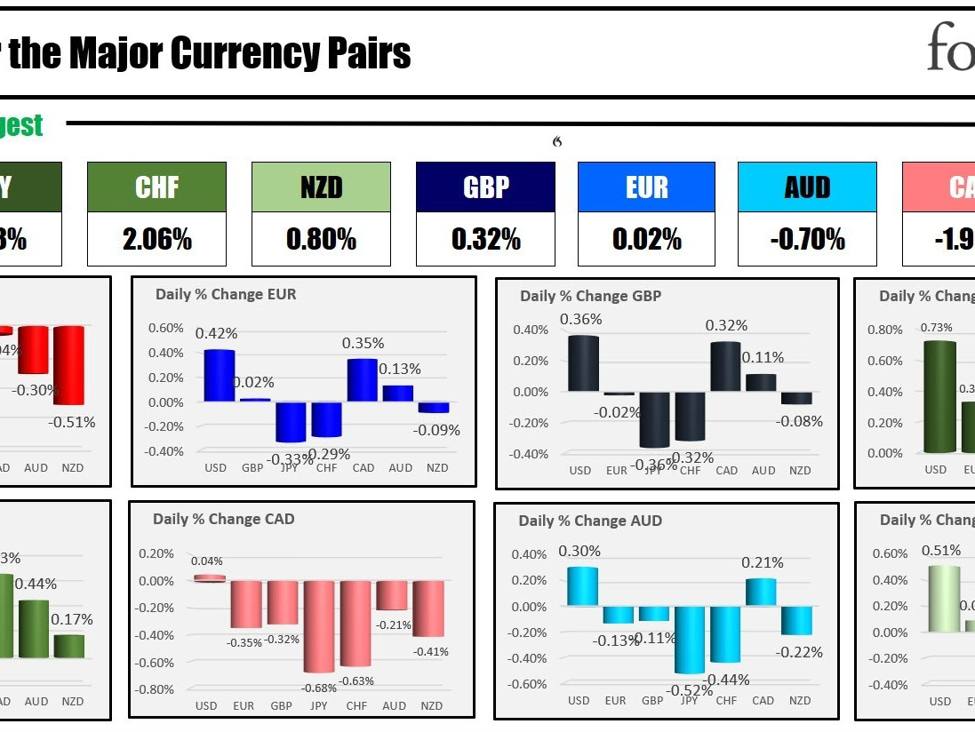

The strongest to the weakest of the major currencies

The JPY is the strongest and the USD is the weakest at the US session begins. The USD has been hit after gains yesterday did not get follow-through price action:

- The EURUSD Fell below its 200-day MA intraday yesterday (that MA is at 1.0844), but bounced near a swing target between 1.0803 and 1.0825, moved back above the 200-day MA and sellers turned to buyers. The price moved above the 200-hour MA at 1.0896, but the price has recently moved back below that MA and trades between the 100-hour MA below at 1.0870 and the 200-hour MA at 1.0896.

- The USDJPY yesterday extended above a swing area up to 148.59 but fell short of the high price from last week at 148.802. Today, the process reversed lower and in the process moved back below is 100-day moving average at 147.566, and tests its rising 200-hour moving average at 147.25. The price is not traded materially below that moving average since January 2.

- The GBPUSD continues its up-and-down trading fell below its 200 and 100-hour moving averages, and also below the 50% midpoint of the move up from the December low at 1.26622. However, the price snapped back higher in late US trading yesterday. In the Asian session, the price moved back above its near-converged 100 and 200-hour moving averages around 1.2700 and tilted the bias back in the upper direction. the price extended to a level at 1.2772, and backed off. The price is back down at 1.2740 currently.

Meanwhile, the improved risk appetite was partly due to an announcement from China’s People’s Bank of China (PBOC). The PBOC declared a substantial 50 basis points (bps) reduction in the Reserve Requirement Ratio (RRR), set to commence on February 5th. Although this measure is not as extensive as the previously promised $268 billion stock market support, it still represents a significant move. For context, the PBOC only reduced the RRR twice in the previous year, with each reduction being 25 bps. These reductions occurred once in March and then again in September. Asian Pacific shares were supported.

In other economic news, the PMI data in Europe this morning was mixed. Below is a summary for each of the major countries with the mixture of BEAT and MISSED from the results:

French Flash Manufacturing PMI

- Actual: 43.2, Forecast: 42.5, Previous: 42.14

- Result: BEAT expectations, IMPROVED compared to previous

French Flash Services PMI

- Actual: 45.0, Forecast: 46.1, Previous: 45.74

- Result: MISSED expectations, DECLINED compared to previous

German Flash Manufacturing PMI

- Actual: 45.4, Forecast: 43.7, Previous: 43.34

- Result: BEAT expectations, IMPROVED compared to previous

German Flash Services PMI

- Actual: 47.6, Forecast: 49.3, Previous: 49.34

- Result: MISSED expectations, DECLINED compared to previous

EU Flash Manufacturing PMI

- Actual: 46.6, Forecast: 44.8, Previous: 44.44

- Result: BEAT expectations, IMPROVED compared to previous

EU Flash Services PMI

- Actual: 48.4, Forecast: 49.1, Previous: 48.84

- Result: MISSED expectations, DECLINED compared to previous

UK Flash Manufacturing PMI (Country not specified)

