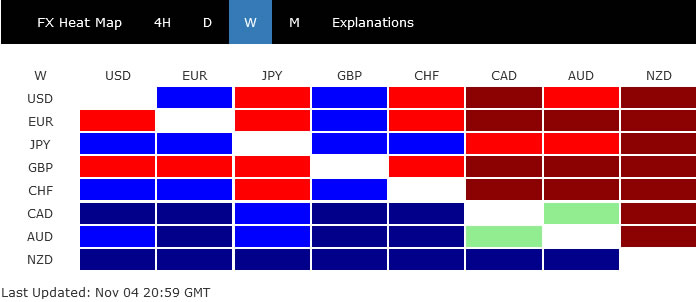

The rumor of earlier reopening in China seemed to have overwhelmed other heavy weight events in the markets last week, including Fed’s hawkish rate hike and non-farm payroll report. Late rally in stock markets helped commodity currencies secured the winning places, with New Zealand Dollar having an edge over Australian and Canadian.

On the other hand, Sterling ended as the worst performer, paring some of the Sunak-era gains, and weighed down by BoE dovish hike. Euro and Swiss Franc didn’t perform much better, even though they did rebounded against the greenback. Dollar was mixed together with Yen, awaiting more guidance from risk sentiment ahead.

{kind=link}

DOW and NASDAQ display contrasting picture

Market sentiment sank after Fed chair Jerome Powell indicated that the terminal interest rate of current cycle could be higher than originally thought, even though the pace of tightening could start to slow as soon as at next meeting. However, the set of non-farm payroll data left investors divided. The strong headline job growth number affirmed Fed’s stance to continue with rate hikes. But the rise in unemployment rate was taken by some as a sign of cooling.

DOW pared back much of the earlier losses on Friday, even though it still lost the weekly winning streak. For now, DOW remains very resilient and rise from 28600.94 should still be in progress towards 34281.36 resistance. Decisive break there will confirm completion of the whole medium term correction from 36952.65 and pave the way to retest this high, probably in the early part of next year. This week remain the favored case as long as 55 day EMA (now at 31241.58) holds.

{kind=link}

However, NASDAQ is displaying a completely different picture. The recovery on Friday was relatively weak. Prior rejection by 55 day EMA affirmed near term bearishness. It’s still expected to extend the down trend from 16212.22 to 61.8% projection from 16212.22 to 10565.13 from 13181.08 at 9691.17, at least, before forming a bottom.

{kind=link}

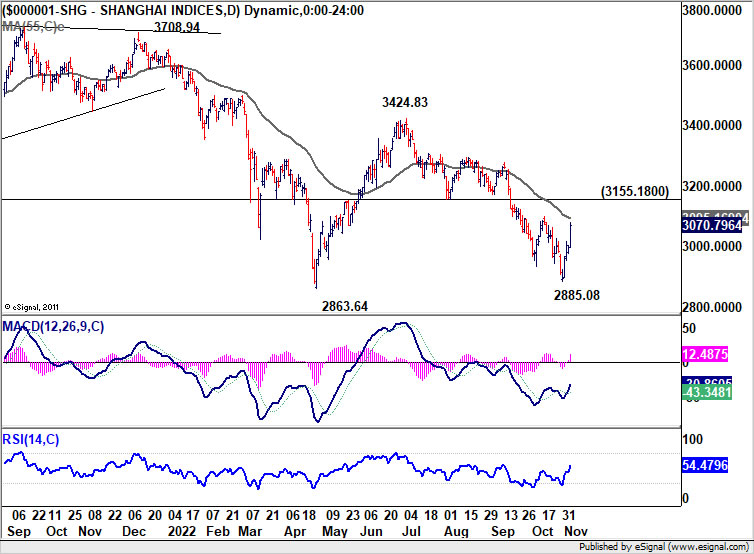

Turnaround in China markets on reopening hope

The turnaround in China markets could be an even stronger factor supporting sentiment elsewhere, including the US and the rebound in DOW. The 5% gain in the Shanghai SSE is seen as triggered by hope for reopening to happen earlier than expected. No official announcement was made by the Chinese government on changing its zero-COVID policy yet. But rumors are alreadying circulating around.

