Last week ended with Dollar taking center stage as the best performer, driven by significant turbulence in the bond markets that sent long-end yields sharply higher and provided a mid-week uplift. Although the greenback experienced a notable pullback following non-farm payroll report, it still stands poised for potential further gains, should the selloff in stocks and treasuries continue.

However, the prospects for an extended Dollar rally are laden with uncertainties. The path towards further gains is tethered to a big “if,” with market conditions and sentiments being highly fluid. The real reversal in Dollar might materialize only at a later stage after another dip, depending on how market sentiments develop.

Elsewhere in the currency ranks, Euro finished as the second strongest, followed by Swiss Franc and Japanese Yen—a pattern that is not uncommon in a risk-averse environment. On the other side of the spectrum, Sterling was marked as the weakest among the European majors, a status accentuated by the surprising dovish tilt in BoE’s rate decision.

Commodity currencies found themselves at the bottom of the performance chart, with Australian Dollar leading the descent. Aussie’s fall was notably influenced by RBA’s decision to keep interest rates on hold, and the communications that suggested it could be already in a phase of prolonged pause.

Turbulence in US treasury market overshadows heavy data week

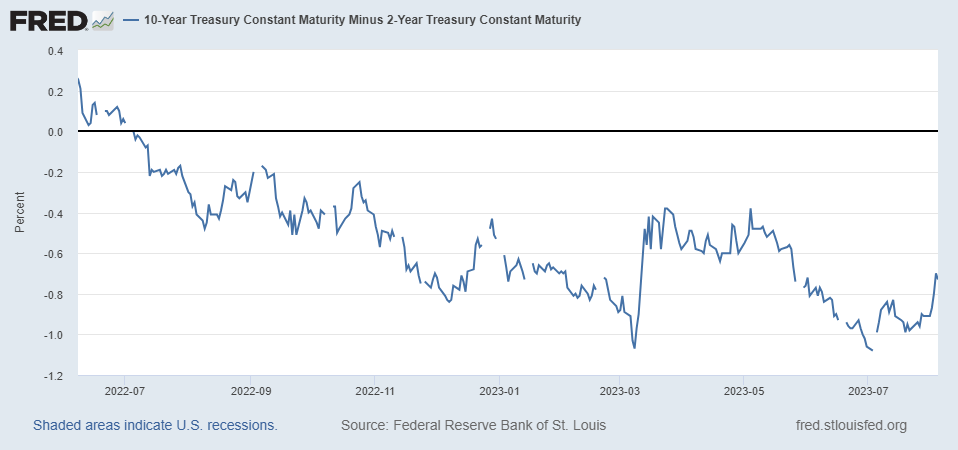

The high volatility in US Treasury somewhat stole the show from heavy data last week. In particular, yields in the long end surged sharply, with 10-year and 30-year yield hitting hitting new highs of the year. More importantly, inversion of 2- and 10-yr yield, once hit the worst level since 1981 in July, reversed notably.

The moves was firstly in reaction to surprised action by Fitch to downgrade US sovereign rating from AAA to AA+, citing “steady deterioration in standards of governance over the last 20 years”. Then, bonds were sold off further after US Treasury said it would it would boost its issuance of long-term debt this quarter, in order to fill the growing gap between tax revenue and government spending.

10-year yield hit as high as 4.206 before being knocked down after non-farm payroll report, and at 4.060. But the overall development further affirmed the case that medium term consolidation from 4.333 has completed with three waves down to 3.253. While some retreat could be seen in the near term, there is no threat to the rally from 3.253 as long as 55 D EMA (now at 3.829) holds.

The bigger question is whether current rise represents resumption of the long term up trend from 0.398 (2020 low). If that’s the case, firm break of 4.333 would set the stage for TNX to head through 5% handle towards 61.8% projection of 1.343 to 4.333 from 3.253 at 5.100.

