Dollar extends its near term rally in Asian session, with support from risk-off sentiment, while US 10-year yield is flirting with 4% handle. Yen is also firm, and has the potential to overwhelm the greenback if Japan steps into the markets again. Commodity currencies are the weakest one so far, with Aussie being the worst. European majors are mixed for now.

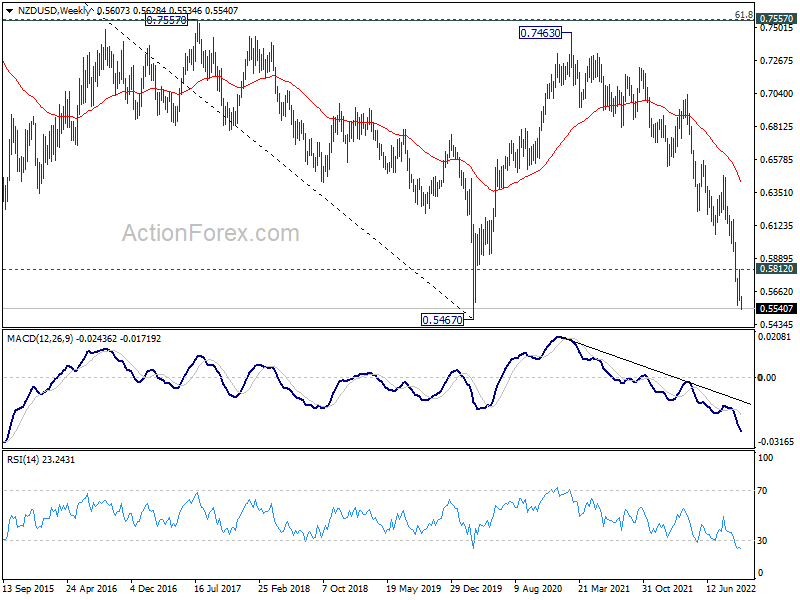

Technically, Dollar’s rally is making progress with break of 1.3832 resistance in USD/CAD and 0.9964 resistance in USD/CHF. NZD/USD has also resumed down trend by falling through 0.5563 support. Near term outlook will stay bearish in NZD/USD as long as 0.5812 support holds. Next target is pandemic low at 0.5467.

{kind=link}

In Asia, at the time of writing, Nikkei is down 2.54%. Hong Kong HSI is down -1.56%. China Shanghai SSE is up 0.40%. Singapore Strait times is down -0.12%. Japan 10-year JGB yield is down -0.0011 at 0.253.

Fed Brainard: Monetary policy will be restrictive for some time

Fed Vice Chair Lael Brainard said in a speech, “monetary policy will be restrictive for some time to ensure that inflation moves back to target over time.”

“It will take time for the cumulative effect of tighter monetary policy to work through the economy broadly and to bring inflation down.”

“In light of elevated global economic and financial uncertainty, moving forward deliberately and in a data-dependent manner will enable us to learn how economic activity, employment, and inflation are adjusting to cumulative tightening in order to inform our assessments of the path of the policy rate.” She said.

Japan Suzuki: Will take appropriate action on excessive Yen moves

Japanese Finance Minister Shunichi Suzuki reiterated today, “we will take appropriate action if there are any excessive moves” in Yen’s exchange rate. The comment came as Yen threatens to decline further towards the lowest level since 1998 again.

Suzuki also said, Japan is closely watching current FX moves with a “strong sene of urgency”. He planned to explain the stance on intervention at G20 meeting. He said that Japan have gained “certain understanding” from the US regarding intervention.

Australia Westpac consumer sentiment dropped to 83.7, RBA averted a much bigger fall

Australia Westpac Consumer Sentiment Index dropped -0.9% mom to 83.7 in October. Westpac said the index remains in “deeply pessimistic territory”, at a level comparable to the lows “briefly reached during the pandemic”, and during the Global Financial Crisis.

It added RBA’s smaller than expected 25bps rate hike “averted a much bigger fall” in sentiment. Sentiment amongst those sampled before the RBA decision showed a “depressing” 77.4 index read. But the post RBA “relief rebound” is “unlikely to be repeated in future months”.

