Dollar is struggling to find a clear direction after a set of contrasting economic data sent mixed signals to the markets. On one side, inflationary pressures remain elevated, especially with core inflation ticking up, signals that Fed won’t be able to accelerate its policy easing. On the other hand, the unexpectedly sharp rise in initial jobless claims has sparked concerns about amore severe slowdown in the employment market.

Market expectations for Fed remain largely unchanged, with Fed funds futures still pricing in over 80% probability of a 25 bps rate cut in both November and December. Beyond these two meetings, however, the future path of monetary easing looks even more uncertain now.

For the day, Japanese Yen leads in strength, supported by comments from a top BoJ official signaling that more rate hikes could still be on the table. Swiss Franc is the second strongest, followed by New Zealand Dollar. Conversely, Canadian Dollar is the weakest, trailed by Euro and British Pound, while Dollar and Australian Dollar are mixed in middle positions.

Looking at the broader picture for the week, Dollar continues to lead as the strongest currency, followed by Swiss Franc and Yen. Commodity currencies, including the New Zealand Dollar, Canadian Dollar, and Australian Dollar, remain under pressure. Euro and Sterling are in the middle of the pack.

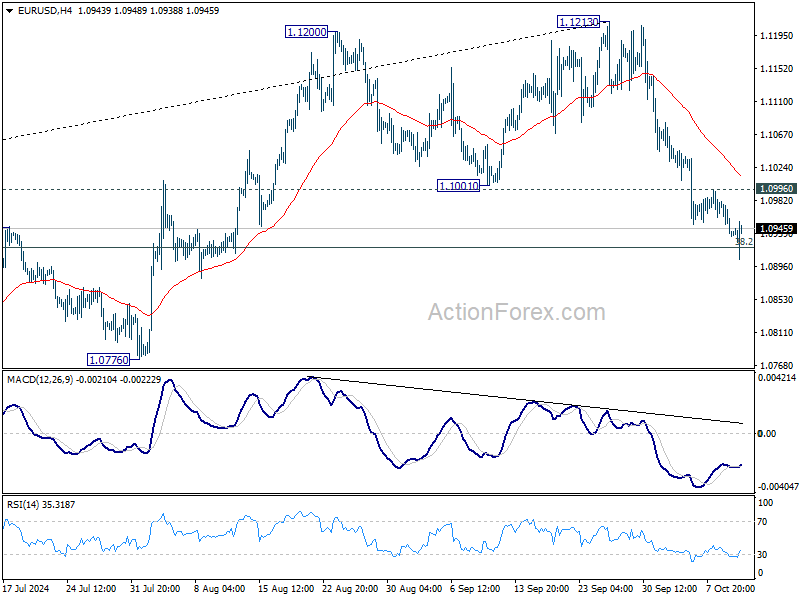

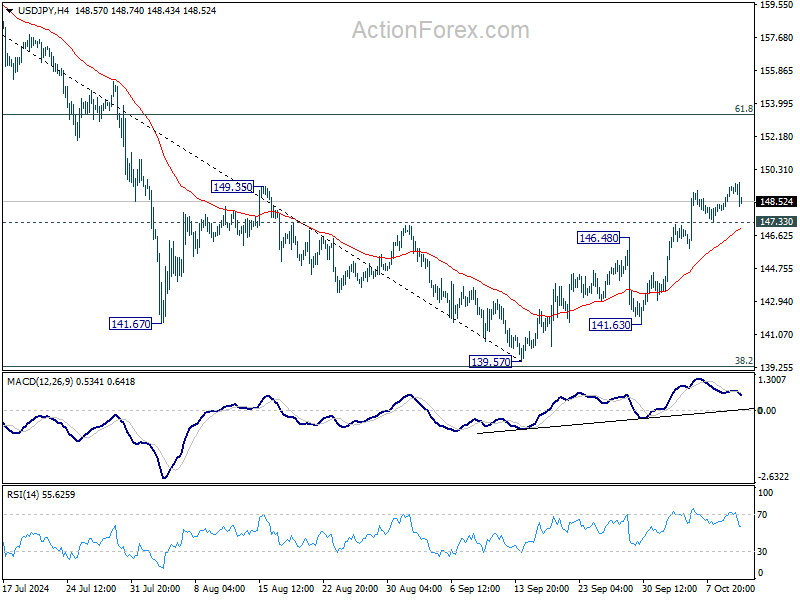

Technically, as there is prospect of deeper retreat in Dollar, here are some levels to watch, including 1.0996 minor resistance in EUR/USD. 1.3174 minor resistance in GBP/USD, 0.8529 minor support in USD/CHF, and 147.33 minor support in USD/JPY. Dollar’s near term rally would still be intact if these levels hold. But firm break of them, in particular if simultaneously, will indicate that Dollar selloff has returned.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is down -0.07%. CAC is down -0.23%. UK 10-year yield is up 0.021 at 4.206. Germany 10-year yield is up 0.002 at 2.265. Earlier in Asia, Nikkei rose 0.26%. Hong Kong HSI rose 2.98%. China Shanghai SSE rose 1.32%. Singapore Strait Times fell -0.29%. Japan 10-year JGB yeld rose 0.0252 to 0.959.

