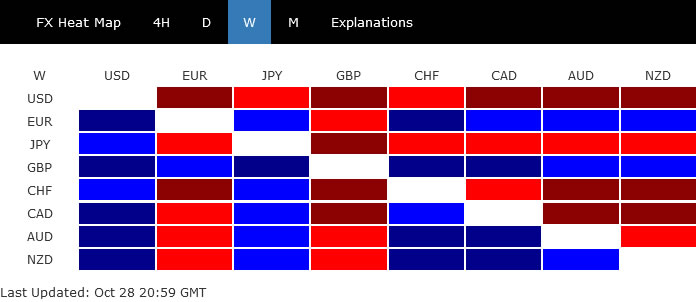

Dollar ended as the worst performer, followed by Yen and Swiss Franc. The US stock markets traded with risk-on sentiment, on talks that Fed would start slowing down tightening pace after one more 75bps hike. But it should be noted that such sentiment was not seen everywhere in the world, in particular China. Thus, rally in commodity currencies was somewhat capped.

Sterling and Euro were the best performers. The Pound was supported by stabilization in UK politics, and expectations of a 75bps hike by BoE. There is prospect of further rally in Sterling ahead, especially in crosses, if the new again UK government could restore investor confidence with the budget to be announced in the middle of the month.

{kind=link}

DOW surged on earnings and Fed pivot talks

DOW registered the fourth straight week of gains and closed strongly last week. Sentiment was partly supported by strong earnings of some stocks. Additionally, investors were raising bets that Fed will start slowing down tightening pace later in the year.

For now, fed fund futures are still pricing in 82.2% chance of a 75bps hike to 3.75-4.00% on November 2, the coming Wednesday. But change of another 75bps hike to 4.50-4.75% dropped below 50%. The move came as some central banks, like RBA and BoC, have already “pivot” to a smaller hikes.

DOW’s strong rise now raises the chance that corrective down trend from 36952.65 has completed at 28600.94 already. Firm break of trend line resistance (now at 33380) will affirm this bullish case and target 34281.36 resistance for confirmation. Even in case of retreat, near term bias will stay on the upside as long as 55 day EMA (now at 31014.89) holds.

Nevertheless, it should be noted that NASDAQ is lagging far far behind in the rebound. Thus, overall sentiment was not overwhelmingly positive.

{kind=link}

{kind=link}

But it’s risk-off in China and Hong Kong

Also, risk-on sentiment was not shared evenly globally. In particular, stocks in China and Hong Kong suffered steep selling as aftermath of the 20th Communist Party Congress. The Shanghai SSE hit the lowest level since May. Hong Kong HSI even fell to lowest level since 2009.

Current downside momentum in HSI suggests that it could well dive further to 161.8% projection of 33484.07 to 21139.26 from 31183.35 at 11209.44 before finding a bottom.

Risk-off sentiment in China is a factor capping rallies in Aussie and Kiwi, and could continue to do so.

{kind=link}

{kind=link}

It could be a pivot week for Dollar

As for Dollar index, corrective pattern from 114.77 continued with another dip last week and touched 55 day EMA. (now at 110.45). It’s now close to an important support zone, with 109.29 resistance turned support and medium term channel support. There is prospect of DXY completing the three wave pattern from 114.7. Strong bounce from current level will push DXY through 114.77 to resume larger up trend. However, sustained break of this support zone will indicate medium term topping, and bring deeper correction pack towards 104.63 support.

The next move will very much depends on FOMC decision and statement, as well as the set of economic data including ISM indexes and non-farm payroll. It could be a pivot week for Dollar, even if it’s too early for Fed.

{kind=link}

Sterling rose broadly as policy situation stabilized

Sterling was the best performer last week as the political situation appeared to have stabilized for now. Rishi Sunak was confirmed as the new UK Prime Minister, and he kept Jeremy Hunt in the position of Finance Minister. The new budget is delayed from October 31 to November 17, and there are expectations of some spending cuts and tax hikes to restore fiscal health of the country.

As for BoE, markets are now expecting 75bps hike on the coming Thursday. New economic projections might not be too meaningful given that the government’s budget won’t be ready.

