Dollar surges broadly today as risk sentiment turns sour again while treasury yields continue to march higher. Yen is apparently weak, with Japan absent from intervention despite the steep decline. But Sterling and Swiss Franc are worse, Commodity currencies are also turning south, with Kiwi on the weaker side. Stronger than expected retail sales data from the UK and Canada are providing no support to the CAD.

Technically, USD/CHF’s strong rally today confirms up trend resumption. The question is when EUR/USD and GBP/USD would follow. Break of 0.9630 minor support in EUR/USD and 1.0922 minor support in GBP/USD will argue that both are ready for at least a retest on recent lows at 0.9534 and 1.0351.

{kind=link}

In Europe, at the time of writing, FTSE is down -1.02%. DAX is down -1.51%. CAC is down -1.97%. Germany 10-year yield is up 0.0905 at 2.493. Earlier in Asia, Nikkei dropped -0.43%. Hong Kong HSI dropped -0.42%. China Shanghai SSE rose 0.13%. Singapore Strait Times rose 0.18%. Japan 10-year JGB yield rose 0.0024 to 0.256.

Canada retail sales rose 0.7% mom in Aug, well above expectations

Canada retail sales rose 0.7% mom to CAD 61.8B in August, much better than expectation of 0.2% mom rise. Sales increased in 6 of 11 subsectors, representing 65% of retail trade. Excluding gasoline stations and motor vehicle and parts, sales also rose 0.9% mom, large increase since march.

In volume terms retail sales were up 1.1% mom.

Based on advance estimate, dales decreased -0.5% mom in September.

UK retail sales volume down -1.4% mom in Sep, value down -0.5% mom

UK retail sales volume dropped -1.4% mom in September, much worse than expectation of -0.5% mom. Sales values dropped -1.4% mom too. On a year earlier, sales volumes dropped -6.9% yoy while sales value rose 3.8% yoy.

Excluding fuel, sales volumes dropped -1.5% mom while sales values dropped -0.4% mom. On a year earlier, sales volume was down -6.2% yoy while sales value was up 3.3% yoy.

Comparing with pre-coronavirus level in February 2020, total retail sales were 12.0% higher in value terms but volumes were -1.3% lower.

Japan Suzuki: We are confronting speculators strictly

Japan stepped up verbal intervention as USD/JPY breaks above 150 level. Finance Minister Shunichi Suzuki warned today, “we are confronting speculators strictly.”

Yet, when asked if Yen was under attack by speculators, Suzuki said, “it’s inappropriate for me to comment on such a question under the current circumstances.”

Regarding BoJ policy, he said, “I’m not in a position to comment anything concrete. We’ll strive to maintain fiscal discipline with a major target of achieving primary budget surplus in fiscal 2025.”

Japan CPI core rose to 3% yoy in Sep

Japan headline CPI was unchanged at 3.0% yoy in September, below expectation of 3.1% yoy. CPI core (all items ex-fresh food) accelerated from 2.8% yoy to 3.0% yoy, matched expectations. CPI core-core (all items ex-fresh food and energy) accelerated from 1.6% to 1.8% yoy, below expectation of 2.0% yoy.

CPI core has now exceeded BoJ’s target for the 6th straight months, and hit the highest level since 1991 (excluding the effect of the 2014 sales tax hike). CPI core-core was also at the highest level since 2015. Yet, BoJ is seeing inflation as mostly driven by imports rather than domestic price pressures. This could be reflected in the 5.6% yoy rise in goods prices, and the sluggish 0.2% yoy rise in services prices.

NZ exports rose 37.% yoy in Sep, imports rose 16% yoy

New Zealand good exports rose 37% yoy or NZD 1.6B to NZD 6B in September. Goods imports rose 16% yoy or NZD 1.1B to NZD 7.6B. Monthly trade balance reported a deficit of NZD -1.6B.

Exports to all major trading partners were up, including China (+31% yoy), Australia (+33% yoy), USA (+13% yoy), EU (+21% yoy), and Japan (+42% yoy).

Imports from all major trading partners rose, except EU, including China (+20% yoy), EU (-5.3% yoy), Australia (+11% yoy), USA (+26% yoy), and Japan (+14% yoy).

