Overall market sentiment is mixed today. European stocks are trading up together with US futures. But heavy selling was seen in Hong Kong and China stocks earlier. Commodity currencies appear to be weighed down by the negative side of the picture, while Dollar is firmer with European majors. Sterling is so far the better performer but there is no follow through buying. The Pound is awaiting news on whether Rishi Sunak will become the next UK Prime Minister. There is little reaction to the poor PMI data from Eurozone and the UK. Yen is mixed for now, slightly on the soft side.

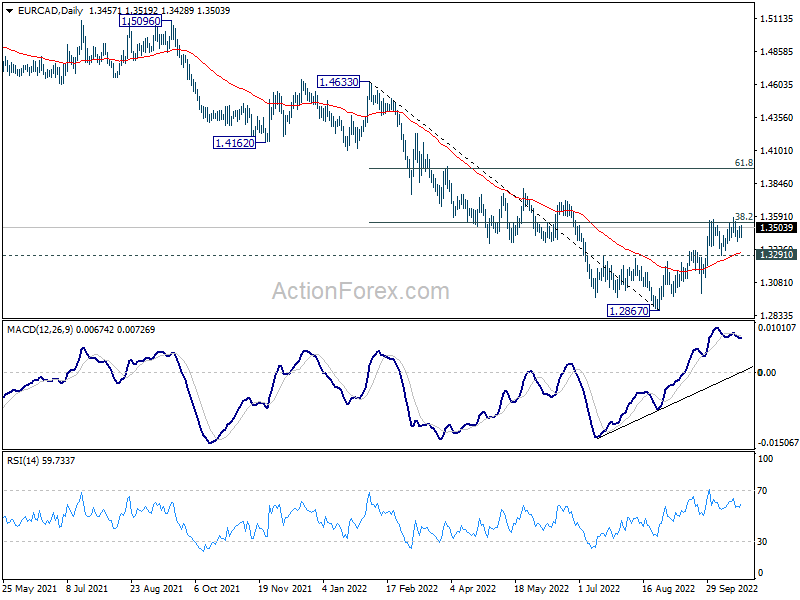

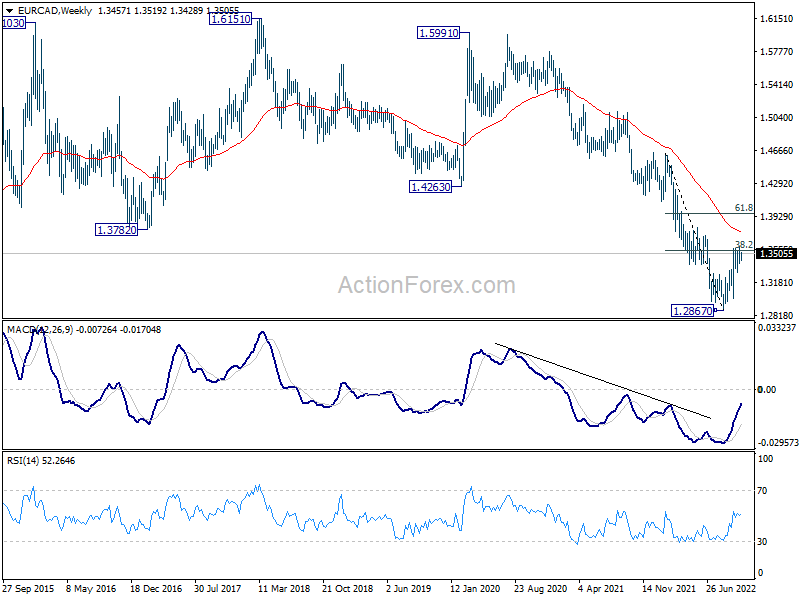

EUR/CAD is a pair to watch this week with ECB and BoC featured. Technically, rebound from 1.2867 short term bottom is in favor to continue as long as 1.3291 support holds. Sustained break of 38.2% retracement of 1.4633 to 1.2867 at 1.3542 will add to the case of medium term bullish reversal, and target 55 week EMA (now at 1.3748). However, rejection by 1.3542, followed by break of 1.3291, will resume larger down trend through 1.2867 low.