An accompanied development was the normalization of US 2- to 10-year yield curve, which reverted back the shallowest level since early June. Increasing expectations that Fed is nearing the peak of the tightening cycle,even if not peaked, will cap yields in the short end. Hence there is prospect of further normalization if selloff in 10-year and 30-year bonds is going to continue in the months ahead.

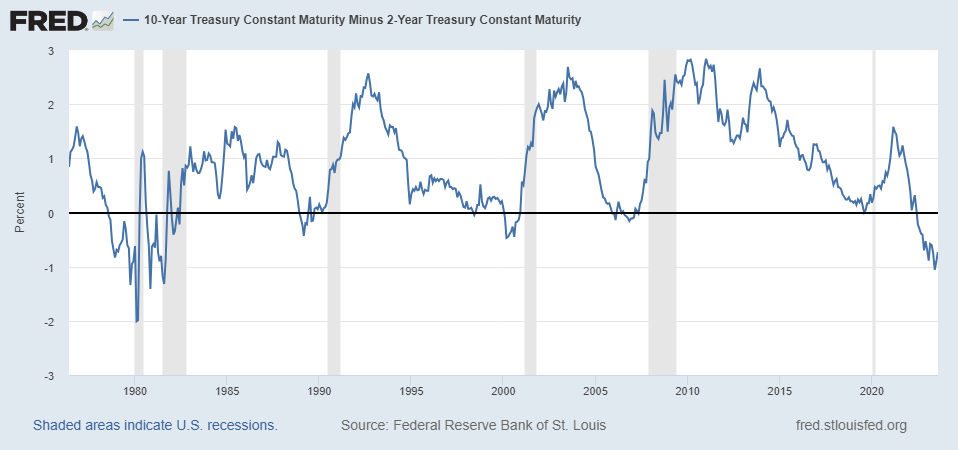

Since the early 90s, the US economy always entered into recession just months after yield curve inversion was fully normalized. That includes relatively brief period of inversion in 2019 and the subsequent short pandemic recession in 2020. Considering the depth and time of the current curve inversion that’s not seen until early 80s, it seems that another recession is inevitable ahead, probably just in a matter of months away.

Let’s now turn to risk sentiment in the markets. S&P 500 ended -2.27% lower last week, its biggest weekly decline since March 10. A short term top should be formed at 4607.07, considering mild bearish divergence condition in D MACD. Deeper pull back is in favor to 55 D EMA (now at 4402.08).

It’s premature to predict a bearish trend reversal in S&P 500. However, if the rise from 3491.58 (2022 low) represents the second leg of the pattern from 4818.62 (2022 high), then it’s actually about time. Even if SPX could notch another high, it should start to feel heavy as it approaches 4818.62. Indeed, firm break of 55 D EMA (now at 4402.08) would be an important warning of reversal, and would likely bring deeper fall to 55 W EMA (now at 4171.02) at the very least.

So beware that the markets are setting themselves up for an “October Crash”, or even a September one.

