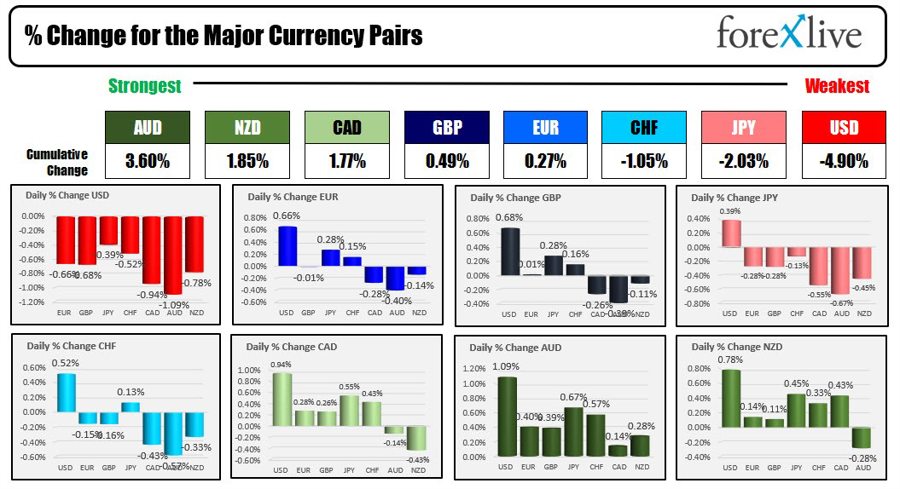

The USD fell sharply today (the greenback is ending the day as the weakest of the major currencies) as the Fed “skip in June” tilt was further priced in despite the fact that ADP and initial jobless claims remained fairly strong (initial jobless claims came in at 232K vs 235K estimate).

There nevertheless was some hope for declining inflationary pressure in the data as well.

The AUD and the NZD were the strongest of the major currencies on flight-to-risk flows. China did announce a better Caixan PMI date today helping the tone in those currencies as well.

Philadelphia Federal Reserve Pres. Harker made several noteworthy comments regarding monetary policy and economic forecasts. He emphasized the importance of closely monitoring data to determine if further policy tightening is necessary. Harker projected sluggish GDP growth below 1% for 2023, with a rise in the unemployment rate to 4.4%. In terms of inflation, he expects it to decrease to around 3.5% this year and 2.5% next year, ultimately reaching the Fed’s 2% target by 2025. Harker expressed optimism about the effectiveness of previous rate hikes, but also mentioned reports of decreased consumer spending. Given the circumstances, he suggested it would be prudent to skip a rate hike. He stated his belief that a recession is unlikely this year. May not

Meanwhile, the monthly ADP employment data was much better than expected,

- US ADP May employment report showed an increase of 278,000 jobs, surpassing the expected 170,000.

- Small businesses added 116,000 jobs, medium-sized firms added 112,000 jobs, and large businesses added 106,000 jobs.

- The previous month’s employment number was revised to +291,000, marking the best figure since June 2022.

Those numbers, initially led to a stronger dollar, but there was also a silver lining in the report, that reversed the dollar in short order. That hope, was in wage numbers within the report. The ADP chief economist said, “This is the second month we’ve seen a full percentage point decline in pay growth for job changers. Pay growth is slowing substantially, and wage-driven inflation may be less of a concern for the economy despite robust hiring.”

Later the quarterly productivity data also showed wage growth slowing. More specifically, unit labor costs came in at 4.2% which was much lower than the 6% expected.

The final positive came from the monthly PMI report. Manufacturing PMI for May came in at 46.9, slightly below the expected 47.0. However, it was the prices paid component of the PMI that was encouraging. It came in at 44.2, significantly lower than the estimated 52.0 and the previous month’s 53.2. Other details showed new orders declining to 42.6 from 45.7, indicating a contraction in demand. Supply deliveries, inventories, customer inventories, backlog of orders, and new export orders all declined as well, indicating overall weakness in the manufacturing sector. Employment showed a slight improvement, with a reading of 51.4 compared to 50.2 in the previous month, but if employment is growing (filling jobs) with steady wages, that is a good thing for inflation.

As a result, the dollar moved lower, as did yields. Looking at the yield curve:

- 2-year yield 4.347% -4.3 basis points

- 5-year yield 3.702% -4.0 basis points

- 10-year yield 3.604% -3.3 basis points

- 30-year yield 3.821% -3.6 basis points

Stocks liked the combination as it closed with gains in all three major indices. The Dow industrial average was up for only the 2nd time in 9 trading days. The NASDAQ index rose for the 4th time in 5 trading days and led the gains today.

- Dow industrial average rose 153.30 points or 0.47%

- S&P index rose 41.17 points or 0.98%

- NASDAQ index rose 165.69 points or 1.28%

Looking at individual stocks,

- Nvidia resumed its run to the upside with a gain of $19.36 or 5.12% at $397.70. It’s all about AI

- Microsoft moved up $4.19 or 1.28% at 332.58.

- Adobe, which recently introduced some advanced AI capabilities in it’s software, rose $8.96 or 2.14%. Adobe will not release earnings until June 15 (or thereabouts), but it’s shares are up 28.58% since May 12

- Meta rose $7.89 or 2.98% as they announced new a new VR product

- Apple rose $2.66 or 1.5%. It will have its worldwide developer conference on June 5 where they are expected to announce their own VR product

A snapshot of other markets as a market moves toward the US close shows:

- Crude oil is up $2.05 or 3.01% at $70.14. After moving to a low price yesterday of $67.03, the price has rebounded ahead of the OPEC+ on Sunday

- Spot gold reacted to the lower dollar and lower interest rates by rising $15 or 0.76% at $1977.82

- Silver is up $0.40 or 1.67% $23.88

- Bitcoin is trading at $26,850 which is just below its 100-day moving average at $26,883 but ahead of its 38.2% retracement of the range since the April low at $26,655.

Thank you for your support. For traders in the Asian session, have a good weekend.