The forex markets are still staying in consolidative mode for now, awaiting guidance from US non-farm payrolls. For now, some Fed hawks are rather clear that there’s seeing no case for slowing down tightening yet. Fed fund futures are pricing in over 70% chance of another 75bps hike in November. But such expectations could be changed by today’s job report, as well as next week’s CPI data.

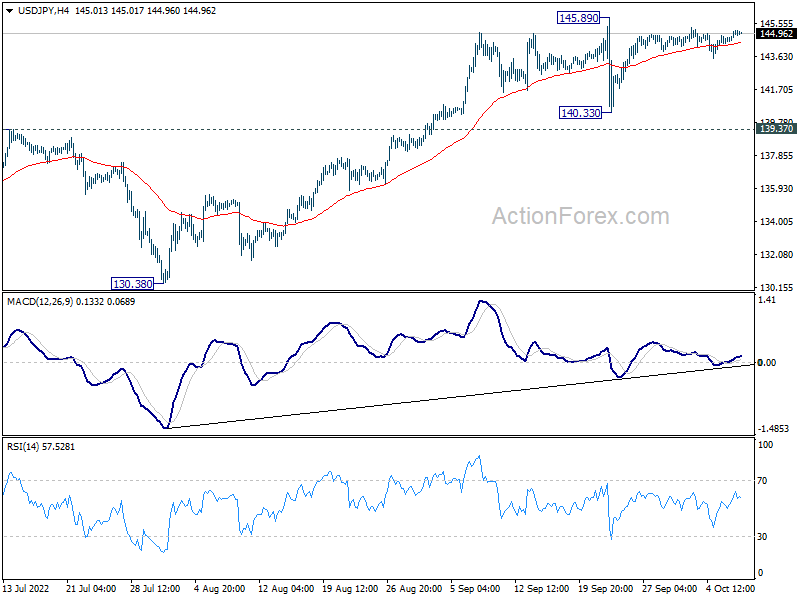

Technically, Yen would be an interesting one to watch today. Strong job data, including wage growth, could prompt US treasury yields higher, which might take USD/JPY through 145.89. Yet, firstly, risk-off sentiment in that case (good news is bad news for stock) could give Yen a floor. Secondly, and more importantly, Japan might intervene again to cushion Yen’s decline. The net result could mean deeper selloff in other Yen crosses. Let’s see.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.74%. Hong Kong HSI is down -1.32%. Singapore Strait Times is down -0.14%. Japan 10-year JGB yield is up 0.003 at 0.247. Overnight, DOW dropped -1.15%. S&P 500 dropped -1.02%. NASDAQ dropped -0.68%. 10-year yield rose 0.0067 to 3.826.

Fed Waller and Mester not seeing case for slower rate hike

Fed Governor Christopher Waller said in a speech yesterday, “Inflation is far from the FOMC’s goal and not likely to fall quickly. This is not the inflation outcome I am looking for to support a slower pace of rate hikes or a lower terminal policy rate”

Separately, Cleveland Fed President Loretta Mester echoed and said, “We have to bring interest rates up to a level that will get inflation on that 2% path, and I have not seen the compelling evidence that I need to see that would suggest that we could start reducing the pace at which we’re going,”

Chicago Fed President Charles Evans said, “We have to look at the momentum in sort of that central component of inflation, and that’s really the part that I believe has most of my colleagues and myself nervous about.” Be he declined to comment on whether Fed would continue with 75bps hike and noted, we “will have a discussion about that.”

Fed Kashkari: We’re quite a ways away from a pause

Minneapolis Fed President Neel Kashkari said, “Until I see some evidence that underlying inflation has solidly peaked and is hopefully headed back down, I’m not ready to declare a pause. I think we’re quite a ways away from a pause.”

“I fully expect that there are going to be some losses and there are going to be some failures around the global economy as we transition to a higher-interest rate environment, and that’s the nature of capitalism,” Kashkari said.

“We need to keep our eyes open for risks that could be destabilizing for the American economy as a whole. But to me, the bar to actually shifting our stance on policy is very high,” he said. “It should not be up to the Federal Reserve or the American taxpayer to bail people out.”

BoC Macklem: Simply put, there is more to be done

BoC Governor Tiff Macklem said in a speech yesterday, “We know we are still a long way from the 2% (inflation) target. We know it will take some time to get there. We also know there could be setbacks along the way, and we can’t afford to let high inflation become entrenched.”

“Simply put, there is more to be done. We will need additional information before we consider moving to a more finely balanced decision-by-decision approach,” he noted.

“We can’t control global developments. But we can use monetary policy to influence the balance between demand and supply in the Canadian economy and therefore ease domestic inflationary pressures over time,” Macklem also said.

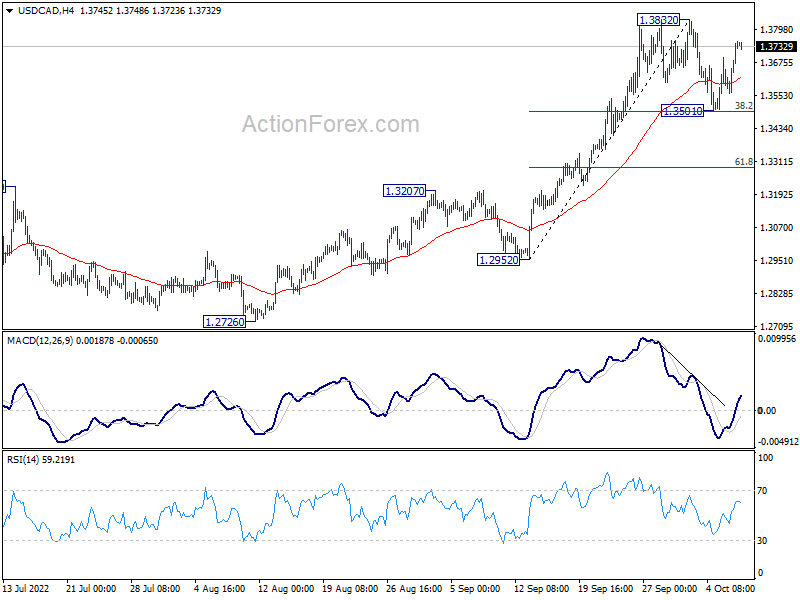

US and Canada employment awaited, USD/CAD ready for breakout

Focus turns to employment data from US and Canada today. US non-farm payroll report is expected to show 265k growth in September. Unemployment rate is expected to be unchanged at 3.7%. Average hourly earnings is expected to rise 0.3% mom in September.