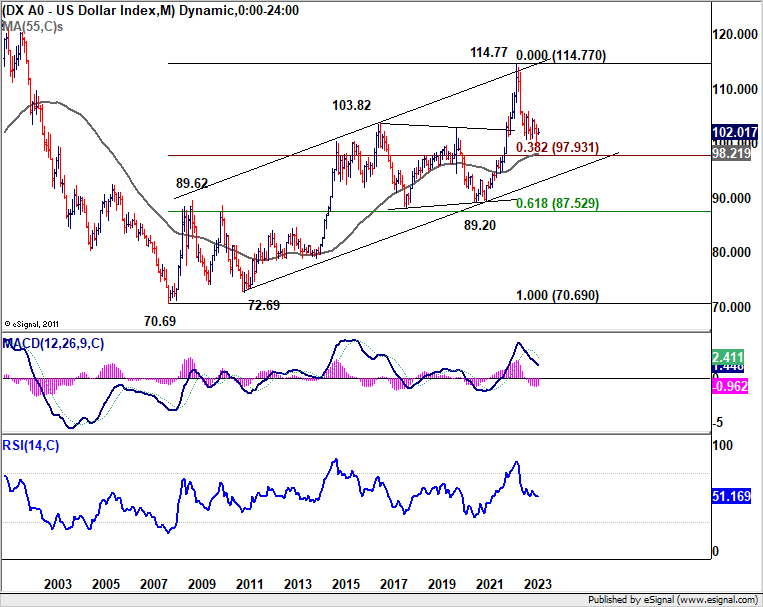

As for Dollar Index, the strong breaks of 101.92 support turned resistance as well as 55 D EMA (now at 102.11) were bullish signals. Yet, the structure and momentum of the rise from 99.57 don’t warrant that it’s a substantial impulsive move. Nevertheless, further rally will now be mildly in favor as long as 100.55 support holds, towards trend line resistance at around 103.80.

Meanwhile, it should be pointed out that even in case of down trend resumption through 99.57, strong support level is expected at around 98 to contain downside, and bring reversal. This support zone represents 61.8% retracement of 89.20 (2021 low) to 114.77 at 98.96, 55 M EMA at 98.21, and 38.2% retracement of 70.69 to 114.77 at 97.93.

So it’s should be just a matter if Dollar is already reversing, or after another fall. That would be subject to developments in bond and stock markets as mentioned above.

Aussie struggles while Sterling pressured, what’s next for GBP/AUD?

Australian Dollar concluded as the weakest performer last we, burdened by growing expectations of a prolonged pause after RBA kept interest rates unchanged at 4.10%. Such expectations were reinforced by the quarterly Statement on Monetary Policy, which indicated the central bank’s increasing confidence in returning in inflation to the target band without further tightening. Aussie faced additional pressures from risk-off sentiment and reversal in Copper prices.

Sterling emerged as the worst performer among European majors, experiencing a selloff following BoE’s 25bps rate hike to 5.25%. The voting wasn’t exactly dovish, with two Monetary Policy Committee members advocating for a 50bps hike while a known dove voted for no change. But the communications were probably starting to set up market expectations for a pause. Speculations are now rife that BoE’s interest rates may not reach the previously anticipated 6% mark, with potentially only one or two more 25bps hikes in the pipeline.