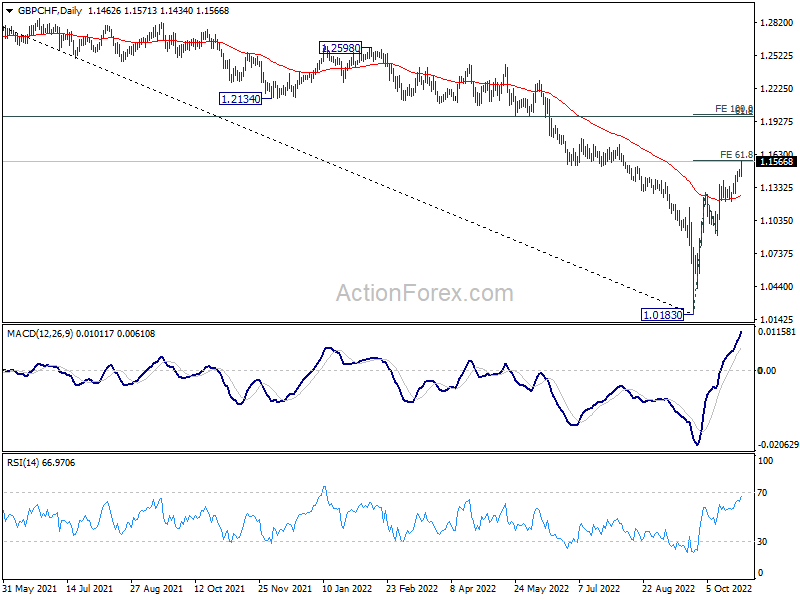

GBP/CHF extended the rebound from 1.0183 and is just inch below 61.8% projection of 1.0183 to 1.0893 to 1.1283 at 1.1573. Firm break of 1.1573 will target cluster level at 100% projection at 1.1993 and 61.8% retracement of 1.3070 to 1.0183 at 1.1967. In any case, further rally is in favor as long as 55 day EMA (now at 1.1251) holds.

{kind=link}

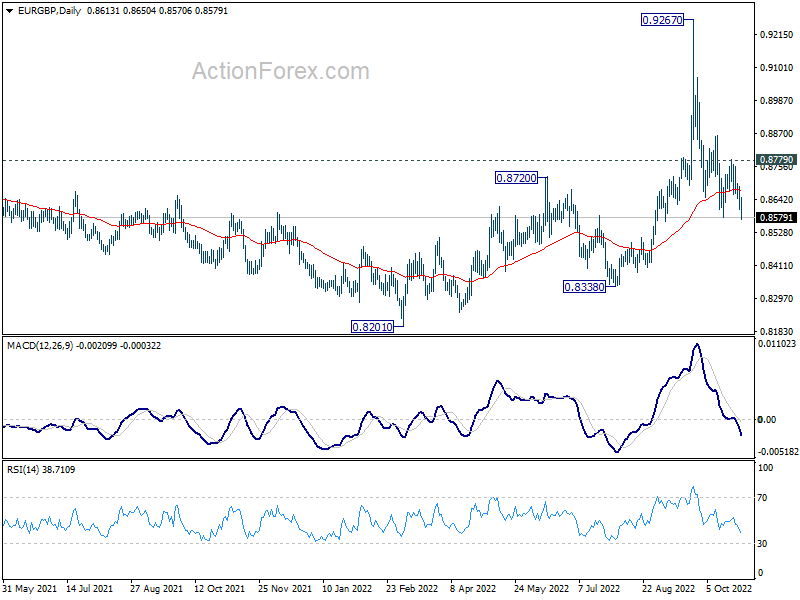

EUR/GBP is resuming the decline from 0.9267 with late breach of 0.8577 support. Outlook will stay bearish as long as 0.8779 resistance holds. Next target is 0.8201/8338 support zone.