{kind=link}

{kind=link}

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 1.59%. CAC is up 1.67%. Germany 10-year yield is down -0.088 at 2.332. Earlier in Asia, Nikkei rose 0.31%. Hong Kong HSI dropped -6.36%. China Shanghai SSE dropped -2.02%. Japan 10-year JGB yield rose 0.0005 to 0.257.

UK PMI manufacturing fell to 47.2, a worryingly deep UK recession

UK PMI Manufacturing dropped further from 48.4 to 45.8 in October, a 29-month low. PMI Services dropped from 50.0 to 47.5, a 21-month low. PMI Composite dropped from 49.1 to 47.2, a 21-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “October’s flash PMI data showed the pace of economic decline gathering momentum after the recent political and financial market upheavals… GDP therefore looks certain to fall in the fourth quarter after a likely third quarter contraction, meaning the UK is in recession…

“The resulting elevated, albeit easing, price pressures look set to drive the Bank of England into further aggressive interest rate hikes. On top of the collapse in political stability, financial market stress and slump in confidence, these higher borrowing costs will add to speculation of a worryingly deep UK recession.”

Eurozone PMI composite dropped to 47.1, economy to contract in Q4, risks on downside

Eurozone PMI Manufacturing dropped from 48.4 to 46.6 in October, a 29-month low. PMI Services dropped from 48.8 to 48.2, a 20-month low. PMI Composite dropped from 48.1 to 47.1, a 23-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “The eurozone economy looks set to contract in the fourth quarter given the steepening loss of output and deteriorating demand picture seen in October, adding to speculation that a recession is looking increasingly inevitable.

“While October’s headline flash PMI is consistent with GDP falling at a modest rate of around 0.2%, demand is falling sharply and companies are increasingly growing worried over high inventories and weaker than expected sales, especially as winter approaches. The risks are therefore tilted towards the downturn accelerating towards the year-end.”

Japan refrains from commenting on currency intervention

Japan Finance Minister Shunichi Suzuki declined to confirm if there was intervention in the currency markets last Friday. But he reiterated, “we cannot tolerate excessive volatility caused by speculative moves, and we are ready to take necessary steps when needed…. we are in a situation where we are confronting speculative moves strictly.”

Masato Kanda, Vice Finance Minister for International Affairs also said, “we won’t comment” on whether Japan will intervene gain. He said, “we will take appropriate steps against excessive volatility 24 hours a day, 365 days a year.”

Chief Cabinet Secretary Hirokazu Matsuno also said, “we refrain from commenting specifically on any currency intervention”.

Japan PMI composite rose to 51.7, but manufacturing struggles

Japan PMI Manufacturing ticked down from 50.8 to 50.7 in October, weakest in 21 months. PMI Manufacturing Output improved slightly from 48.3 to 48.7. PMI Services rose from 52.2 to 53.0. PMI Composite also rose from 51.0 to 51.7.

Laura Denman, Economist at S&P Global Market Intelligence, said: “Latest flash PMI data has pointed to a further improvement in Japan’s private sector economy in October… The manufacturing sector, however, continued to struggle in the face of weak demand conditions and severe cost pressures… With inflationary pressures remaining elevated across the private sector, business confidence dipped to a six-month low.”

RBA Kent: Depreciation in AUD will have very modest uplift in prices

RBA Assistant Governor Christopher Kent said in a speech, “The Board expects to increase interest rates further in the period ahead, given the need to establish a more sustainable balance of demand and supply and in the face of a very tight labour market.” The “size and timing” of rate increases will depend on “incoming data” and “outlook for inflation and the labour market.”

Kent also said the appreciation of the US dollar will “add to the cost of imports for a time” because much the global trade is invoices in it. At the same time, rise in US interest rates will also “contribute to a decline in global inflation pressures”. The depreciation of Australia’s nominal trade-weighted exchange rate over the year to date will contribute only a “very modest uplift in the level of consumer prices over the period ahead”.

Australia PMI composite dropped to 49.6, renewed contraction

Australia PMI Manufacturing dropped from 53.5 to 52.8 in October, a 14-month low. PMI Services dropped from 50.6 to 49.0, a 9-month low. PMI Composite dropped from 50.9 to 49.6, a 9-month low.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence said: “Australia’s private sector saw renewed contraction in October with the service sector primarily showing signs of stress. A fall in demand for services was underpinned by higher interest rates and prices, altogether reflective of the detriments of aggressive monetary policy tightening and capacity constraints upon business activity.”

