Dollar remains the top performer for the week, despite a mild pullback today. Sterling jumped into second place, buoyed by stronger-than-expected UK retail sales data. Meanwhile, Canadian Dollar holds third position, although its momentum has waned, suggesting it could slip before the weekly close.

On the weaker side, Swiss Franc continues to lag behind, marking the worst performance of the week. Euro follows closely as the second weakest currency, weighed down by dovish tone of ECB’s rate cut yesterday. Japanese Yen also struggles, ranking third worst, despite verbal interventions by Japanese officials aimed at stabilizing the currency.

Both Australian and New Zealand Dollars are taking a breather from recent losses, supported by a rebound in Chinese markets. However, overall market sentiment suggests that risk-sensitive currencies like Aussie and Kiwi will continue to face pressure amid ongoing global uncertainties.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is up 0.41%. CAC is up 0.78%. UK 10-year yield is down -0.0245 at 4.075. Germany 10-year yield is down -0.022 at 2.195. Earlier in Asia, Nikkei rose 0.18%. Hong Kong HSI rose 3.61%. China Shanghai SSE rose 2.91%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.0051 to 0.970.

UK retail sales rises 0.3% mom in Sep, extended rebound in consumption

UK retail sales volumes rose by 0.3% mom in September, defying expectations of -0.3% decline. This marked the highest retail sales index level since July 2022, reflecting stronger-than-anticipated rebound in consumer activity.

Looking at the broader picture, sales volumes in Q3 surged by 1.9% compared to Q2, the joint-largest quarterly rise since July 2021. This upward momentum, shared with March 2024.

BoJ’s Ueda stresses vigilance amid global uncertainty, cautions on market volatility

In a speech today, BoJ Governor Kazuo Ueda highlighted the persistent uncertainties surrounding Japan’s economic recovery and global market conditions, urging caution in assessing the outlook.

Ueda emphasized the “still high” level of unpredictability in the overseas economic environment, particularly noting volatility in key markets such as the US.

“The overseas economic outlook, including that for the United States, remains uncertain, while market moves continue to be unstable,” Ueda remarked.

“We must closely monitor such developments with high vigilance, and scrutinize their fallout on Japan’s economic and price outlook,” he said, underlining that Japan’s recovery remains fragile and exposed to global economic shifts.

Japan’s CPI core slows to 2.4%, core-core edges up

Japan’s core CPI, which excludes fresh food, eased from 2.8% yoy to 2.4% yoy in September, slightly above expectations of 2.3% yoy. Despite the slowdown, core inflation has remained above BoJ’s 2% target for well over two years.

The deceleration in price gains is largely attributed to government utility subsidies, which have helped lower household expenses. Headline CPI fell from 3.0% yoy to 2.5%, with gas prices subtracting 0.55 percentage points from the overall figure. This indicates that without government intervention, inflation would have remained higher.

Meanwhile, CPI measure that excludes both food and energy costs—often referred to as core-core CPI—increased from 2.0% yoy to 2.1% yoy, suggesting underlying inflation remains firm. However, service prices saw a slight decrease in momentum, slowing from 1.4% yoy to 1.3% yoy.

China’s Q3 GDP growth slows to 4.6%, stimulus impact yet to solidify

China’s economy grew 4.6% yoy in Q3, slowing slightly from 4.7% in Q2 but in line with market expectations. This marks the slowest pace of growth since early 2023, as external pressures and a challenging global environment continue to weigh on the country’s economic performance. On a quarterly basis, GDP expanded by 0.9%.

The National Bureau of Statistics noted that the economy remained “generally stable with steady progress,” highlighting continued increase in production and demand, alongside stable employment and prices.

The NBS emphasized that the effects of the government’s stimulus policies were beginning to show, with “major indicators displaying positive changes recently.”

However, the bureau also cautioned that the external environment was becoming “increasingly complicated and severe,” underscoring the need to further solidify the foundation for sustained recovery.

