Euro softens broadly today after ECB delivered 75bps rate hike as widely expected. President Christine Lagarde delivered no specially hawkish message that could give Euro another lift. On the down hand, Dollar is recovering, with some help from better than expected GDP data. But the greenback remains the worst performed followed by Canadian and Swiss Franc. Sterling is the leader.

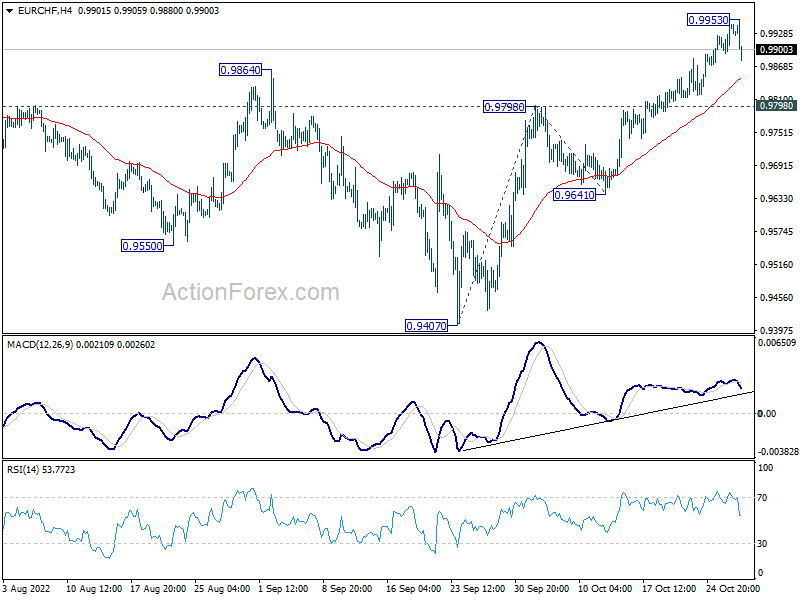

Technically, EUR/CHF’s retreat now suggests that a temporary top is in place at 0.9953, just ahead of parity. Some consolidations could be seen. But another rise will remain in favor as long as 0.9798 resistance turned support holds. Rise from 0.9407 should still resume at a later stage.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.17%. DAX is up 0.05%. CAC is down -0.30%. Germany 10-year yield is down -0.102 at 2.014. Earlier in Asia, Nikkei dropped -0.32%. Hong Kong HSI rose 0.72%. China Shanghai SSE dropped -0.55%. Singapore Strait Times rose 0.23%. Japan 10-year JGB yield dropped -0.0055 to 0.253.

ECB hikes 75bps, recalibrates TLTRO III

ECB raises interest rates by 75bps as widely expected. The main refinancing, marginal lending, and deposit rates are 2.00%, 2.25%, and 1.50% respectively, with effect from November 2. The central bank also maintains tightening bias, and said, it “expects to raise interest rates further, to ensure the timely return of inflation to its 2% medium-term inflation target.”

Future policy rate path will be based on the “evolving outlook for inflation and the economy”, and follow its “meeting-by-meeting approach.

Also, the terms and conditions of the TLTRO III refinancing operations are changed, and “recalibrated” to ensure consistency with broader monetary policy normalization process.

US GDP grew 2.6% annualized in Q3, slightly above expectations

US GDP grew at annualized rate of 2.6% in Q3, above expectation of 2.4%. PCE price index growth slowed from 9.0% to 4.1%, below expectation of 5.4%.

BEA noted that the increase in real GDP reflected increases in exports, consumer spending, nonresidential fixed investment, federal government spending, and state and local government spending, that were partly offset by decreases in residential fixed investment and private inventory investment. Imports, which are a subtraction in the calculation of GDP, decreased.

Also released, durable goods orders rose 0.4% mom in september, below expectation of 0.5% mom. Ex-transport order dropped -0.5% mom, worse than expectation of 0.0% mom. Initial jobless claims rose 3k to 217k in the week ending October 21.

Germany Gfk consumer sentiment rose to -41.9, too early to speck of a trend shift

Germany Gfk Consumer Sentiment for November improved from -42.8 to -41.9, slightly below expectation of -41.8. In October, economic expectations dropped from -21.9 to -22.2. Income expectations rose from -67.7 to -60.5. Propensity to buy also rose from -19.5 to -17.5.

