UPCOMING

EVENTS:

- Monday: BoJ Summary of Opinions. (US Holiday)

- Tuesday: UK Labour Market report, Eurozone ZEW, US NFIB

Small Business Optimism Index, Fed’s SLOOS. - Wednesday: Japan PPI, Australia Wage Price Index, US CPI.

- Thursday: Australia Labour Market report, UK GDP,

Eurozone Employment Change and Industrial Production, US PPI, US Jobless

Claims, Fed Chair Powell. - Friday: Japan GDP, China Industrial Production and

Retail Sales, US Retail Sales, US Industrial Production and Capacity

Utilization.

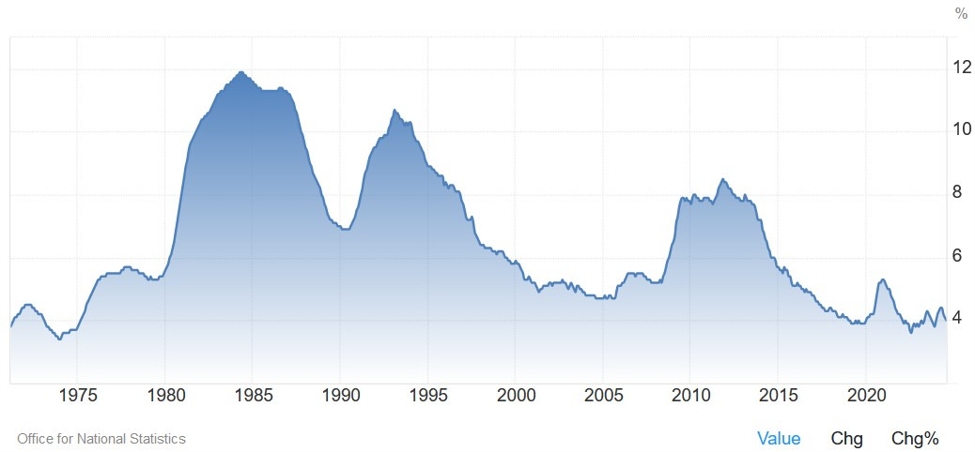

Tuesday

The UK Unemployment

Rate is expected to tick higher to 4.1% vs. 4.0% prior. The Average Earnings

incl. Bonus is expected at 3.9% vs. 3.8% prior, while the ex-Bonus measure is

seen at 4.7% vs. 4.9% prior.

The market sees

just a 20% chance of a 25 bps cut in December and, although a weak report might

raise the probabilities a bit, the market will likely focus more on the

inflation figures with two CPI reports left before the last BoE decision for

the year.

UK Unemployment Rate

Wednesday

The Australian Q3

Wage Price Index Y/Y is expected at 3.6% vs. 4.1% prior, while the Q/Q measure

is seen at 0.9% vs. 0.8% prior. The data is unlikely to change anything for the

RBA although lower readings would be welcomed.

Australia Wage Price Index YoY

The US CPI Y/Y is

expected at 2.6% vs. 2.4% prior, while the M/M measure is seen at 0.2% vs. 0.2%

prior. The Core CPI Y/Y is expected at 3.3% vs. 3.3% prior, while the M/M

figure is seen at 0.3% vs. 0.3% prior.

At the latest

Fed’s decision, Fed Chair Powell said that they expect bumps on inflation and

that one or two bad data months on inflation won’t change the process. This

keeps the 25 bps cut in December in place even if we get higher inflation

readings.

The market though

is forward-looking, and the rise in Treasury yields showed that the market sees

risks to the inflation outlook. Moreover, the red sweep could increase those

fears if the progress on inflation stalls, or worse, reverses.

Therefore, higher

inflation readings might not change the near-term monetary policy outlook, but

I personally see it changing the market’s outlook and eventually the Fed’s one.

US Core CPI YoY

Thursday

The Australian

Labour Market report is expected to show 25K jobs added in October vs. 64.1K in

September and the Unemployment Rate to tick higher to 4.2% vs. 4.1% prior. The

data is unlikely to change anything for the RBA but faster than expected

weakening could see the market pricing in more aggressive rate cuts in 2025,

much like it did with the RBNZ.

Australia Unemployment Rate

The US PPI Y/Y is

expected at 2.3% vs. 1.8% prior, while the M/M measure is seen at 0.2% vs. 0.0%

prior. The Core PPI Y/Y is expected at 3.0% vs. 2.8% prior, while the M/M

figure is seen at 0.3% vs. 0.2% prior.

This report will

likely be seen in light of the US CPI data releases the day before and it might

add to the angst around inflation if both come out higher than expected.

US Core PPI YoY

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

after an improvement in the last two months, spiked to the cycle highs in the

last couple of weeks due to distortions coming from hurricanes and strikes.

This week Initial

Claims are expected at 224K vs. 221K prior, while there’s no consensus for

Continuing Claims at the time of writing although the prior reading saw an

increase to 1892K vs. 1852K prior.

US Jobless Claims

Friday

The US Retail

Sales M/M is expected at 0.3% vs. 0.4% prior, while the ex-Autos M/M measure is

seen at 0.3% vs. 0.5% prior. The focus will be on the Control Group figure

which is expected at 0.3% vs. 0.7% prior.

Consumer spending

has been stable which is something you would expect given the positive real

wage growth and resilient labour market. We’ve also been seeing a steady pickup

in the UMich Consumer

Sentiment which suggests

that consumers’ financial situation is stable/improving.

US Retail Sales YoY