Westpac expects four more consecutive 25bps rate hikes at RBA’s November, December, February and March meetings.

Australia NAB business conditions rose to 25, confidence dropped to 5

Australia NAB Business Confidence dropped from 10 to 5 in September. Business Conditions rose from 22 to 25. Trading conditions rose from 29 to 38. Profitability conditions was unchanged at 19. Employment conditions dropped from 17 to 16.

“Conditions are now higher than their pre-COVID peak, which shows just how strong demand is at present,” said NAB Chief Economist Alan Oster. “The current level of conditions are only exceeded by the post-lockdown surge in early 2021. Clearly, consumers are still finding a way to keep spending, with the very strong labour market, savings buffers and a broader post-pandemic recovery all playing a role.”

“Confidence eased in the month but is still around the long-run average in the history of the survey,” said Oster. “The confidence index has been volatile recently but is clearly a little lower than it was early in the year when the passing of the Omicron wave was providing a strong reason for optimism. Still, businesses are far from pessimistic.”

Looking ahead

UK employment data is the main focus today. Italy will release industrial production.

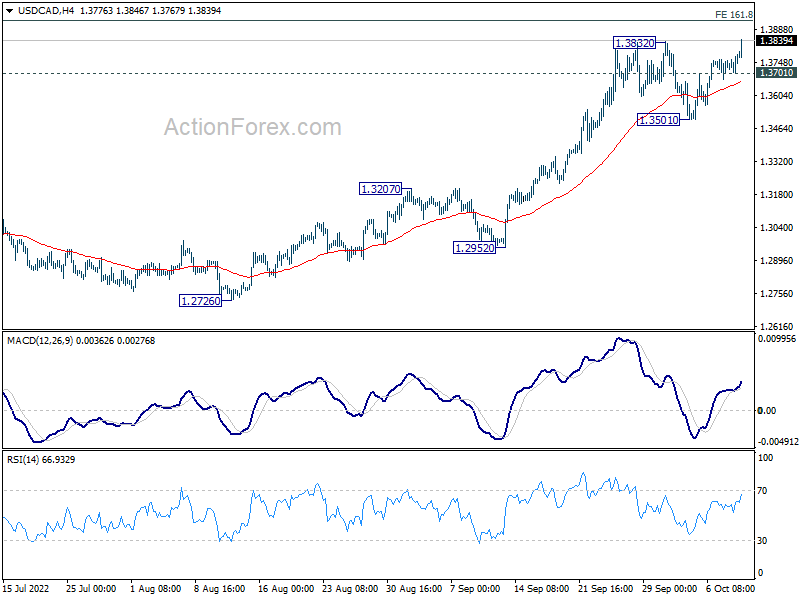

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3728; (P) 1.3756; (R1) 1.3808; More…

USD/CAD’s rally resumed by breaking 1.3832 and intraday bias is back on the upside. Current up trend should target 161.8% projection of 1.2005 to 1.2947 from 1.2401 at 1.3925. Decisive break there will target 200% projection at 1.4285. On the downside,e below 1.3701 minor support will turn intraday bias neutral first. but outlook will stays bullish as long as 1.3501 support holds, in case of retreat.

{kind=link}

In the bigger picture, up trend from 1.2005 (2021 low) is still in progress. Based on current impulsive momentum, it could be resuming long term up trend from 0.9056 (2007 low). Whether it is or it isn’t, retest of 1.4689 (2016 high) should be seen next. This will now remain the favored case as long as 1.3222 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Sep | 1.80% | 0.50% | ||

| 23:30 | AUD | Westpac Consumer Confidence Oct | -0.90% | 3.90% | ||

| 23:50 | JPY | Current Account (JPY) Aug | -0.53T | -0.47T | -0.63T | |

| 00:30 | AUD | NAB Business Confidence Sep | 5 | 10 | ||

| 00:30 | AUD | NAB Business Conditions Sep | 25 | 20 | ||

| 06:00 | GBP | Claimant Count Change Sep | 4.2K | 6.3K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Aug | 3.60% | 3.60% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Aug | 5.30% | 5.20% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Aug | 5.90% | 5.50% | ||

| 08:00 | EUR | Italy Industrial Output M/M Aug | 0.20% | 0.40% |