“It is certainly too early to speak of a trend shift at this time. The situation remains very tense for consumer sentiment,” explains Rolf Bürkl, GfK consumer expert. “Inflation has recently risen to ten percent in Germany, and concerns about the security of energy supplies continue to rise. Therefore, it remains to be seen whether the current stabilization will last or whether, considering the upcoming winter, there is reason to fear a further worsening of the situation.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9989; (P) 1.0039; (R1) 1.0134; More…

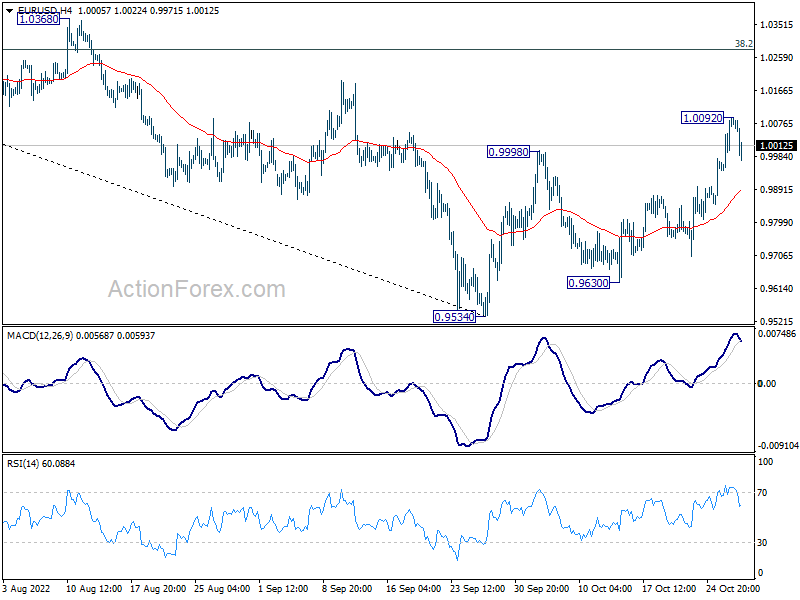

EUR/USD retreated after hitting 1.0092 and intraday bias is turned neutral first. Overall, rise from 0.9534 is still expected to continue as long as 4 hour 55 EMA (now at 0.9885). Above 1.0092 will resume the rally from 0.9534 to 38.2% retracement of 1.1494 to 0.9534 at 1.0283.

{kind=link}

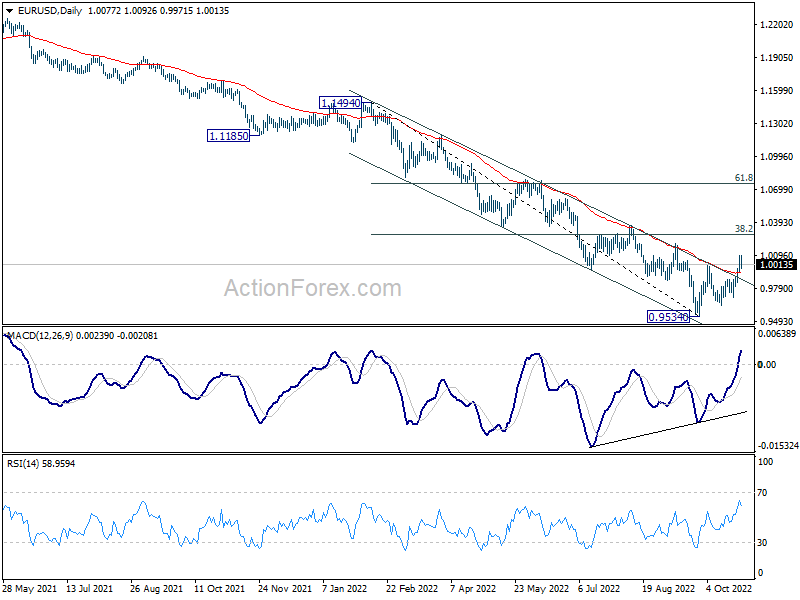

In the bigger picture, the case of medium term bottoming at 0.9534 building up, with bullish convergence condition in daily MACD. While it is too early to call for trend reversal, firm break of 0.9998 opens up stronger rebound back to 55 week EMA (now at 1.0630) even as a corrective rise. This will now be the favored case as long as 55 day EMA (now at 0.9937) holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Import Price Index Q/Q Q3 | 3.00% | 0.80% | 4.30% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Nov | -41.9 | -41.8 | -42.5 | -42.8 |

| 12:15 | EUR | ECB Main Refinancing Rate | 2.00% | 2.00% | 1.25% | |

| 12:30 | USD | Initial Jobless Claims (Oct 21) | 217K | 225K | 214K | |

| 12:30 | USD | GDP Annualized Q3 P | 2.60% | 2.40% | -0.60% | |

| 12:30 | USD | GDP Price Index Q3 P | 4.10% | 5.40% | 9.10% | 9.00% |

| 12:30 | USD | Durable Goods Orders Sep | 0.40% | 0.50% | -0.20% | 0.30% |

| 12:30 | USD | Durable Goods Orders ex Transportation Sep | -0.50% | 0.00% | 0.20% | |

| 12:45 | EUR | ECB Press Conference | ||||

| 14:30 | USD | Natural Gas Storage | 111B |