Australian Dollar trades higher today, following recovery in Asian stock markets. RBA hikes by 25 bps as widely expected and indicates more tightening to come ahead. There is little reaction as the message is well digested by the markets already. Nevertheless, Aussie is slightly outperformed by New Zealand Dollar for the moment. On the other hand, Dollar, Yen and Swiss France turned softer while European majors are mixed with Canadian.

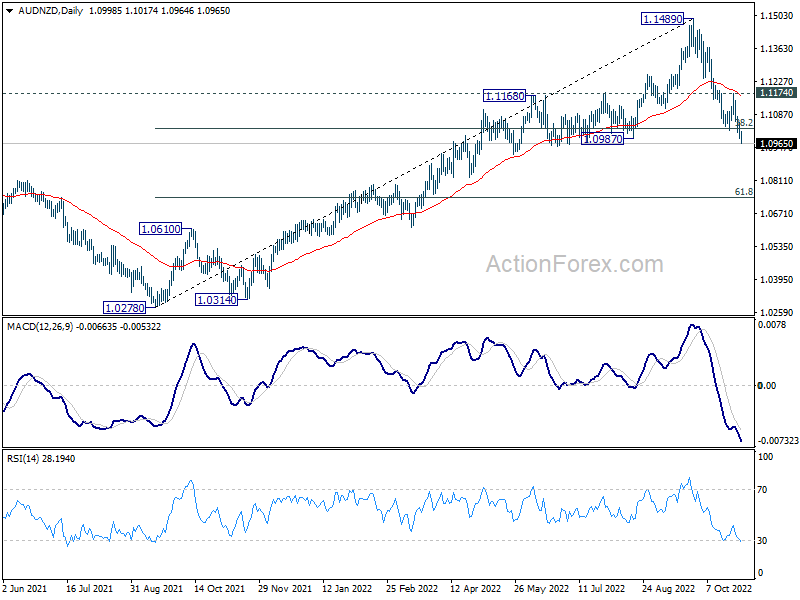

Technically, while Aussie is firmed elsewhere, it’s extending recent decline against Kiwi. AUD/NZD’s break of 1.0987 support suggests that deeper correction is underway. Near term outlook will stay bearish as long as 1.1174 resistance holds. Next target is 61.8% retracement of 1.0287 to 1.1489 at 1.0746. Such development would momentum of Aussie’s rebound elsewhere.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.11%. Hong Kong HSI is up 2.80%. China Shanghai SSE is up 1.03%. Singapore Strait Times is up 0.89%. Japan 10-year JGB yield is up 0.0101 at 0.255. Overnight, DOW dropped -0.39%. S&P 500 dropped -0.75%. NASDAQ dropped -1.03%. 10-year yield rose 0.0067 to 4.077.

RBA hikes 25bps, rates to rise further over the period ahead

RBA raises cash rate target by 25bps to 2.85% as widely expected. It maintains tightening bias and expects to “increase interest rates further over the period ahead”. The size and timing of future rate hikes will be determined by incoming data and the outlook for inflation and labor market.

The central bank expects inflation to “further increase” over the months ahead and peak at around 8% this year. CPI inflation is forecast to be around 4.75% over 2023 and a little above 3% over 2024. GDP growth forecast was “revised down a little” to 3% this year, 1.50% in 2023 and 2024. Unemployment rate is forecast to rise gradually from current 3.5% to a little above 4% in 2024 as economic growth slow.

China Caixin PMI manufacturing recovered to 49.2, impact of Covid controls lingered

China Caixin PMI Manufacturing rose from 48.1 to 49.2 in October, above expectation of 49.0. Caixin noted that output and new orders fell again as COVID-19 containment measures continued. Selling prices fell for the sixth consecutive month. Business confidence edged up slightly.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the negative impact of Covid controls on the economy lingered. In October, supply, domestic and overseas demand, and employment in the manufacturing sector all contracted, but the rates of contraction slowed from the previous month. Costs rose slightly, and cuts to output prices were still common. Logistics and transportation were still sluggish, and companies’ purchases and inventories rose slightly. Market sentiment improved, but optimism remained limited from a long-term perspective.

Japan PMI manufacturing finalized at 50.7, but business remained optimistic

Japan PMI Manufacturing was finalized at 50.7 in October, slightly down from September’s 50.8. That’s the lowest level in 21 months. S&P Global noted that inflationary pressure remained severer. Business remained optimistic with sentiment at nine-month high.

Laura Denman, Economist at S&P Global Market Intelligence, said: “Sluggish markets and weaker demand conditions, on both a domestic and international level, became a recurring trend throughout the report and were seemingly the driving forces behind the slower sector performance… Meanwhile, inflationary pressures remained severe..

“Japanese manufacturing firms increased their selling prices more aggressively, as signalled by a near-record rate of output cost inflation…. Despite this, firms seem unfazed by the challenges that the sector is currently facing remaining optimistic towards their 12-month outlook on growth in October. In fact, the degree of confidence accelerated from September and reached a nine-month high.”