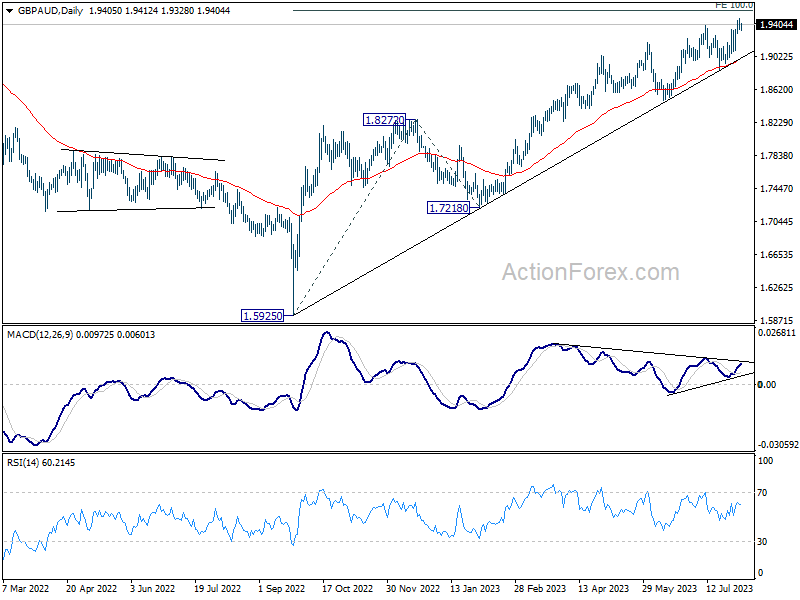

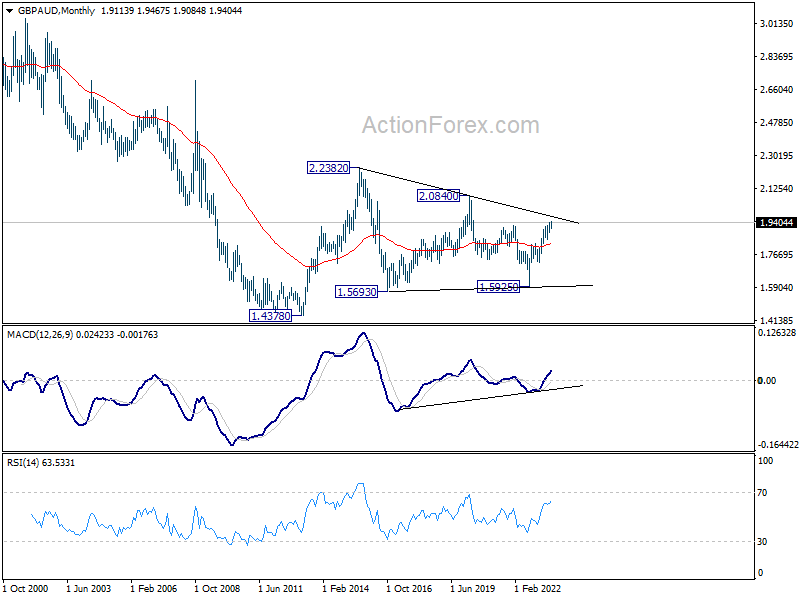

GBP/AUD extended its recent uptrend to 1.9467, but upside momentum seems restrained by bearish divergence condition in D MACD. The cross is now edging closer to the 100% projection of 1.5925 to 1.8272 from 1.7218 at 1.9565, as well as the long-term falling trendline resistance around 1.9766. Consequently, the risk of a correction is starting to loom.

On the downside, break of 1.8847 support level would signal that a medium-term top has formed, potentially leading to a pullback to 55 W EMA (now at 1.8318). If this scenario plays out, it would more likely coincide with a deeper selloff in Sterling across other currency pairs, including against both Dollar and Euro, rather than a solid rebound in Aussie.

