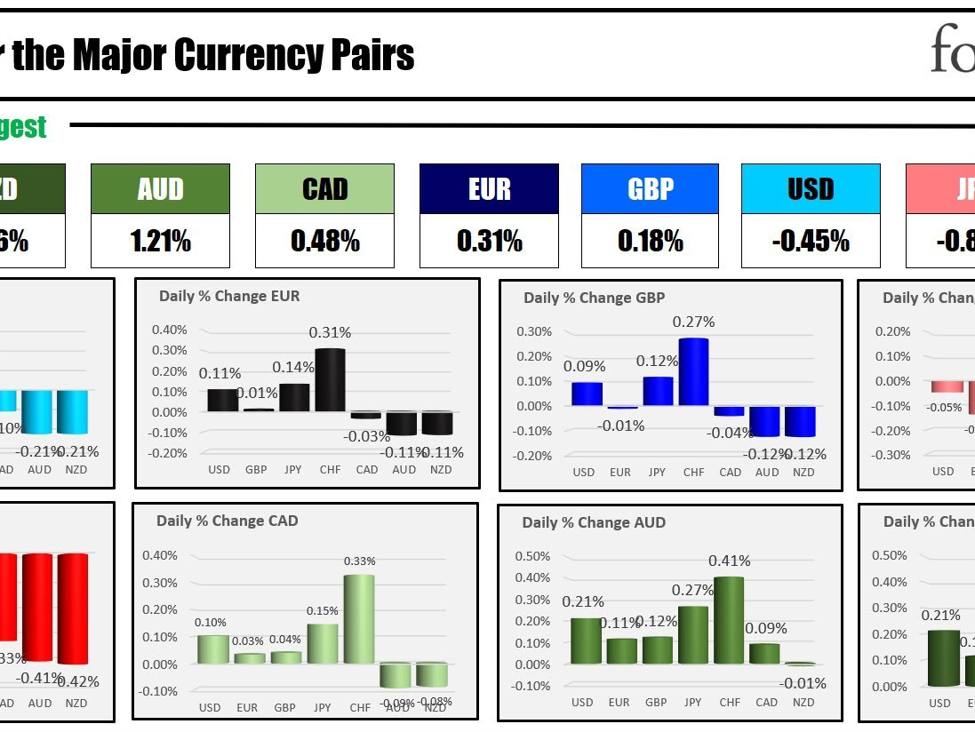

The NZD is the strongest and the CHF is the weakest as the NA session begins. The USD is mixed to lower to start the North American session.

The ECB will announce at their rate decision with expectations of no change in policy. That will take place at 8:15 AM ET. ECB Pres. Lagarde will follow-up the rate decision with her press conference which will commence at 8:45 AM ET. Justin Low, pointed out that the focus will be on ECB President Lagarde’s press conference, where there are two main scenarios that could notably impact markets:

- Explicit Ruling Out of Rate Cuts: If Lagarde explicitly states there will be no rate cuts in March and April, it could affect market reactions. Current trader expectations include a 71% likelihood of a 25 basis points cut in April. Factors Lagarde might mention include developments in the Red Sea, wage pressure outlooks, or dissatisfaction with the current disinflation narrative. The tone of her remarks will be crucial; any perceived timidity could alter market expectations.

- Vagueness on Rate Cuts: If Lagarde is vague and leaves open the possibility of a rate cut in March or April, it could lead to a depreciation of the euro and potentially prompt traders to fully price in a rate cut for April. This scenario might also provide a slight boost to risk assets.

The most likely outcome is a muted market reaction. Lagarde is expected to emphasize a data-dependent approach, offering mild pushback against current market pricing. She may not explicitly rule out an April rate cut but could suggest it might be appropriate “by the summer.”

Lagarde is also expected to acknowledge recent improvements in inflation but will likely argue that the ECB’s job is not complete and that price pressures may persist for a while.

Between the ECB decision and the press conference will be a slew of economic data out of the US including the fourth-quarter advanced GDP report which is expected at 2.0% (versus 4.9% in 3Q). The largely followed Atlanta Fed GDPNow model forecasts a rise of 2.4%. Also released at 8:30 AM ET will be durable goods with expectations of 1.1% versus 5.4% last month. The ex transportation durable goods are expected to increase by 0.2% versus 0.5% last month. US trade data is expected at $-88.7 billion versus $-90.3 billion last month and preliminary wholesale mentors are expected to decline by -0.2%.

US building permits were just released early at 1.493 million units versus 1.467 million last month. That was up 1.8% the month.

Yesterday after the close, Tesla reported disappointing results and warned of a slowdown going forward. Tesla shares in premarket training are down $-17 or -8.17%.

Looking at a sampling of earnings released this morning, there is a mixture of good and bad (see results below).

Marsh & McLennan Companies Inc (MMC) Q4 2023:

- Beat Expectations: Adjusted EPS of $1.68 (expected $1.63).

- Met Expectations: Revenue of $5.55 billion (expected $5.54 billion).

Sherwin-Williams Co (SHW) Q4 2023:

- Beat Expectations: EPS of $1.81 (expected $1.80).