Looking ahead

Germany import prices, Swiss SECO consumer climate and SVME PMI, UK PMI manufacturing final will be featured in European session. Later in the day, US ISM manufacturing will take center stage while Canada will release PMI manufacturing.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6368; (P) 0.6398; (R1) 0.6428; More…

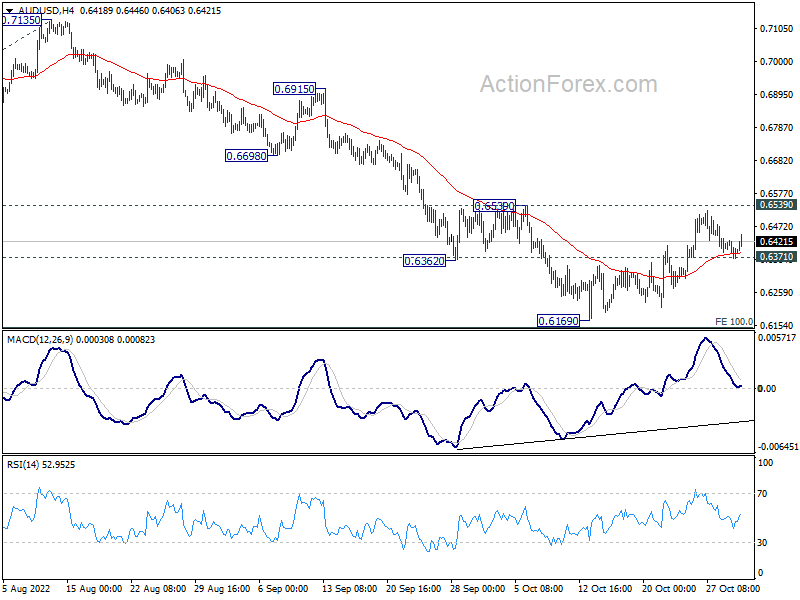

AUD/USD recovered after drawing support from 0.6371, but stays below 0.6539 resistance. Intraday bias stays neutral first. On the upside, decisive break of 0.6535 resistance, and sustained trading above 55 day EMA (now at 0.6553), will raise the chance of medium term bottoming, and target 0.6680 support turned resistance next. On the downside, below 0.6371 minor support will turn bias back to the downside for retesting 0.6169 low instead.

{kind=link}

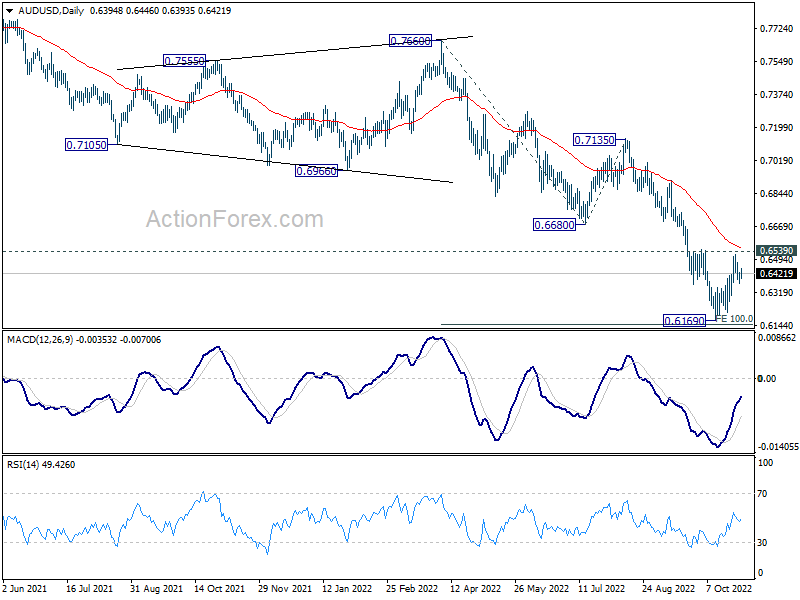

In the bigger picture, down trend form 0.8006 (2021 high) is expected to continue as long as 0.6680 support turned resistance holds. Medium term momentum remains strong and retest of 0.5506 (2020 low) cannot be ruled out. But firm break of 0.6680 will be the first sign of reversal, and bring stronger rebound back to 0.7135 resistance.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Sep | 3.80% | -1.60% | ||

| 00:30 | JPY | Manufacturing PMI Oct F | 50.7 | 50.7 | 50.7 | |

| 01:45 | CNY | Caixin Manufacturing PMI Oct | 49.2 | 49 | 48.1 | |

| 03:30 | AUD | RBA Interest Rate Decision | 2.85% | 2.85% | 2.60% | |

| 07:00 | EUR | Germany Import Price Index M/M Sep | 0.60% | 4.30% | ||

| 08:00 | CHF | SECO Consumer Climate Q4 | -43 | -42 | ||

| 08:30 | CHF | SVME PMI Oct | 56 | 57.1 | ||

| 09:30 | GBP | Manufacturing PMI Oct F | 45.8 | 45.8 | ||

| 13:30 | CAD | Manufacturing PMI Oct | 49.2 | 49.8 | ||

| 13:45 | USD | Manufacturing PMI Oct F | 49.9 | 49.9 | ||

| 14:00 | USD | ISM Manufacturing PMI Oct | 50 | 50.9 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | 53 | 51.7 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Oct | 48.7 | |||

| 14:00 | USD | Construction Spending M/M Sep | -0.50% | -0.70% |