Overall, the forex markets are bounded in tight range as consolidative trading continues. There is no clear sign of a sustainable rebound in Dollar, and thus, the most is more likely down than up. Yen is clearly soft but selling hasn’t really take off yet. Commodity currencies are currently having a slight upper hand against Europeans, but nobody is overwhelming nobody yet.

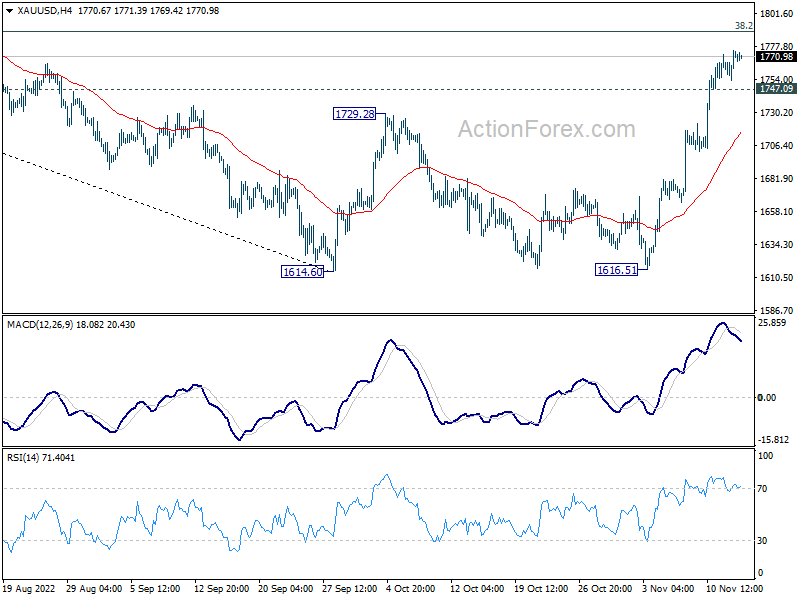

Technically, Gold’s rally continues today but upside momentum is diminishing as seen in 4 hour MACD. While further rise is likely, upside could be limited by 38.2% retracement of 2070.06 to 1614.60 at 1788.58, at least on first attempt. Break of 1747.09 minor support turn this bias to the downside for 4 hours 55 EMA (now at 1716.38). If happens, that might be accompanied by corresponding recovery in Dollar.

{kind=link}

In Asia, Nikkei rose 0.10%. Hong Kong HSI is up 3.36%. China Shanghai SSE is up 1.49%. Singapore Strait Times is up 0.63%. Japan 10-year JGB yield is up 0.0029 at 0.245. Overnight, DOW dropped -0.63%. S&P 500 dropped -0.89%. NASDAQ dropped -1.12%. 10-year yield rose 0.052 to 3.865.

Fed Brainard: Appropriate soon to move to a slower pace

Fed Vice Chair Lael Brainard said yesterday, “I think it will probably be appropriate soon to move to a slower pace of increases, but I think what’s really important to emphasize is… we have additional work to do.”

“It’s really going to be an exercise on watching the data carefully and trying to assess how much restraint there is and how much additional restraint is going to be necessary, and sustained for how long, and those are the kinds of judgments that lie ahead for us,” she said.

“It makes sense to move to a more deliberate and a more data dependent pace as we continue to make sure that there’s restraint that will bring inflation down over time,” she said.

“As we go forward…risks are going to be two sided if we get into more restrictive or further into restrictive territory,” she said, “so we’ll be balancing those considerations.”

SNB Jordan: High probability for another rate hike in Dec

SNB Chairman Thomas Jordan said yesterday, “it cannot be excluded that the SNB will raise interest rates in December,” given that interest rates are still low.

“There is a high probability that the SNB will have to tighten its monetary policy further,” he said. “The next meeting will be in December and there is a high probability that it will be necessary to tighten monetary policy again to make sure that inflation can be fought sufficiently.”