Key economic data released alongside the GDP report suggested signs of resilience in some sectors. Industrial production increased by 5.4% yoy in September, surpassing expectations of 4.6% yoy. Retail sales also exceeded forecasts, rising 3.2% yoy compared to the expected 2.4% yoy. Fixed asset investment saw a 3.4% year-to-date increase, slightly above 3.3% expected by analysts.

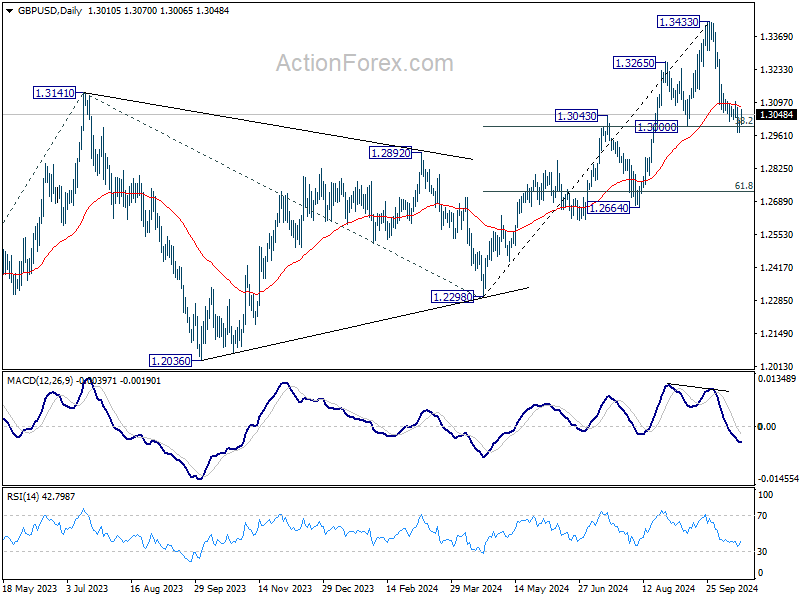

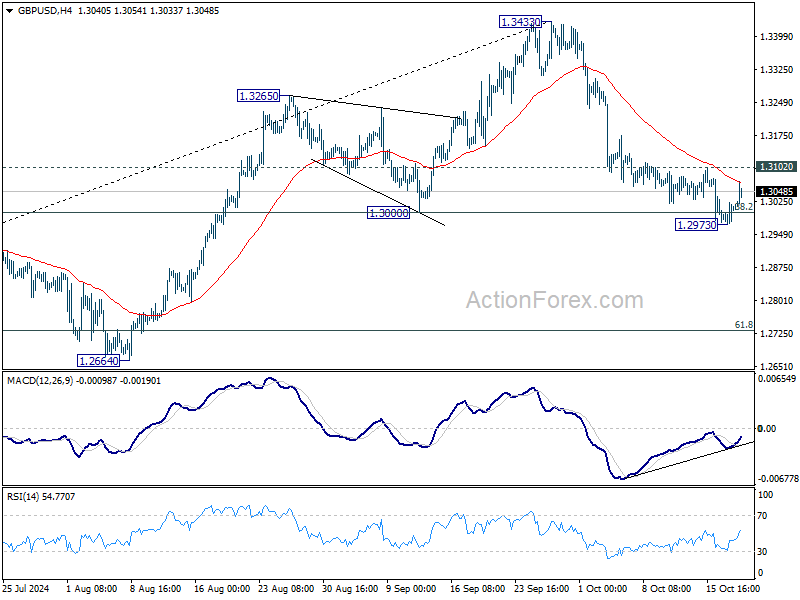

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2982; (P) 1.3003; (R1) 1.3031; More…

Intraday bias in GBP/USD remains neutral for the moment. On the downside, sustained trading below 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) will argue that whole rise from 1.2298 has completed and bring deeper fall to 61.8% retracement at 1.2732. Nevertheless, strong bounce from current level, followed by break of 1.3102 minor resistance, will turn bias back to the upside for stronger rebound towards 1.3433.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.