{kind=link}

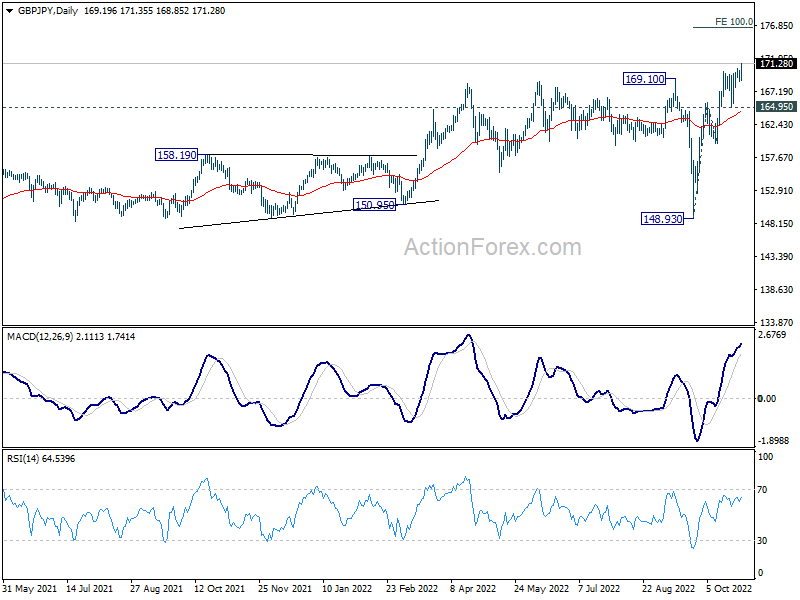

GBP/JPY’s up trend also resumed with late break of 170.57 resistance. Outlook will now stay bullish as long as 164.99 support holds. Next target is 100% projection of 148.93 to 165.69 from 159.71 at 176.47.

{kind=link}

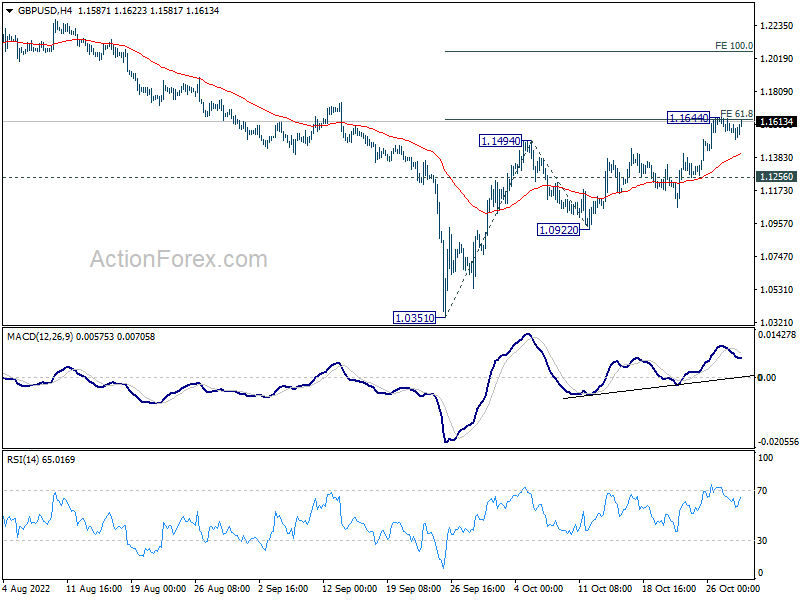

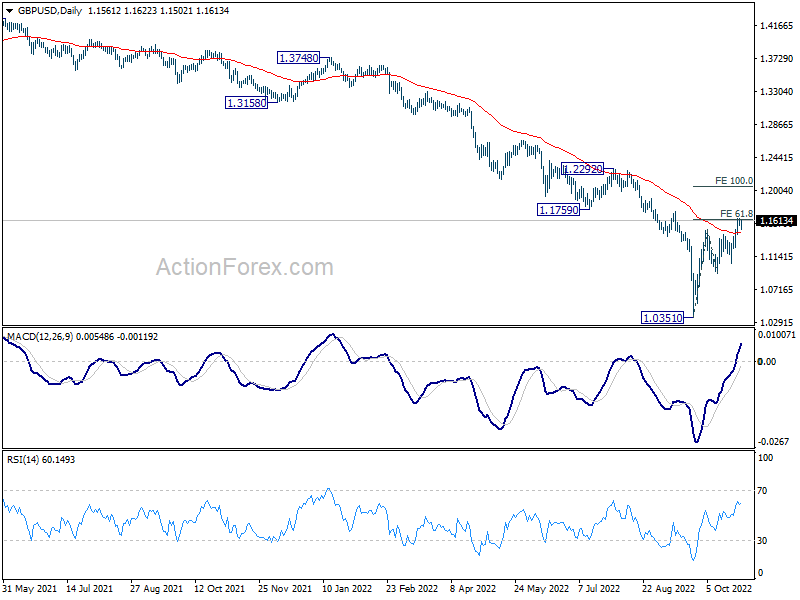

GBP/USD Weekly Outlook

GBP/USD’s rebound from 1.0351 resumed last week and hit 1.1644 before retreating. Initial bias stays neutral this week first, but further rise is expected as long as 1.1256 minor support holds. Break of 1.1644 will resume rise form 1.0351 to 100% projection of 1.0351 to 1.1494 from 1.0922 at 1.2065. However, break of 1.1256 will turn bias back to the downside for 1.0922 support and below.

