It’s an extremely slow day in the markets. Sterling appears to be a touch stronger after Rishi Sunak finally become the third UK Prime Minister in Two months, accepting King Charles’s request to form a government. Meanwhile, Swiss Franc is slightly on the softer side. But overall, most major crosses and pairs are staying range bound. Germany Ifo Business Climate triggered no reaction in Euro. The stock markets are mixed too, with China markets closed slightly slower despite attempt by the “national team” to buy a rebound. Benchmark treasury yields in the US and Europe are also trading lower.

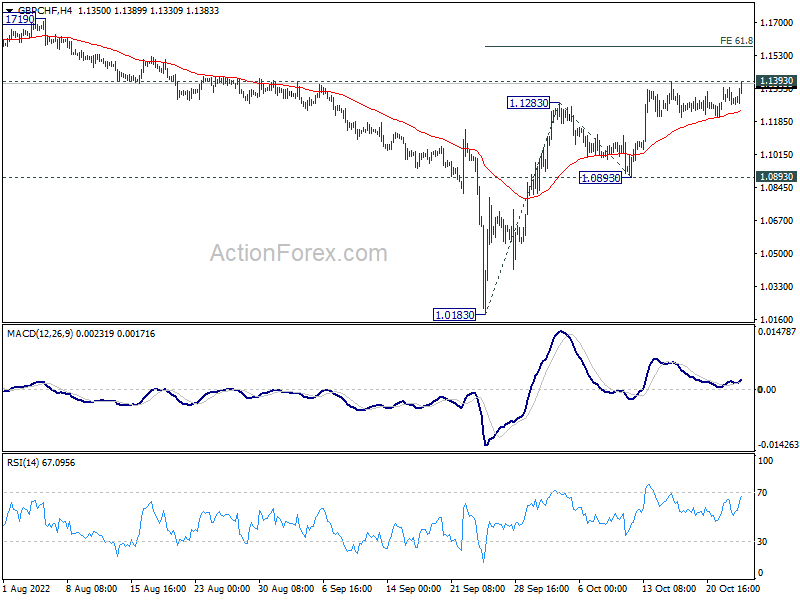

Technically, EUR/CHF’s rally today is so far not accompanied by any meaning movement in Euro elsewhere. Now, GBP/CHF appears to be trying to resume near term rise from 1.0183. Firm break of 1.1393 resistance will confirm and target 61.8% projection of 1.0183 to 1.1283 from 1.0893 at 1.1573. Let’s see whether the Pound would move elsewhere or not.

{kind=link}

In Europe, at the time of writing, FTSE is down-0.83%. DAX is down -0.96%. CAC is up 0.17%. Germany 10-year yield is down -0.0989 at 2.231. Earlier in Asia, Nikkei rose 1.02%. Hong Kong HSI dropped -0.10%. China Shanghai SSE dropped -0.04%. Singapore Strait Times rose 0.48%. Japan 10-year JGB yield rose 0.0004 to 0.257.

Germany Ifo business climate fell slightly to 84.3, facing a difficult winter

Germany Ifo Business Climate ticked down from 84.4 to 84.3 in October, above expectation of 84.0. Current Assessment index dropped from 94.5 to 94.1, above expectation of 92.5. Expectations index rose from 75.3 to 75.6, above expectation of 74.9.

By sector, manufacturing fell from -14.3 to -15.9. Services rose slightly from -8.9 to -8.6. Trade rose from -32.3 to -31.9. Construction dropped from -21.9 to -24.9.

Ifo isad: “Companies were less satisfied with their current business. Their expectations improved, but they are still worried about the coming months. The German economy is facing a difficult winter.”

RBNZ Conway hopeful that inflation has peaked

RBNZ Chief Economist Paul Conway said annual inflation rate of 7.2% was “obviously too high”. But, he added, “we expect to see inflationary pressures easing going forward” and “are hopeful that it has peaked.”

The “very rapid tightening in monetary policy” is starting to have an effect and “there are early signs that the economy is starting to cool,” he said.