RBA minutes: Not ruling out returning to larger hikes

Minutes of RBA’s November 1 meeting revealed that board members consider both a 25 bps or a 50bps rate hike. There were “arguments in favour of both courses of action”, but the case for 25bps was stronger.

“Acknowledging the uncertainty, members did not rule out returning to larger increases if the situation warranted,” the minutes noted. “Conversely, the Board is prepared to keep rates unchanged for a period while it assesses the state of the economy and the inflation outlook. Interest rates are not on a pre-set path.”

At the meeting, RBA raised the cash rate target by 25bps to 2.85%.

Japan GDP contracted -0.3% qoq in Q3

Japan GDP contracted -0.3% qoq in Q3, much worse than expectation of 0.3% qoq. In annualized term, GDP contracted -1.2%, versus expectation of 1.1%. GDP deflator dropped -0.5% yoy, versus expectation of -0.2% yoy.

During the quarter, imports rose strongly by 5.2% yoy on higher energy costs and weak Yen exchange rate. Exports grew only 1.9% qoq and led to a decline in net exports, which dragged GDP down. Domestically, private consumption grew 0.3% qoq only.

“Increased imports due to the easing of supply constraints and a temporary increase in payments for external services contributed to the negative growth,” Chief Cabinet Secretary Hirokazu Matsuno said.

“The environment surrounding households and businesses is becoming more difficult, with declining real household incomes and rising corporate costs,” Matsuno added.

China retail sales contracted -0.5% yoy in Oct

China industrial production rose 5.0% yoy in October, below expectation of 5.2% yoy. Retail sales dropped -0.5% yoy, much worse than expectation of 1.0% yoy. That’s also the first decline since May. Fixed asset investment rose 5.8% ytd yoy, below expectation of 5.9%.

“We will focus on expanding effective demand, deepening structural reform on the supply side, continuing to stabilise employment and prices, stabilizing expectations, stimulating market vitality more, consolidating the economic recovery to a sound basis, and try to achieve better development results,” the NBS said in a statement.

Looking ahead

UK job data will be focus in European session. Germany ZEW economic sentiment is another. Eurozone will also release GDP revision and trade balance. Later in the day, Canada will release manufacturing sales and wholesale sales. US will release PPI and Empire State manufacturing index.

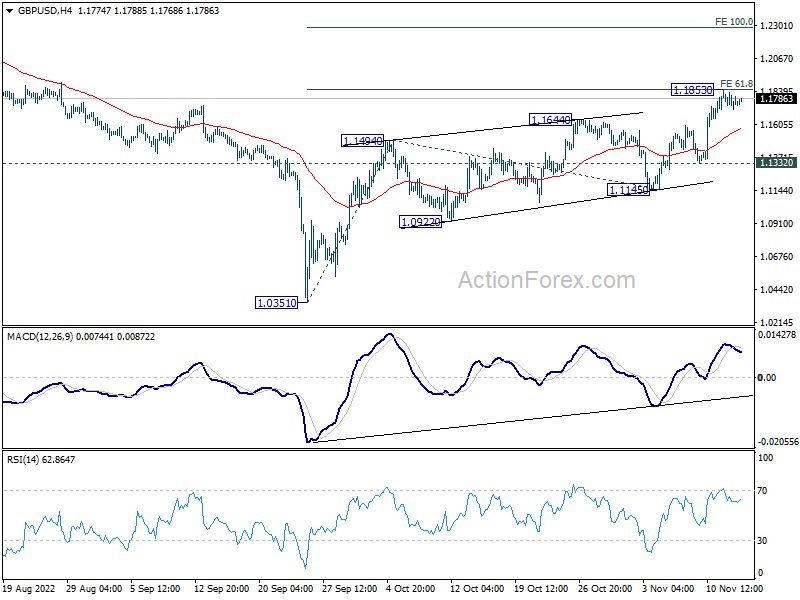

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1703; (P) 1.1766; (R1) 1.1821; More…

Intraday bias in GBP/USD is turned neutral first with a temporary top in place at 1.1853. Some consolidations would be seen first, but downside of retreat should be contained above 1.1332 support to bring another rise. On the upside, firm break of 61.8% projection of 1.0351 to 1.1494 from 1.1145 at 1.1851 will pave the way to 100% projection at 1.2288.