Technically, Shanghai SSE’s rebound from 2885.08 will face the first hurdle at 55 day EMA (now at 3095.16). Sustained trading above the EMA, and better followed by firm break of 3155.18 support turned resistance, should confirmed that whole decline from 3424.83 was over. That would set the stage for further rally to towards 3424.83 resistance. Before that happens, the case of earlier reopening would remain doubtful.

{kind=link}

Dollar extending correction, breakout delayed

Improving market sentiment, both in the US and China, knocked Dollar index down towards the end of the week. Yet, there is no change in the technical outlook that DXY is in consolidation from 114.77. It’s staying well inside the medium term rising channel, and thus, a breakout through 114.77 high is just delayed, not derailed. Nevertheless, sustained break of the channel support (now at around 109) will argue that it’s already in a medium term correction and would target 104.63 support instead.

{kind=link}

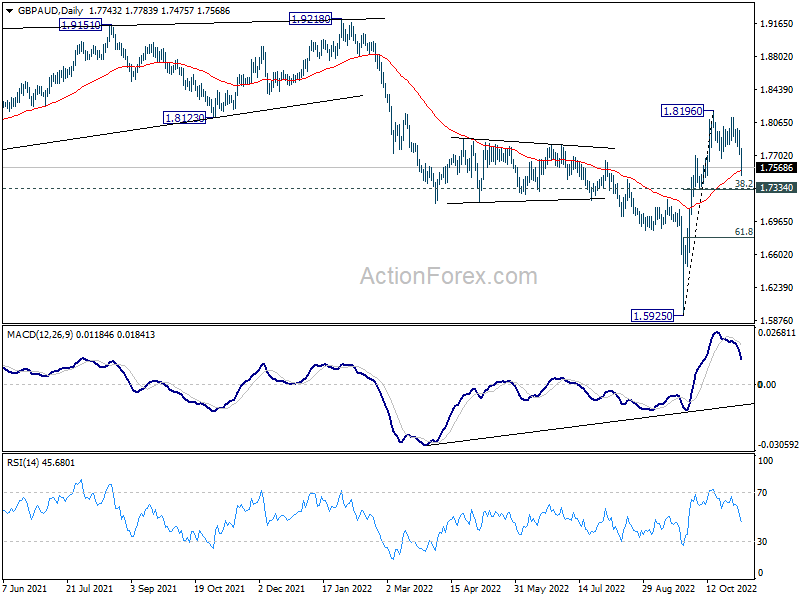

GBP/AUD in correction after dovish BoE hike

Sterling ended as the worst perform last week, partly because it just pared back some recent rebound. BoE’s dovish 75bps hike was another factor. The decision on rate was no unanimous, with 7 members voting for a 75bps hike, one member voting for 50bps and one member voting for 25bps. Inflation forecast was revised down due to the Government’s Energy Price Guarantee. At the same time, BoE is projecting recession for a prolonged period. The 75bps hike was seen as a one-off and next would be 50bps in December, followed by a final 25bps hike in February, before pausing.

GBP/AUD’s decline from 1.8196 accelerated lower last week. still, it’s seen as a corrective move to the rebound from 1.5925 only. Strong support should be seen at 1.7334 cluster support (38.2% retracement of 1.5925 to 1.8196 at 1.7328) to contain downside. Rise from 1.5925 is expected to resume at a later stage.

Nevertheless, the development in GBP/AUD will heavily depend on sentiment on Aussie, and thus on whether China is really exiting its zero-COVID policy soon. If so, even still as a correction, GBP/AUD could fall further to 61.8% retracement at 1.6793 before bottoming.