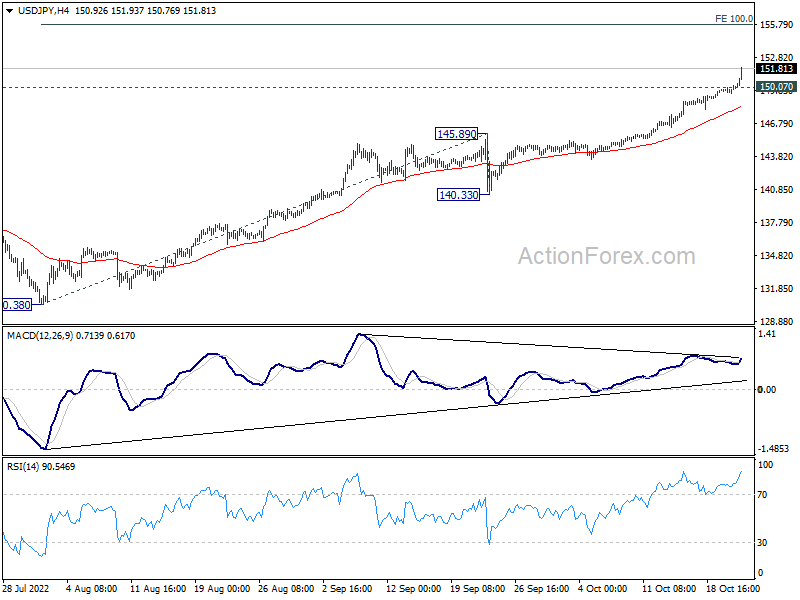

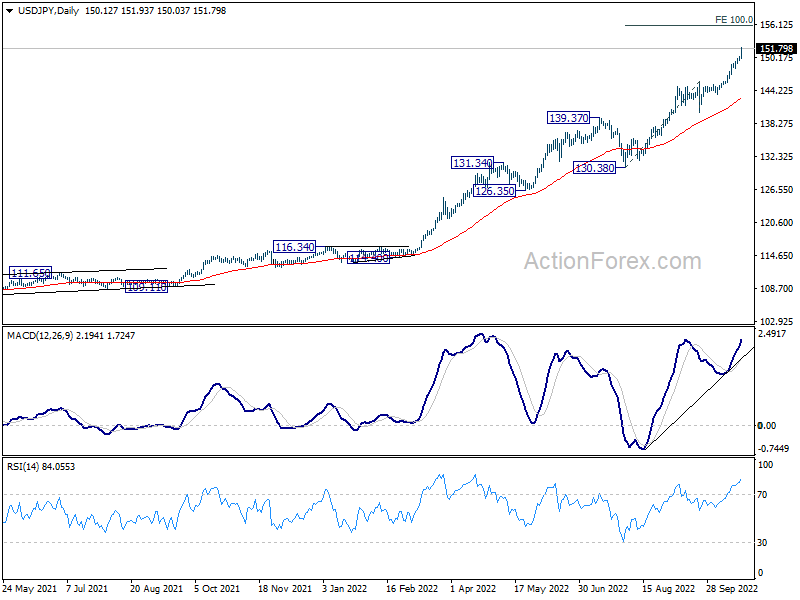

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.71; (P) 150.00; (R1) 150.44; More…

USD/JPY’s rally accelerates to as high as 151.93 so far. Intraday bias remains on the upside. Next target for the up trend is 100% projection of 130.38 to 140.33 from 145.89 at 155.84 next. On the downside, below 150.07 minor support will turn intraday bias neutral first. But near term outlook will remain bullish as long as 145.89 resistance turned support holds.

{kind=link}

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). 147.68 (1998 high) was already met and there is no clearly sign of topping yet. In any case, break of 140.33 support is needed to be the first sign of medium term topping. Otherwise, further rise is in favor to next target at 160.16 (1990 high).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -1615M | -1413M | -2447M | -2625M |

| 23:01 | GBP | GfK Consumer Confidence Oct | -47 | -52 | -49 | |

| 23:30 | JPY | National CPI Core Y/Y Sep | 3.00% | 3.00% | 2.80% | |

| 06:00 | GBP | Retail Sales M/M Sep | -1.40% | -0.50% | -1.60% | -1.70% |

| 06:00 | GBP | Retail Sales Y/Y Sep | -6.90% | -5.00% | -5.40% | -5.60% |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Sep | -1.50% | -0.30% | -1.60% | -1.70% |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Sep | -6.20% | -4.10% | -5.00% | -5.30% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 19.2B | 12.3B | 11.1B | 8.6B |

| 12:30 | CAD | New Housing Price Index M/M Sep | -0.10% | 0.20% | 0.10% | |

| 12:30 | CAD | Retail Sales M/M Aug | 0.70% | 0.20% | -2.50% | |

| 12:30 | CAD | Retail Sales ex Autos M/M Aug | 0.70% | 0.30% | -3.10% | |

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | -30.3 | -28.8 |