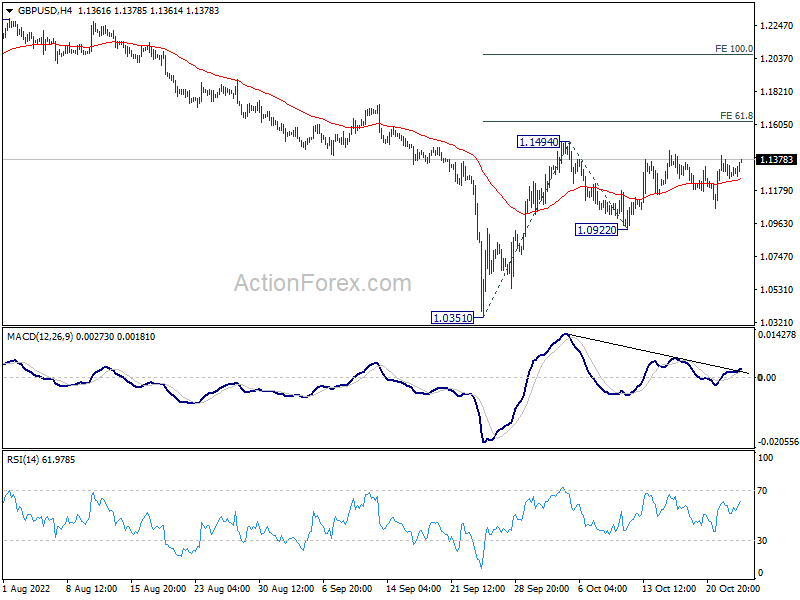

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1222; (P) 1.1316; (R1) 1.1373; More…

GBP/USD rises mildly today but stays inside range of 1.0922/1494. Intraday bias remains neutral for the moment. Further rally is in favor with 1.0922 minor support intact. On the upside, break of 1.1494 will resume the rise from 1.0351 to 61.8% projection of 1.0351 to 1.1494 from 1.0922 at 1.1628. On the downside, below 1.0922 will turn bias back to the downside for 1.0351 low instead.

{kind=link}

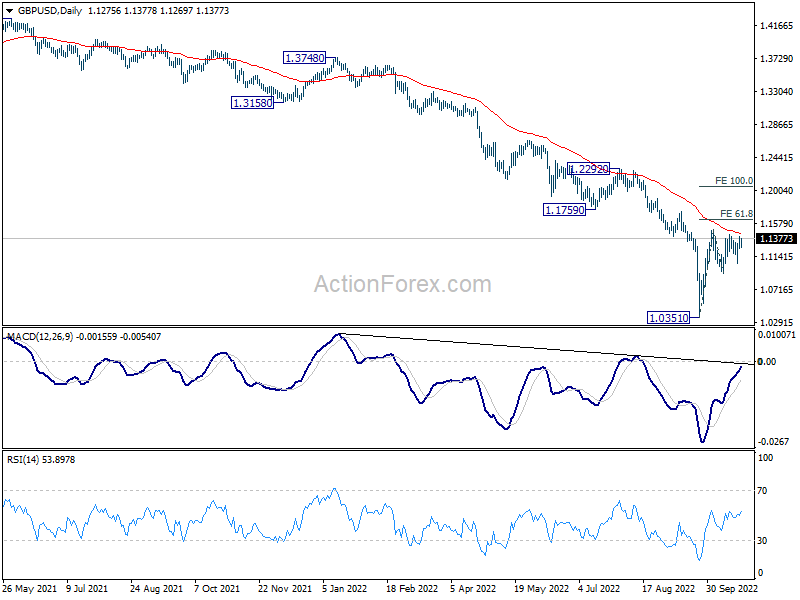

In the bigger picture, fall from 1.4248 (2018 high) is resuming long term down trend from 2.1161 (2007 high). Next target is 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. There is no scope of a medium term rebound as long as 1.1759 support turned resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Oct | 84.3 | 84 | 84.3 | 84.4 |

| 08:00 | EUR | Germany IFO Current Assessment Oct | 94.1 | 92.5 | 94.5 | |

| 08:00 | EUR | Germany IFO Expectations Oct | 75.6 | 74.9 | 75.2 | 75.3 |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Aug | 13.10% | 15.40% | 16.10% | 16.00% |

| 13:00 | USD | Housing Price Index M/M Aug | -0.70% | -0.70% | -0.60% | |

| 14:00 | USD | Consumer Confidence Oct | 105.6 | 108 |