{kind=link}

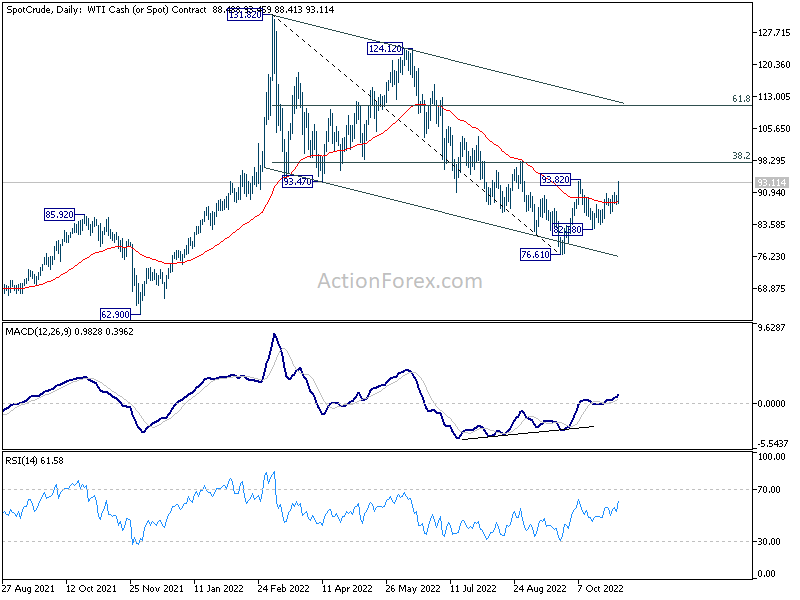

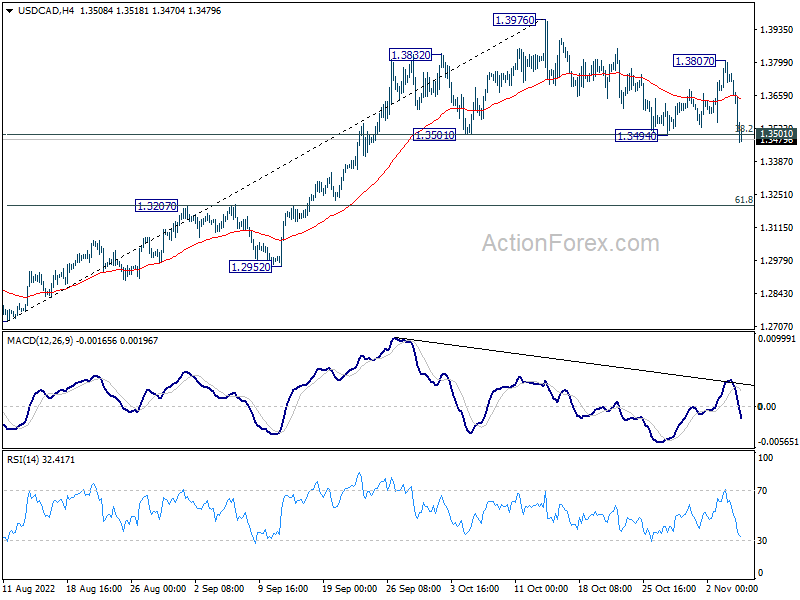

USD/CAD completed head and shoulder top

Canadian Dollar was among the best performers, as supported by stellar job market data and rise in oil price. WTI oil’s rise from 76.61 looks set to resume through 93.82 resistance soon. The key hurdle is in 38.2% retracement of 131.82 to 76.61 at 97.70. Sustained break there will argue that whole down trend from 131.82 has completed with three waves down to 76.61, and bring further rally to 61.8% retracement at 110.72. However, rejection by 97.70 will keep medium term bearish for another fall through 76.61.

{kind=link}

USD/CAD’s close below 1.3494 support suggests that it has completed a head and shoulder top pattern (ls: 1.3832; h: 1.3976; rs: 1.3807). Sustained trading below 1.3494 will confirm and bring deeper decline to 1.3207 cluster support (61.8% retracement of 1.2726 to 1.3976 at 1.3204), which is also close to 1.3222 resistance turned support. Downside should be contained there to bring rebound. But for near term, deeper fall is in favor as long as 1.3807 resistance holds.