{kind=link}

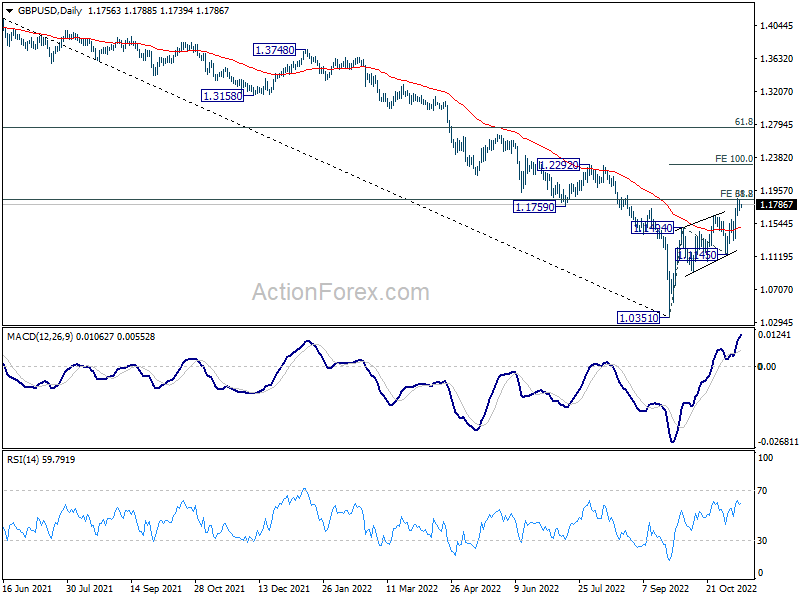

In the bigger picture, current development suggests that rise from 1.0351 is a medium term bottom. Rise from there is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1145 support holds. Sustained break of 38.2% retracement of 1.4248 to 1.0351 at 1.1840 will pave the way to 61.8% retracement at 1.2759 and possibly above.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q3 P | -0.30% | 0.30% | 0.90% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | -0.50% | -0.60% | -0.30% | |

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 02:00 | CNY | Industrial Production Y/Y Oct | 5.00% | 5.20% | 6.30% | |

| 02:00 | CNY | Retail Sales Y/Y Oct | -0.50% | 1.00% | 2.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 5.80% | 5.90% | 5.90% | |

| 04:30 | JPY | Industrial Production M/M Sep F | -1.70% | -1.60% | -1.60% | |

| 07:00 | GBP | Claimant Count Change Oct | -12.6K | 25.5K | ||

| 07:00 | GBP | Unemployment Rate (3M) Sep | 3.50% | 3.50% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 5.60% | 5.40% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 6.00% | 6.00% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | -39.4B | -47.3B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.20% | 0.20% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.30% | 0.40% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | -54.1 | -59.2 | ||

| 10:00 | EUR | Germany ZEW Current Situation Nov | -67.5 | -72.2 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | -55 | -59.7 | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | -0.50% | -2.00% | ||

| 13:30 | CAD | Wholesale Sales M/M Sep | -0.20% | 1.40% | ||

| 13:30 | USD | Empire State Manufacturing Index Nov | -7 | -9.1 | ||

| 13:30 | USD | PPI M/M Oct | 0.50% | 0.40% | ||

| 13:30 | USD | PPI Y/Y Oct | 8.30% | 8.50% | ||

| 13:30 | USD | PPI Core M/M Oct | 0.40% | 0.30% | ||

| 13:30 | USD | PPI Core Y/Y Oct | 7.20% | 7.20% |