Looking at related data, ISM manufacturing employment dropped from 54.2 to 48.7, back into contraction region. But ISM services employment rose from 50.2 to 53.0. ADP private employment grew a solid 208k, up from prior month’s 185k. Four-week moving average of initial claims dropped notably from 246k to 207.

Overall, the headline print and unemployment rate are unlikely to deviate much from expectations. The surprise factor is probably in wage growth.

Meanwhile, from Canada, employment is expected to rebound and grow 22.5k in September, with unemployment rate unchanged at 5.4%.

USD/CAD’s pull back from 1.3832 might have completed at 1.3501, after hitting 38.2% retracement of 1.2952 to 1.3832. An upside breakout looks ready after the above mentioned event risks are cleared. Nevertheless, even in case of another fall to extend the corrective pattern, downside should be contained by 1.3501.

{kind=link}

Elsewhere

Japan labor cash earnings rose 1.7% yoy in August, above expectation of 1.4% yoy. Household spending rose 5.1% yoy, below expectation of 6.8% yoy.

Swiss unemployment rate and foreign currency reserves, Germany import price and retail sales, France trade balance, and Italy retail sales will be released in European session. Job data from the US and Canada will be featured later in the day.

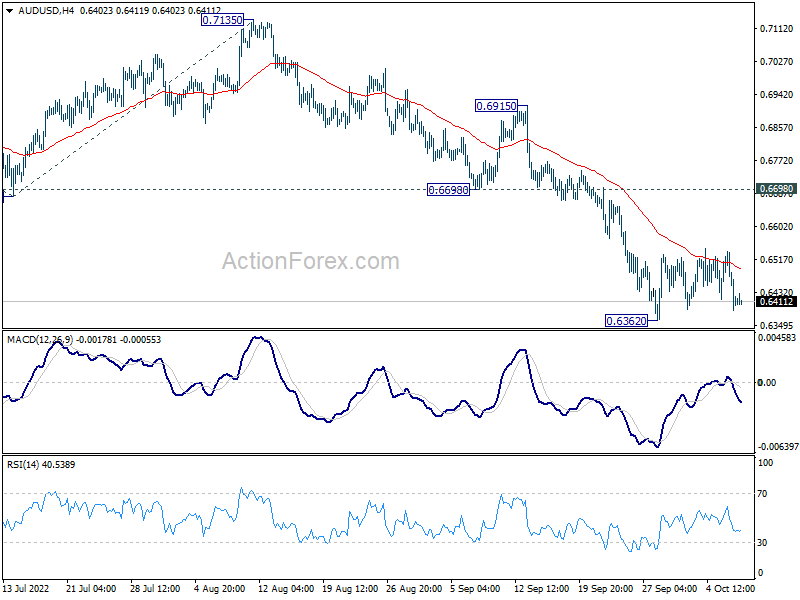

AUD/USD Daily Report

Daily Pivots: (S1) 0.6352; (P) 0.6447; (R1) 0.6503; More…

Intraday bias in AUD/USD remains neutral as consolidation from 0.6362 could extend. Another recovery cannot be ruled out, but upside should be limited well below 0.6698 support turned resistance. Break of 0.6362 will resume larger down trend to 100% projection of 0.7660 to 0.6680 from 0.7135 at 0.6155.

{kind=link}

In the bigger picture, down trend form 0.8006 (2021 high) is expected to continue as long as 0.7135 resistance holds. With 61.8% retracement of 0.5506 (2020 low) to 0.8006 at 0.6461 firmly taken out, next target is 0.5506 low. Medium term momentum will now be closely monitored to gauge the chance of break of 0.5506.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | 1.70% | 1.40% | 1.80% | |

| 23:30 | JPY | Overall Household Spending Y/Y Aug | 5.10% | 6.80% | 3.40% | |

| 05:00 | JPY | Leading Economic Index Aug P | 100.9% | 99.20% | 98.90% | |

| 05:45 | CHF | Unemployment Rate Sep | 2.10% | 2.10% | ||

| 06:00 | EUR | Germany Import Price Index M/M Aug | 2.20% | 1.40% | ||

| 06:00 | EUR | Germany Retail Sales M/M Aug | -1.00% | 1.90% | ||

| 06:45 | EUR | France Trade Balance (EUR) Aug | -13.2B | -14.5B | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | 860B | |||

| 08:00 | EUR | Italy Retail Sales M/M Aug | 1.00% | 1.30% | ||

| 12:30 | USD | Nonfarm Payrolls Sep | 265K | 315K | ||

| 12:30 | USD | Unemployment Rate Sep | 3.70% | 3.70% | ||

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.30% | 0.30% | ||

| 12:30 | CAD | Net Change in Employment Sep | 22.5K | -39.7K | ||

| 12:30 | CAD | Unemployment Rate Sep | 5.40% | 5.40% | ||

| 14:00 | USD | Wholesale Inventories Aug F | 1.30% | 1.30% |