- Beat Expectations: Revenue of $5.25 billion (expected $5.22 billion).

American Airlines Group Inc (AAL) Q4 2023:

- Beat Expectations: Revenue of $13.06 billion (expected $13.02 billion).

Comcast Corp (CMCSA) Q4 2023:

- Beat Expectations: Adjusted EPS of $0.84 (expected $0.79).

- Beat Expectations: Revenue of $31.25 billion (expected $30.51 billion).

Blackstone Inc (BX) Q4 2023:

- Beat Expectations: EPS of $1.11 (expected $0.95).

- Missed Expectations: Revenue of $1.29 billion (expected $2.57 billion).

Northrop Grumman (NOC) Q4 2023:

- Missed Expectations: Adjusted EPS of -$1.45 (expected $5.80).

- Beat Expectations: Revenue of $10.6 billion (expected $10.44 billion).

Humana (HUM):

- Adjustment Announcement: No longer believes the adjusted EPS target for 2025 of $37/share is achievable.

Valero Energy Corp (VLO) Q4 2023:

- Beat Expectations: Adjusted EPS of $3.55 (expected $2.95).

- Missed Expectations: Revenue of $35.41 billion (expected $35.69 billion).

Southwest Airlines Co (LUV) Q4 2023:

- Beat Expectations: Adjusted EPS of $0.37 (expected $0.12).

- Beat Expectations: Revenue of $6.82 billion (expected $6.74 billion).

Humana Inc (HUM) Q4 2023:

- Missed Expectations: EPS of -$0.11 (expected *$0.17).

- Beat Expectations: Revenue of $25.73 billion (expected $25.42 billion).

Mobileye Global Inc (MBLY) Q4 2023:

- Beat Expectations: EPS of $0.28 (expected $0.27).

- Missed Expectations: Revenue of $0.637 billion (expected $0.64 billion).

Dow Inc (DOW) Q4 2023:

- Beat Expectations: EPS of $0.43 (expected $0.40).

- Beat Expectations: Revenue of $10.62 billion (expected $10.37 billion).

After the close today Intel, Visa and T-Mobile will announce their earnings. On Friday morning American Express will announce. Next week is the big week with Microsoft, Apple, Alphabet, and Amazon all on the schedule.

Crude oil is higher in premarket trading and extended to $76.37 at session highs. That was the highest level since December 1. The 200 day moving average looms above at $77.61.

US stocks are mixed after mixed results yesterday with the Dow Industrial Average lower and the S&P and NASDAQ index higher (each for the fifth consecutive day). The S&P has made new all-time highs for four consecutive days running.

A snapshot of the markets as the North American session begins currently shows:

- Crude oil is trading up $0.70 or 0.93% at $75.78. At this time yesterday, the price was at $74.16

- Gold is trading up $0.49 or 0.02% at $2013.95. At this time yesterday, it was trading at $2033.09

- Silver is trading up $0.19 or 0.84% at $22.83. At this time yesterday, it was trading at $22.75

- Bitcoin traded at $39,867. At this time yesterday, the price was trading much lower at $40,173. The high price after the Bitcoin ETFs were approved for trading reached $49106.

In the premarket for US stocks, the major indices are mixed. Yesterday, the major indices closed mixed with the Dow Industrial Average lower, but the S&P and NASDAQ closing higher for the fourth consecutive day. The S&P index closed at another record level:

- Dow Industrial Average futures are implying a decline of -14.25 points. Yesterday, the index fell – -99.06 points or -0.26%

- S&P futures are implying a gain of 2.24 points. Yesterday, the index rose 3.93 points or 0.08%

- Nasdaq futures are implying a gain of 31.05 points. Yesterday, the index rose 55.97 points or 0.36%

In the European equity markets, the major indices are trading lower:

- German DAX, -0.52%

- France CAC -0.54%

- UK FTSE 100 -0.20%

- Spain’s Ibex -1.07%

- Italy’s FTSE MIB -4.04% (delayed by 10 minutes).

Shares in the Asian Pacific markets were higher as the market reacted further to the PBOC decline in the reserve rate requirement as the central bank tries to inflate stocks and the economy post Covid.

- Japan’s Nikkei 225, +0.03%

- China’s Shanghai composite index , +3.03%

- Hong Kong’s Hang Seng index, +1.96%

- Australia S&P/ASX, +0.48%

Looking at the US debt market, yields are trading mixed with the shorter end marginally higher and the longer end lower:

- 2-year yield 4.384% +0.6 basis points. Yesterday at this time, the yield was at 4.315%

- 5-year yield 4.076% +0.3 basis points. Yesterday at this time, the yield was at 4.013%

- 10-year yield 4.168% -1.0 basis points. Yesterday at this time, the yield was at 4.103%

- 30-year yield 4.391%, -2.3 basis. Yesterday at this time, the yield was at 4.341%

- The 2-10 year spread is at -21.8 basis points. At this time yesterday, the spread was at – -21.1 basis points

- The 2-30 year spread is at +0.8 basis points. At this time yesterday, the spread was at +2.8 basis points.

In the European debt market, the benchmark 10-year yields are mostly lower: