The selloff in Dollar overnight didn’t last very long. The greenback is trying to recovery in Asian session, as traders turned cautious on news that Poland was struck by a Russia-made projectile. But overall trading is subdued so far. Aussie and Kiwi are the strongest ones for the week at this point, supported by optimism over China reopening. Yen and Swiss Franc are the weakest on positive risk sentiment. Dollar, Euro and Sterling are mixed. Focuses will now turn to inflation data from the UK and Canada.

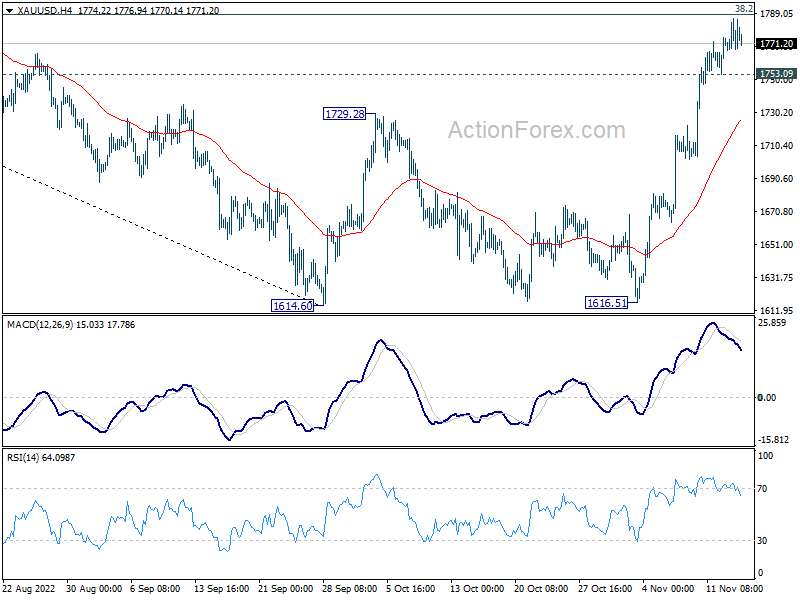

Technically, some attention will stay on Gold to gauge whether Dollar is ready for recovery. Gold is clearly losing upside momentum as seen in 4 hour MACD, as it approaches 38.2% retracement of 2070.06 to 1614.60 at 1788.58. Break of 1753.09 minor support will indicate that a temporary top is at least in place. Deeper decline would then be seen back to 4 hours 55 EMA (now at 1726.20).

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.13%. Hong Kong HSI is down -1.14%. China Shanghai SSE is down -0.22%. Singapore Strait Times is down -0.05%. Japan 10-year JGB yield is up 0.0008 at 0.245. Overnight, DOW rose 0.17%. S&P 500 rose 0.87%. NASDAQ rose 1.45%. 10-year yield dropped -0.066 to 3.799.

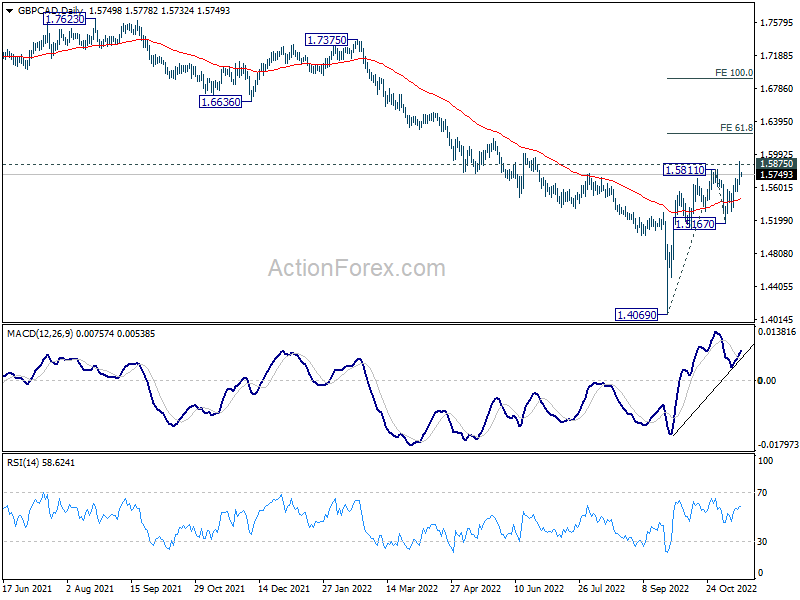

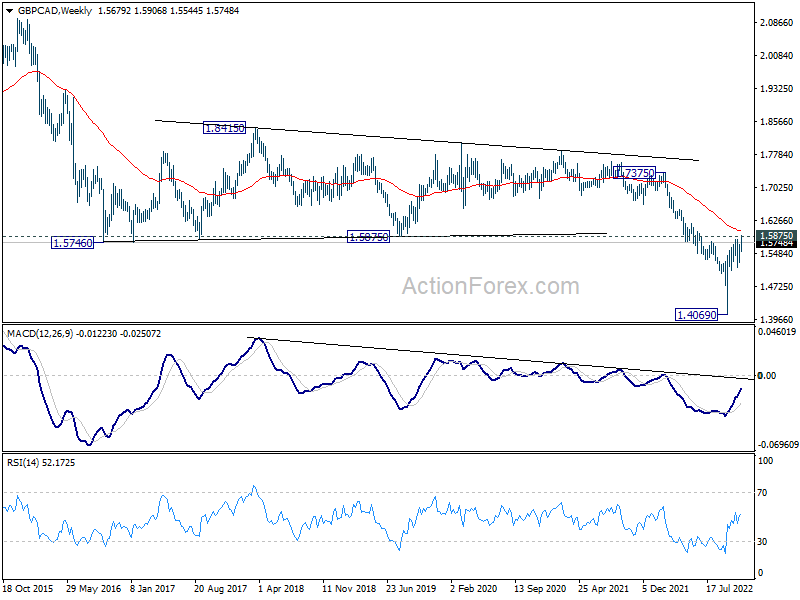

GBP/CAD pressing key resistance ahead of UK and Canada CPI

GBP/CAD is a pair to watch today with inflation data from the UK and Canada featured. The cross tried to resume the rise from 1.4069 this week, and breached 1.5811 resistance. Yet, there is no clear follow through buying so far.

Looking at the bigger picture, it’s now pressing an important resistance at 1.5875 (2019 low). 55 week EMA (now at 1.6012) is also in proximity. Rejection by this resistance zone, followed by break of 1.5167 support, will keep medium term outlook neutral-to-bearish.

However, sustained break of the resistance will solidify the case of bullish trend reversal. Further break of 61.8% projection of 1.4069 to 21.5811 from 1.5167 at 1.6244 will likely prompt upside acceleration to 100% projection at 1.6909.

{kind=link}

{kind=link}

Japan machine orders dropped -4.6% mom in Sep

Japan private-sector machine orders dropped sharply by -4.6% mom in September, much worse than expectation of 0.7% mom. That followed a -5.8% mom decline in August.

Nevertheless, for October-December period, manufacturers surveyed by the Cabinet Office are expecting core orders to rise 3.6%.

The government also downgraded its view on machinery orders to “recovery is stalling”, from “economy was picking up”.

Australia Westpac leading index signals sustained weak growth next year

Australia Westpac Leading Index dropped from -1.09% to -1.19% in October, a new post-pandemic low. Westpac said the is consistent with “sustained weak growth” in 2023. It expects GDP growth to slow from around 3.4% in 2022 to just 1% next year.

It added, “key drivers of the slowdown are: monetary policy tightening; falling commodity prices; and softness in jobs growth as capacity constraints bite.”

Regarding RBA policy, Westpac expects another 25bps rate hike at the December 6 meeting. And, “a mooted pause in the tightening is unlikely to occur in 2022 or the early months of 2023 as the Bank continues to underperform its inflation objectives.”

Looking ahead

Inflation data from the UK is the major focus in European session, with CPI and PPI featured. Later in the day, Canada will publish CPI and housing starts. US will release retail sales, import price, industrial production, business inventories and NAHB housing index.

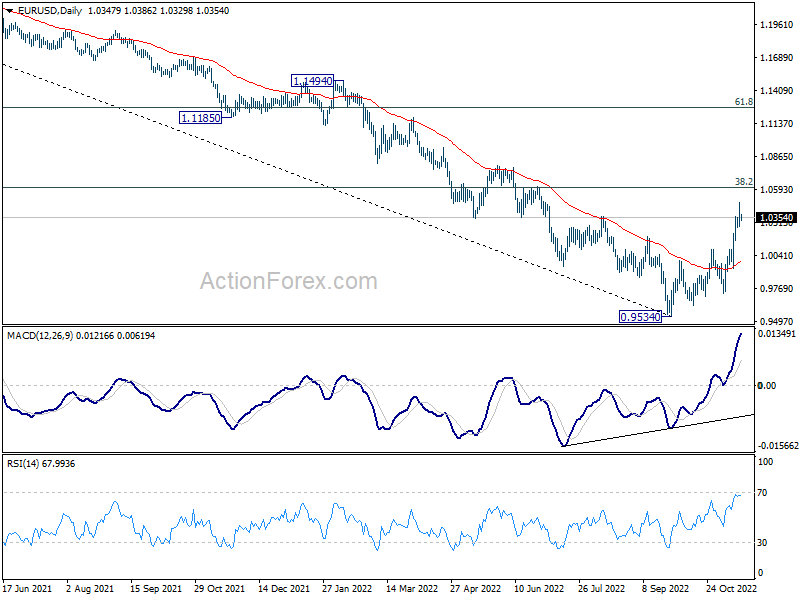

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0258; (P) 1.0369; (R1) 1.0458; More…

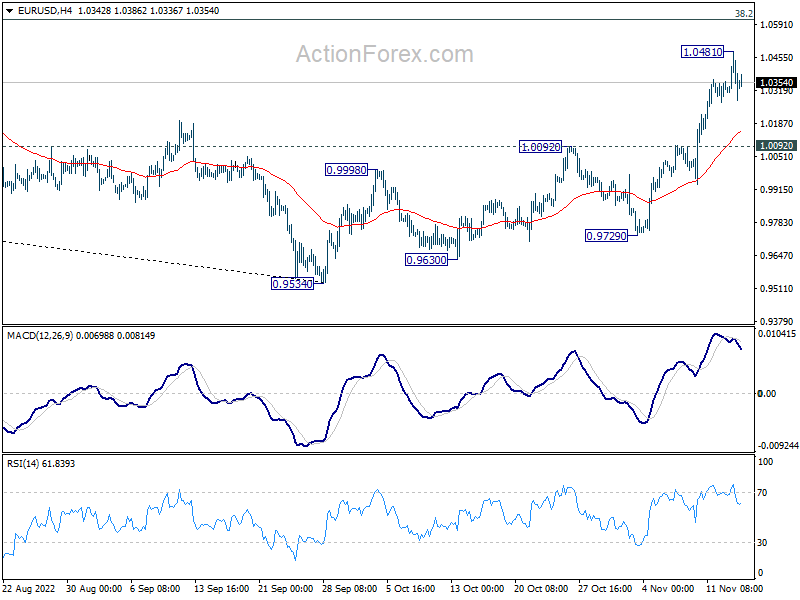

A temporary top is formed at 1.0481 with current retreat. Intraday bias in EUR/USD is turned neutral for some consolidations. Downside should be contained by 1.0092 resistance turned support to bring another rally. Break of 1.0481 will resume the rise from 0.9534 and target 1.0609 fibonacci level.

{kind=link}

In the bigger picture, a medium term bottom was in place at 0.9534, on bullish convergence condition in daily MACD. Even as a corrective rise, rally from 0.9534 should target 38.2% retracement of 1.2348 (2021 high) to 0.9534 at 1.0609. Sustained trading above 55 week EMA (now at 1.0566) will raise the chance of trend reversal and target 61.8% retracement at 1.1273. This will now remain the favored case as long as 1.0092 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Oct | -0.10% | 0.00% | ||

| 23:50 | JPY | Machinery Orders M/M Sep | -4.60% | 0.70% | -5.80% | |

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 1.00% | 0.90% | 0.70% | 0.80% |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | -0.4% | 0.60% | 0.70% | |

| 07:00 | GBP | CPI M/M Oct | 1.70% | 0.50% | ||

| 07:00 | GBP | CPI Y/Y Oct | 10.60% | 10.10% | ||

| 07:00 | GBP | Core CPI Y/Y Oct | 6.40% | 6.50% | ||

| 07:00 | GBP | RPI M/M Oct | 1.80% | 0.70% | ||

| 07:00 | GBP | RPI Y/Y Oct | 13.40% | 12.60% | ||

| 07:00 | GBP | PPI Input M/M Oct | 1.00% | 0.40% | ||

| 07:00 | GBP | PPI Input Y/Y Oct | 17.70% | 20.00% | ||

| 07:00 | GBP | PPI Output M/M Oct | 0.00% | 0.20% | ||

| 07:00 | GBP | PPI Output Y/Y Oct | 14.80% | 15.90% | ||

| 07:00 | GBP | PPI Core Output M/M Oct | 1.30% | 0.70% | ||

| 07:00 | GBP | PPI Core Output Y/Y Oct | 14.00% | 14.00% | ||

| 13:15 | CAD | Housing Starts Oct | 275K | 300K | ||

| 13:30 | CAD | CPI M/M Oct | 0.80% | 0.10% | ||

| 13:30 | CAD | CPI Y/Y Oct | 7.00% | 6.90% | ||

| 13:30 | CAD | CPI Median Y/Y Oct | 4.80% | 4.70% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Oct | 5.30% | 5.20% | ||

| 13:30 | CAD | CPI Common Y/Y Oct | 5.90% | 6.00% | ||

| 13:30 | USD | Retail Sales M/M Oct | 0.90% | 0.00% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 0.40% | 0.10% | ||

| 13:30 | USD | Import Price Index M/M Oct | -0.50% | -1.20% | ||

| 14:15 | USD | Industrial Production M/M Oct | 0.20% | 0.40% | ||

| 14:15 | USD | Capacity Utilization Oct | 80.40% | 80.30% | ||

| 15:00 | USD | Business Inventories Sep | 0.50% | 0.80% | ||

| 15:00 | USD | NAHB Housing Market Index Nov | 36 | 38 | ||

| 15:30 | USD | Crude Oil Inventories | -2.0M | 3.9M |