- Actual: 47.3, Forecast: 46.7, Previous: 46.24

- Result: BEAT expectations, IMPROVED compared to previous

UK Flash Services PMI (Country not specified)

- Actual: 53.8, Forecast: 53.1, Previous: 53.44

- Result: BEAT expectations, IMPROVED compared to previous

Today, US yields are lower (after gains yesterday). Stocks are higher in pre-market trading. The European equities are also trading higher. The S&P and Nasdaq are working on 4 days of gains. Yesterday, the Dow fell snapping its 3 day win streak as 3M earnings disappointed and added to the negative bias in the Dow 30.

In the US, their flash PMI data will be released at 9:45 AM ET with manufacturing at 47.6 versus 47.9 last month. Services is expected at 51.4 versus 51.4 last month.

Also at 9:45 AM ET, the Bank of Canada will announce their decision with no change expected (main at 5.0%. The subsequent press conference will begin at 10:30 AM. What can be expected from BofA? CLICK HERE.

After the close yesterday Netflix earnings came in lower-than-expected but there was a huge subscriber surge. That has the stock currently trading up 9.82%.

Earnings results this morning shows:

-

General Dynamics Corp (GD)

- EPS: $3.64 (expected $3.68) – MISSED

- Revenue: $11.67 billion (expected $11.37 billion) – BEAT

-

Kimberly-Clark Corp (KMB)

- EPS: L51 (expected $1.54) – Unclear due to unclear EPS data.

- Revenue: $5.0D billion (expected $4.98 billion) – Assuming typo, BEAT

-

AT&T Inc (T)

- EPS: $0.54 (expected $0.56) – MISSED

- Revenue: $32.022 billion (expected $31.48 billion) – BEAT

-

Elevance Health (ELV)

- EPS: $5.62 (expected $5.64) – MISSED

- Revenue: $42.5 billion (expected $42.09 billion) – BEAT

- After the close today, some key releases could have a market impact:

- Tesla

- IBM

- ServiceNow, and

- Lam Research

A snapshot of the markets as the North American session begins currently shows:

- Crude oil is trading down $-0.20 or -0.25% at $74.16. At this time yesterday, the price was at $74.12

- Gold is trading up $4.01 or 0.20% at $2033.09. At this time yesterday, it was trading at $2024.88

- Silver is trading $0.32 or 1.46% at $22.75. At this time yesterday, it was trading at $22.27

- Bitcoin traded at $40,173. At this time yesterday, the price was trading much lower at $38,748. The high price after the Bitcoin ETFs were approved for trading reached $49106.

In the premarket for US stocks, the major indices are trading higher. Yesterday, the major indices closed mixed with the Dow Industrial Average lower, but the S&P and NASDAQ closing higher for the fourth consecutive day. The S&P index closed at another record level:

- Dow Industrial Average futures are implying a gain of 108 points. Yesterday, the index fell -96.36 points or -0.25%

- S&P futures are implying a gain of 22.15 points. Yesterday, the index rose 14.17 points or 0.29%

- Nasdaq futures are implying a gain of 142.04 points. Yesterday, the index rose 65.66 points or 0.43%

In the European equity markets, the major indices are trading higher:

- German DAX, +1.30%

- France CAC +0.02%

- UK FTSE 100 +0.34%

- Spain’s Ibex +0.03%

- Italy’s FTSE MIB +0.71% (delayed by 10 minutes).

Shares in the Asian Pacific markets were mixed, but the downtrodden Hang Seng index did rise by the most since November 15.

- Japan’s Nikkei 225, -0.80%

- China’s Shanghai composite index , +1.80%

- Hong Kong’s Hang Seng index, +3.56%

- Australia S&P/ASX, +0.06%

Looking at the US debt market, yields are trading higher:

- 2-year yield 4.315% -3.2 basis points. Yesterday at this time, the yield was at 4.408%

- 5-year yield 4.013% -3.9 basis points. Yesterday at this time, the yield was at 4.052%

- 10-year yield 4.103% -3.9 basis points. Yesterday at this time, the yield was at 4.130%

- 30-year yield 4.341% -3.7 basis points. Yesterday at this time, the yield was at 4.353%

- The 2-10 year spread is at -21.1 basis points. At this time yesterday, the spread was at -27.6 basis points

- The 2-30 year spread is at +2.8 basis points. At this time yesterday, the spread was at -5.4 basis points. At session highs last week, the spread got to +7.5 basis points

In the European debt market, the benchmark 10-year yields are mostly lower:

European benchmark 10 year yields