Last week the CPI data in the U.S. came in above expectations with headline

inflation rising 0.4% and core CPI by 0.5%. The ECB hiked its interest rates by

50bps stressing that inflation is projected to remain too high and refrained

from signalling any future policy changes.

They also noted the high levels of uncertainty in the financial markets and

said it will take a data-dependent approach.

For this week, on Tuesday we’ll get the CPI print in Canada and the U.S.

existing home sales data. ECB President Lagarde will speak in a panel titled

“CBDCs: Keeping momentum in uncertain times” at the Bank of

International Settlement Innovation Summit in Basel.

This type of event is not expected to create market volatility, but it’s

worth keeping an eye on it in case she comments on the banking stress situation

or future rate hikes.

Wednesday will bring the U.K. CPI data and what is likely the week’s most

awaited event: the FOMC Policy Announcement and the Federal Funds Rates.

This will be followed by the SNB Monetary Policy Assessment, Policy Rate

and press conference on Thursday as well as the MPC official bank rate votes in

the U.K., the monetary policy summary and the official bank rate. In the U.S.,

the unemployment claims, and new home sales data will also be released.

On Friday we’ll get the flash manufacturing and flash services PMIs for the

euro area, U.K. and the U.S.

The CPI data for the Canadian economy is eagerly awaited as it will be the

last print before the next BoC meeting in April. The economy is holding up

reasonably well, but the tight labour market, elevated levels of inflation and

high wage growth might force the bank to resume its tightening cycle. As a

reminder, at the last meeting, the BoC decided to hold rates. The consensus for

the CPI y/y is to rise from 5.9% to 6.1% and the CPI m/m to also rise by 0.7%.

The BoC meeting minutes will be released the following day and might contain

clues about potential future rate hikes.

The CPI for the U.K. is expected to show signs of cooling down with the

consensus for m/m at -0.4%. A surprise on the downside will likely suggest the

BoE hiking cycle is nearing its end.

Wednesday’s FOMC decision and Chairman Powell’s press conference will be

the highlight of the week. The market consensus is for a 25bps hike, but swaps

indicate only 16bps of tightening is currently priced in at this time,

according to Scotiabank.

It will be interesting to see the Fed’s reaction to the current stress in

the banking sector combined with elevated levels of inflation. There are a few

analysts who argue that it would be appropriate for the Fed to hold or even cut

the rates.

However, rate cuts at the moment might be a reckless action especially with

the high inflation still looming. In conclusion, a 25bps hike seems to be the

base case as assessing the impact of the current banking sector events needs

more time.

At the SNB meeting analysts expect a 50bps or even a 75bps rate hike. In

Switzerland inflation remains high, but even though it’s not as high as in

other developed countries, the latest rise in domestic CPI is a cause for

concern.

The SNB estimated inflation for Q1 at 3.0%, but it currently sits above its

estimation, at 3.4%. This would justify a 75bps hike, but due to the Credit

Suisse turmoil, the bank might opt for a more moderate 50bps hike and see how

the situation evolves. As a reminder, the SNB also hiked the rate by 50bps in

December to 1%.

At this week’s BoE meeting the consensus is for a 25bps rate hike which is

supposed to be the last one. It will be interesting to watch what the Governor

has to say about the situation in the banking sector and the risk of contagion

as a consequence of Credit Suisse’s problems.

At the last ECB meeting President Lagarde went ahead with a 50bps hike

fearing that stepping back from its pace of tightening might spread fear among

investors, so BoE might follow the same reasoning.

Flash manufacturing and flash services PMIs for the eurozone have shown

signs of improvement since the beginning of the year. The softening energy prices

have given some relief to consumer purchasing power, adding some optimism about

the economy.

The consensus for the services PMI is 52.5, which is slightly below the

February print at 52.7, but still in expansion territory. The manufacturing

PMI, however, while recovering, remains in contraction overall, with 48.5 in

February and an expected moderate increase to 48.9 in March.

Everyone is looking for clues on how the banking sector woes might impact

businesses, but for now it’s too early to see it in the data.

For the U.K flash PMI, analysts will watch if the surprising increase in

February, which put the index into expansion territory at 53.1 for the first

time since July 2022, will continue, which could indicate further side of

activity recovery.

While still on the decline, the housing market situation in the U.S. started to

stabilize since the beginning of the year after a period of pressure due to

high mortgage rates. The consensus is

for a rise in existing home sales data for February, but new home sales are

expected to see a decline following the January 7.2% jump.

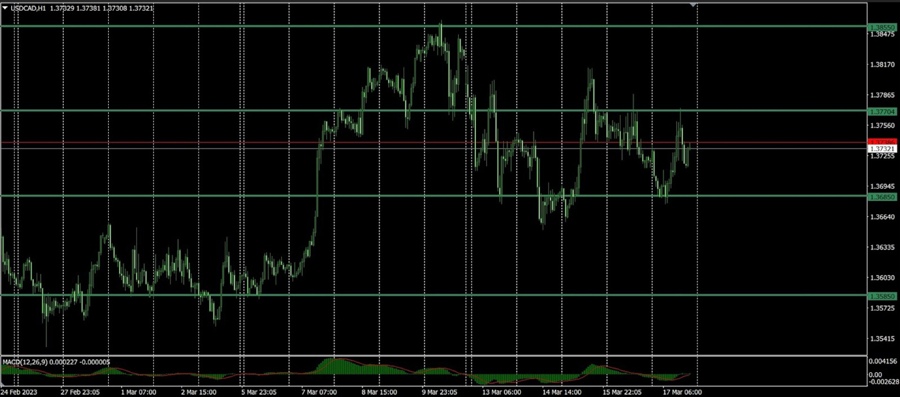

USD/CAD expectations

The pair ended the week without a clear direction and could continue to

move in a range. The FOMC meeting could cause some volatility, as well as the

CPI data in Canada if it surprises on the upside.

Overall, the USD/CAD has room for further appreciation. A hawkish tone from

the Fed coupled with the new Dot Plot might fuel an appreciation tendency as

investors seem to be indifferent to the CAD.

A correction is expected until the 1.3685 level of support and if that

level holds the next target could be the 1.3855 level of resistance.

On the downside, the next level of support is at 1.3585.

GBP/CHF expectations

On the H1 chart the pair closed the week near the 1.1310 level of

resistance. A bearish divergence seems to be forming that could suggest a

bigger correction until the 1.1160 level of support, if the fundamentals align.

If that level holds, the next target could be 1.1365. On the upside, the next

level of resistance is at 1.1435.

A risk for this trade is the BoE and the SNB monetary policy announcements.

This article was written by

Gina Constantin.