{kind=link}

{kind=link}

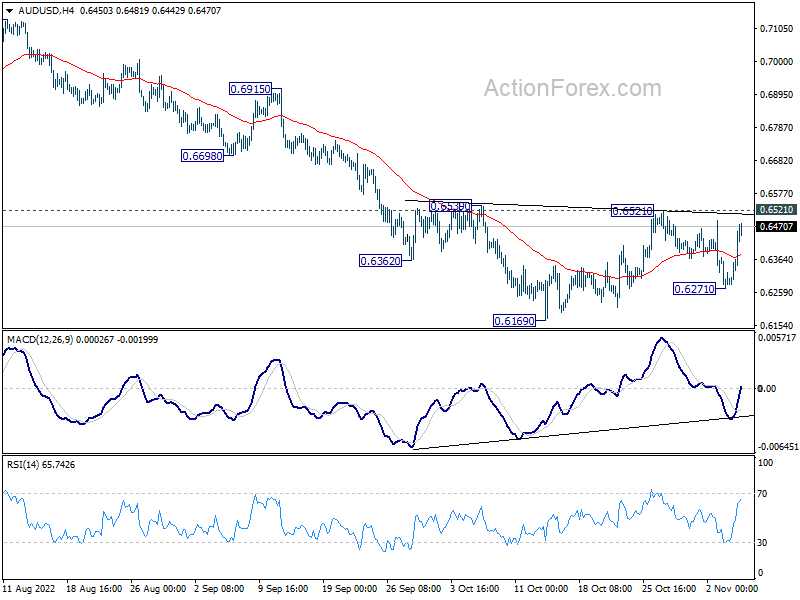

AUD/USD Weekly Outlook

AUD/USD was initially rejected by 0.6539 resistance and dipped to 0.6271 last week, but recovered notably since then. Initial bias is turned neutral this week first. On the upside, decisive break of 0.6521 resistance will now complete a head and shoulder bottom pattern (ls: 0.6362; h: 0.6169; rs: 0.6271). That would also come with sustained trading above 55 day EMA (now at 0.6533). Near term outlook will then be turned bullish for 0.6680/7315 resistance zone next. On the downside, however, break of 0.6271 will bring retest of 0.6169 low instead.

