have done little in swaying investor sentiment, at least for now.

The Shanghai SSE extended the whole down trend from 3418.95 to close at 3064.07. It’s now in proximity to 100% projection 3418.95 to 3144.24 from 3322.12. Strong rebound from current level, followed by firm break of 3144.24 support turned resistance, will argue that the decline has completed already. The three wave structure would also affirm that it’s merely a corrective move.

However, sustained break of 3047.41 could prompt further downside acceleration towards 2885.08 (2022 low), and open up more medium term bearish bias. The situation could probably unfolded next week and that would be an important risk factor in Asia, in addition to the aftermath of Jackson Hole in the US.

USD/JPY Daily Outlook

Daily Pivots: (S1) 144.98; (P) 145.47; (R1) 146.34; More…

Intraday bias in USD/JPY stays neutral as it’s still bounded in range. On the upside, sustained break of 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76 will pave the way to retest 151.93 high. However, considering bearish divergence condition in 4H MACD, firm break of 144.52 support will be a sign of reversal, and turn bias back to the downside for 55 D EMA (now at 142.45).

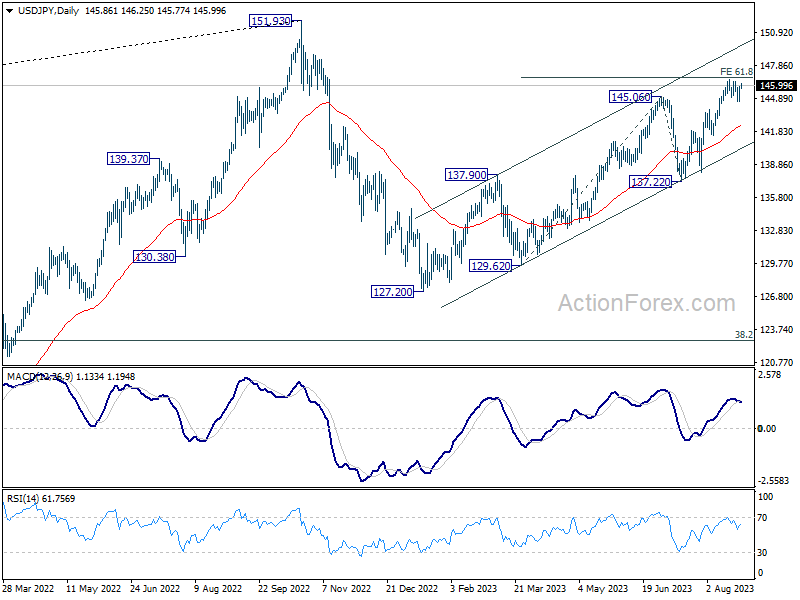

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Aug | 2.90% | 3.00% | 3.20% | |

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Aug | 2.80% | 2.90% | 3.00% | |

| 23:30 | JPY | Tokyo CPI ex Food Energy Y/Y Aug | 4.00% | 4.00% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 1.70% | 1.20% | 1.20% | 1.40% |

| 06:00 | EUR | Germany GDP Q/Q Q2 F | 0.00% | 0.00% | 0.00% | |

| 08:00 | EUR | Germany IFO Business Climate Aug | 85.7 | 86.6 | 87.3 | 87.4 |

| 08:00 | EUR | Germany IFO Current Assessment Aug | 89.0 | 89.8 | 91.3 | 91.4 |

| 08:00 | EUR | Germany IFO Expectations Aug | 82.6 | 83.8 | 83.5 | 83.6 |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug F | 71.2 | 71.2 |