US CPI slows to 2.4% yoy in Sep, but core CPI rises to 3.3% yoy

US CPI rose 0.2% mom in September, above expectation of 0.1% mom. CPI core (less food and energy) rose 0.3% mom, above expectation of 0.2% mom, and Shelter costs rose 0.2% mom. Food prices rose 0.4% mom. Together, these two indexes contributed over 75 percent of the monthly all items increase. Energy index fell -1.9% mom.

Over the 12-month period, CPI ticked down from 2.5% yoy to 2.4% yoy, above expectation of 2.3% yoy. That’s still the lowest level since February 2021. CPI core ticked up from 3.2% yoy to 3.3% yoy, above expectation of 3.2% yoy. Energy index fell -6.8% yoy while food index rose 2.3% yoy.

US initial jobless claims surges to 258k, highest since mid-2023

US initial jobless claims jumped sharply by 33k to 258k in the week ending October 5, well above expectation of 231k. That’s also the highest level since mid-2023. Four-week moving average of initial claims rose 7k to 231k.

Continuing claims rose 42k to 1861k in the week ending September 28. Four-week moving average of continuing claims rose 4.5k to 1832k.

ECB Minutes: Caution on inflation as rate cuts expected to continue

Following the ECB’s 25bps rate cut in September, the minutes reveal a cautious stance on future monetary easing, emphasizing the need to rely on a broader evaluation of data, rather than any single metric. While members agreed that further reductions in policy restrictiveness would depend on incoming data, they stressed that “data-dependence” should not be misinterpreted as “data point-dependence” , and mechanical response to short-term inflation figures.

The committee highlighted that a “gradual and cautious approach” remains appropriate, as uncertainties around inflation persist. Despite some signs of improvement, it is still too early to declare the inflation battle won. Concerns over upward revisions in core inflation projections and recent surprises in services inflation were also noted.

ECB emphasized that the “real test” of inflation stability would come in 2025, when the impact of wage growth and productivity gains would be clearer.

For now, markets expect another rate cut at the upcoming October meeting, with a follow-up move in December also largely anticipated.

BoJ’s Himino: Rate hikes to continue if economic outlook aligns

BoJ Deputy Governor Ryozo Himino made it clear at a conference today that the central bank if the economic and price forecasts outlined in the July Outlook Report are realized, “the bank will accordingly continue to raise the policy interest rate and adjust the degree of monetary accommodation.”

He emphasized that future decisions will be data-dependent, with each meeting assessing the evolving outlook, stating that the BoJ is “not on a preset course.”

Himino addressed the surprise and market disruption following BoJ’s unexpected rate hike in July, acknowledging that the central bank faced criticism for its communication approach.

He conceded, “There’s no silver bullet to improving communications,” but stressed the bank’s strong commitment to refining how it conveys policy decisions to the markets.

Japan’s PPI rises 2.8% yoy in Sep, import prices tumble

Japan’s PPI rose by 2.8% yoy in September, a notable increase from the previous month’s 2.6% yoy and well above the market’s expectation of 2.3% yoy.

A significant development was the shift in import prices. Yen-based import price index dropped sharply by -2.6% yoy, turning negative for the first time in eight months. This is a stark reversal from the 10.7% yoy rise recorded as recently as July. Export prices also followed a similar downward trend, falling by -1.0% yoy after previously rising by 2.5% yoy.

On a month-over-month basis, PPI remained flat at 0.0% mom, while yen-based import price index decreased by -2.9% mom, and the export price index fell by -1.7% mom. The decline in both import and export prices reflects a combination of softer global demand and a stronger Yen.

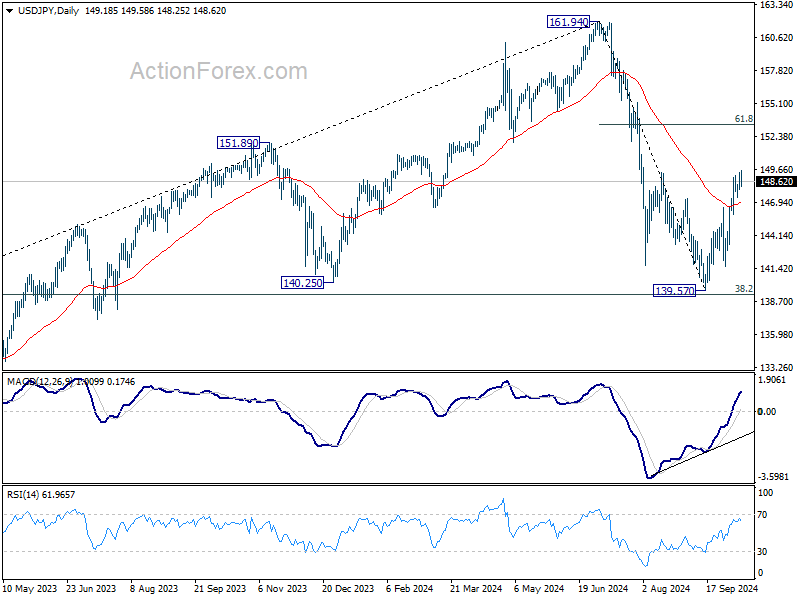

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.43; (P) 148.89; (R1) 149.78; More…

USD/JPY dips in early US session but stays above 147.33 minor support. Intraday bias stays on the upside, as rise from 139.57 short term bottom is still in progress. Current rally is seen as the second leg of the corrective pattern from 161.94. Next target is 61.8% retracement of 161.94 to 139.57 at 153.39. On the downside, below 147.33 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should now be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.