{kind=link}

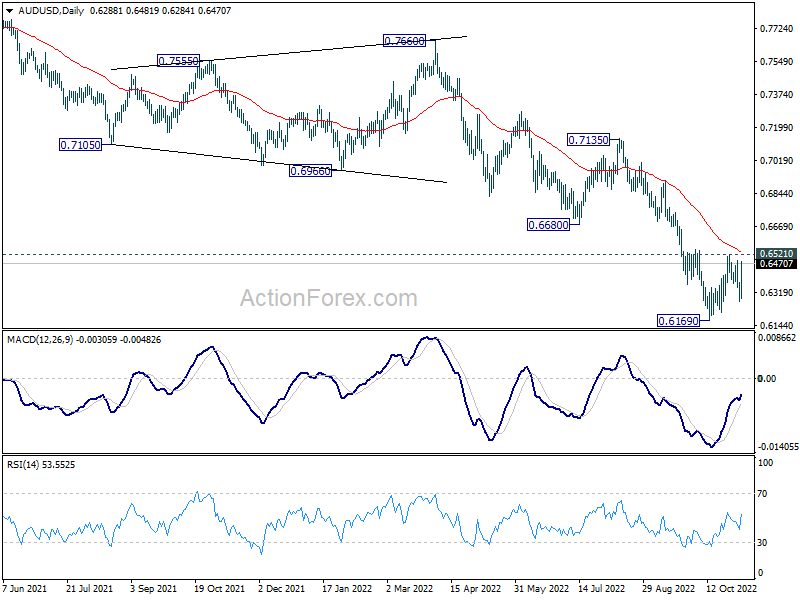

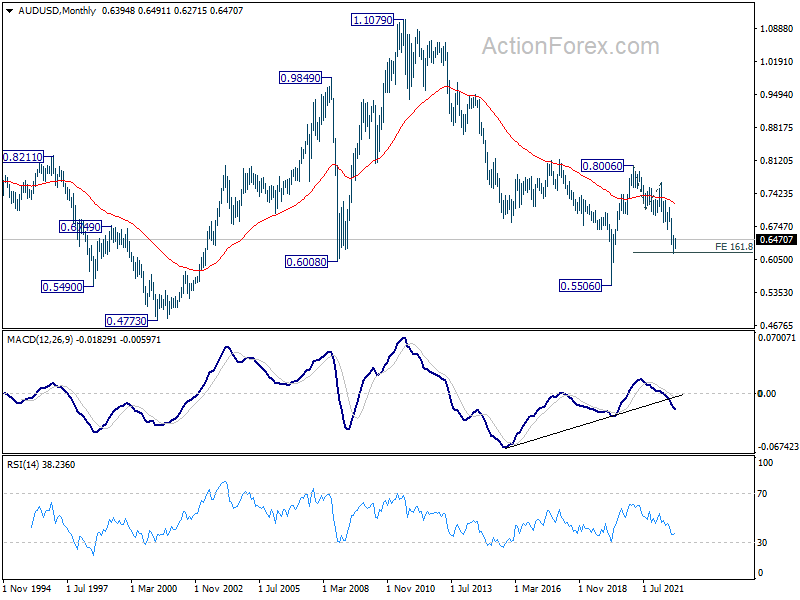

In the bigger picture, down trend from 0.8006 (2021 high) is expected to continue as long as 0.6680 support turned resistance holds. Medium term momentum remains strong and retest of 0.5506 (2020 low) cannot be ruled out. But firm break of 0.6680 will be the first sign of reversal, and bring stronger rebound back to 0.7135 resistance.

{kind=link}

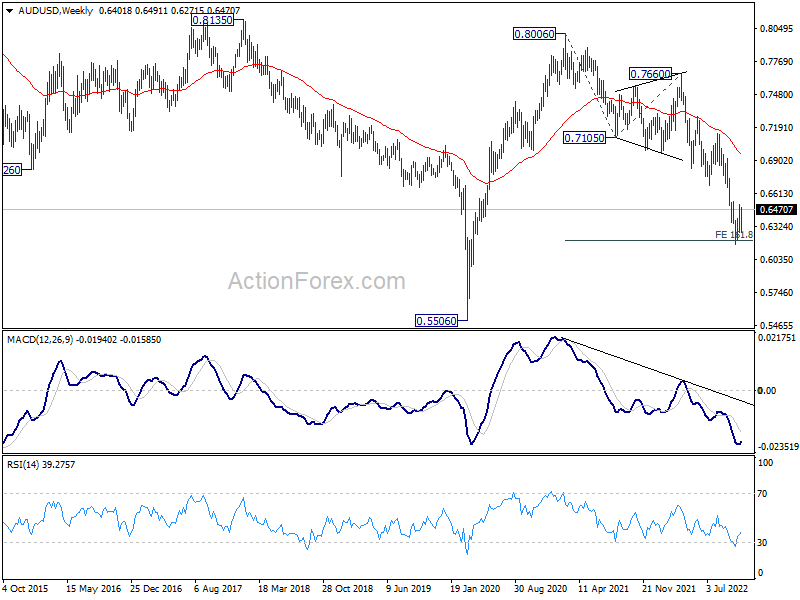

In the long term picture, the down trend from 0.8006 could still be seen as a corrective move, considering that it failed to break through 161.8% projection of 0.8006 to 0.7105 from 0.7660 at 0.6202 decisively. Strong rebound from current level will keep long term outlook neutral first. However, sustained break of 0.6202 will open up deep fall to retest 0.5506.

{kind=link}

{kind=link}