{kind=link}

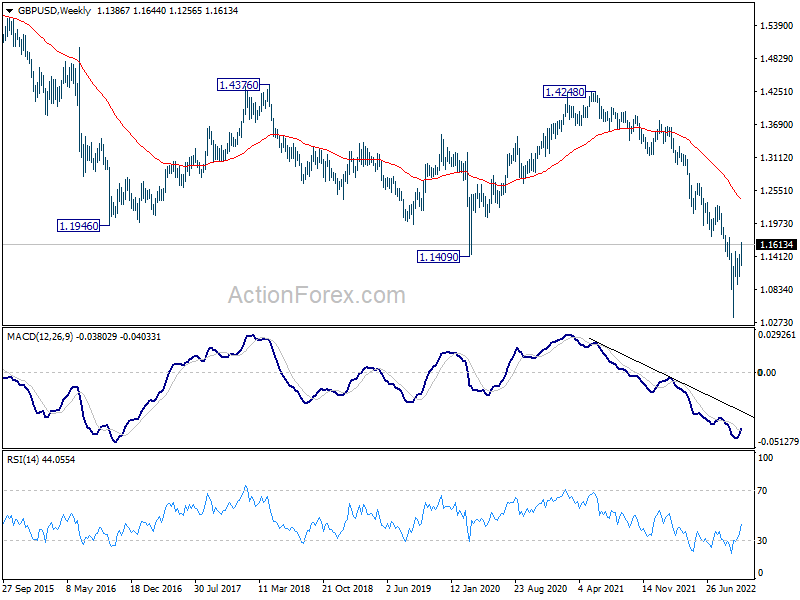

In the bigger picture, fall from 1.4248 (2018 high) is part of the long term down trend from 2.1161 (2007 high). Outlook will stay bearish as long as 1.1759 support turned resistance holds. Parity would be the next target on resumption. Nevertheless, firm break of 1.1759 will confirm medium term bottoming, and open up stronger rise back to 55 week EMA (now at 1.2392).

{kind=link}

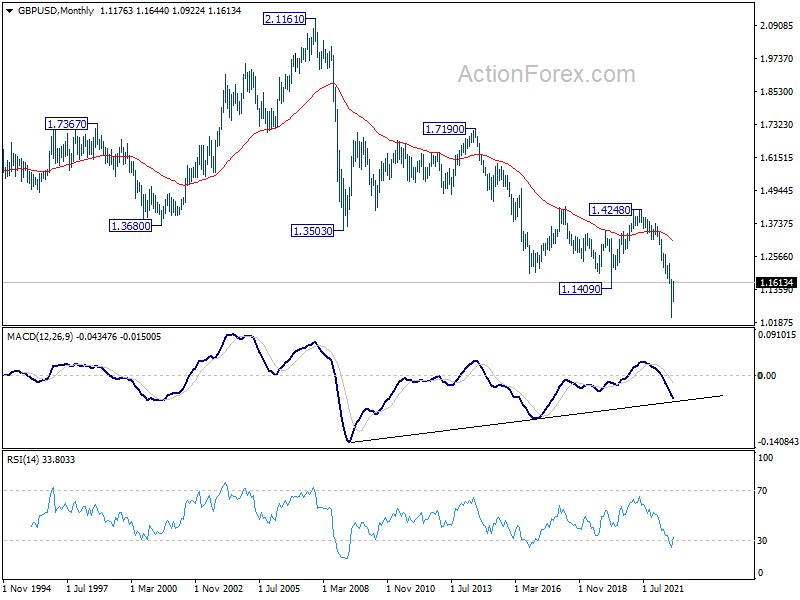

In the longer term picture, as long as 1.4248 resistance holds (2021 high), there is no confirmation of long term bottoming yet. That is, down trend from 2.1161 (2007) could still resume for another low through 1.0351.

{kind=link}

{kind=link}