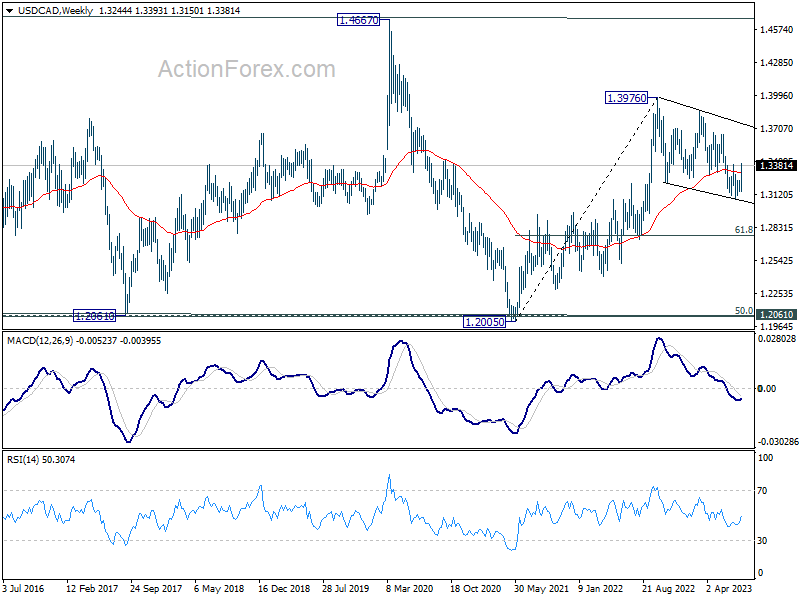

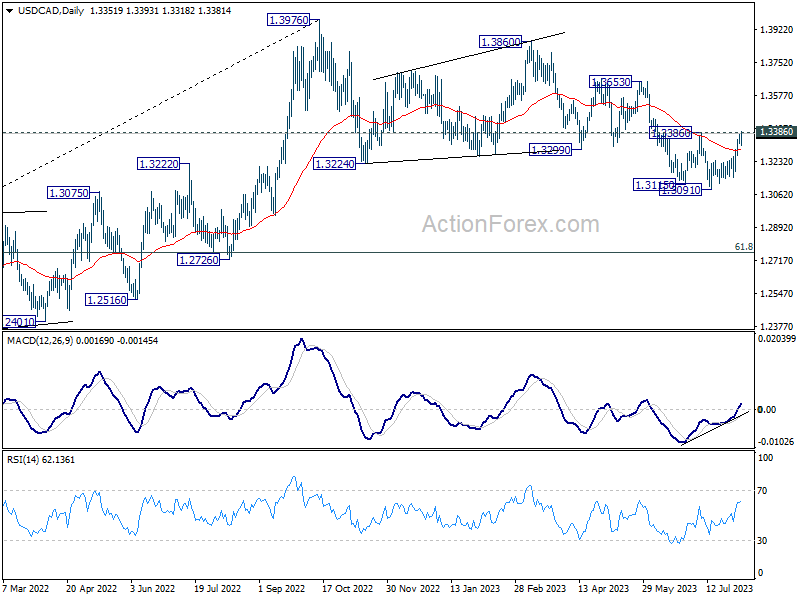

USD/CAD Weekly Outlook

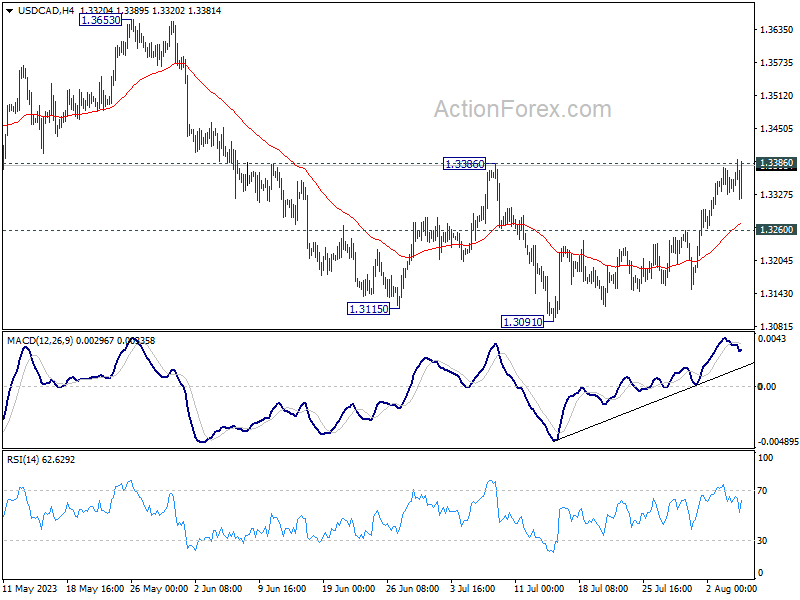

USD/CAD’s rebound from 1.3091 extended higher last week and it’s now pressing 1.3386 resistance. Sustained break of 1.3386 will argue that whole correction from 1.3976 has completed with three waves down to 1.3091. Further rally would then be seen to 1.3653 resistance next. Nevertheless, rejection by 1.3386, followed by break of 1.3260 minor support, should resume larger decline through 1.3091 low.

In the bigger picture, price actions from 1.3976 are viewed as a corrective fall only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976 towards 1.4667/89 long term resistance zone. In case of another fall, downside should be contained by 61.8% retracement of 1.2005 to 1.3976 at 1.2758.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3057) holds.