China posted solid production but weak retail sales data

After a delay amid the 20th Communist Party Congress last week, China released a batch of economic data today.

GDP grew 3.9% yoy in Q3, and beat expectation of 3.3% yoy. In September, industrial grew 6.3% yoy, faster than August’s 4.2% yoy, and beat expectation of 4.9% yoy. Retail sales, however, rose only 2.5% yoy, slowed from August’s 5.4% yoy, and missed expectation of 3.1% yoy. Fixed asset investment rose 5.9% ytd yoy, below expectation of 6.0%.

Also released, in USD term, exports rose 10.7% yoy in September. Imports rose 0.3% yoy. Trade surplus widened from USD 79.4B to USD 84.0B, above expectation of USD 81B.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9755; (P) 0.9812; (R1) 0.9919; More…

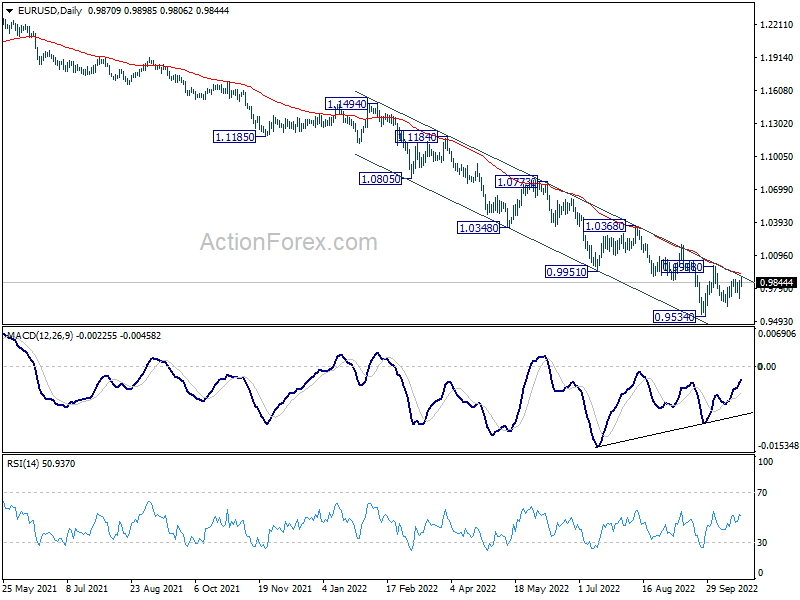

Range trading continues in EUR/USD and intraday bias stays neutral at this point. On the downside, break of 0.9630 bring retest of 0.9534 first. Firm break there will resume larger down trend. However, break of 0.9998 resistance will resume the rise from 0.9534, and carry larger bullish implications.

{kind=link}

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, break of 0.9998 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even with strong rebound. However, considering bullish convergence condition in daily MACD, firm break of 0.9998 will confirm medium term bottoming, and bring further rise back to 1.0368 resistance first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Oct P | 52.8 | 53.5 | ||

| 22:00 | AUD | Services PMI Oct P | 49 | 50.6 | ||

| 00:30 | JPY | Jibun Bank Manufacturing PMI Oct P | 50.7 | 51.3 | 50.8 | |

| 07:15 | EUR | France Manufacturing PMI Oct P | 47.4 | 47 | 47.7 | |

| 07:15 | EUR | France Services PMI Oct P | 51.3 | 51.5 | 52.9 | |

| 07:30 | EUR | Germany Manufacturing PMI Oct P | 45.7 | 47.2 | 47.8 | |

| 07:30 | EUR | Germany Services PMI Oct P | 44.9 | 44.8 | 45 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Oct P | 46.6 | 48 | 48.4 | |

| 08:00 | EUR | Eurozone Services PMI Oct P | 48.2 | 48.2 | 48.8 | |

| 08:30 | GBP | Manufacturing PMI Oct P | 45.8 | 48 | 48.4 | |

| 08:30 | GBP | Services PMI Oct P | 47.5 | 49 | 50 | |

| 13:45 | USD | Manufacturing PMI Oct P | 51.2 | 52 | ||

| 13:45 | USD | Services PMI Oct P | 49.2 | 49.3 |