Australian Dollar dips broadly today after RBA delivered a smaller than expected rate hike. But the selloff in Aussie is so relatively limited. New Zealand Dollar follows lower, ahead of tomorrow’s RBNZ rate decision. RBNZ is expected to hike by 50bps, but now it’s not totally certain given that tightening is already “mature”. Sterling is so far the stronger on today as rebound is making progress. Dollar and Euro are mixed while Yen and Swiss Franc are on the softer side.

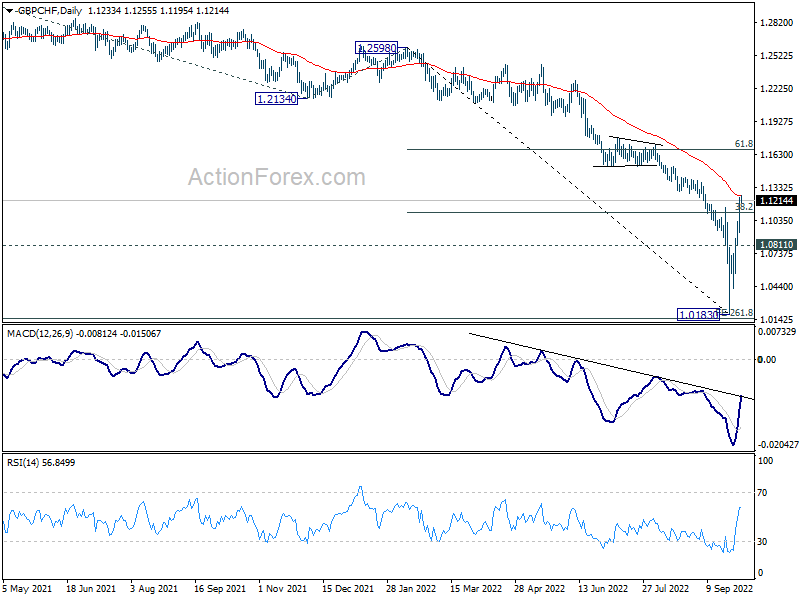

Technically, GBP/CHF powered through 38.2% retracement of 1.2598 to 1.0183 at 1.1106 yesterday. It’s now pressing 55 day EMA. Sustained break there will pave the way to 61.8% retracement at 1.1675. Such development would help lift Sterling elsewhere, including pushing GBP/USD back through prior support turned resistance at 1.14 handle.

{kind=link}

In Asia, at the time of writing, Nikkei is up 2.86%. Japan 10-year JGB yield is down -0.0128 at 0.231. Singapore Strait Times is up 0.82%. China and Hong Kong are on holiday. Overnight DOW rose 2.66%. S&P 500 rose 2.59%. NASDAQ rose 2.27%. 10-year yield dropped -0.153 to 3.651.

RBA hikes by only 25bps, maintain tightening bias

RBA raises the cash rate target by only 25bps to 2.60%, smaller than expectation of a 50bps hike. Tightening bias is maintained as the board “expects to increase interest rates further over the period ahead”. The size and timing of future hikes will continued to be determined by incoming data and the board’s assessment of inflation and labor market outlook.

In the accompanying statement, RBA said inflation is expected to “further increase” over the coming months. CPI would be around 7.75% over 2022, a little above 4% over 2023, and around 3% over 2024. The economy is “continuing to grow solidly” with national income boosted by a “record level of the terms of trade”. Labor markets is “very tight”. Wages growth is “continuing to pick up” but “remains lower than in other advanced economies” with high inflation.

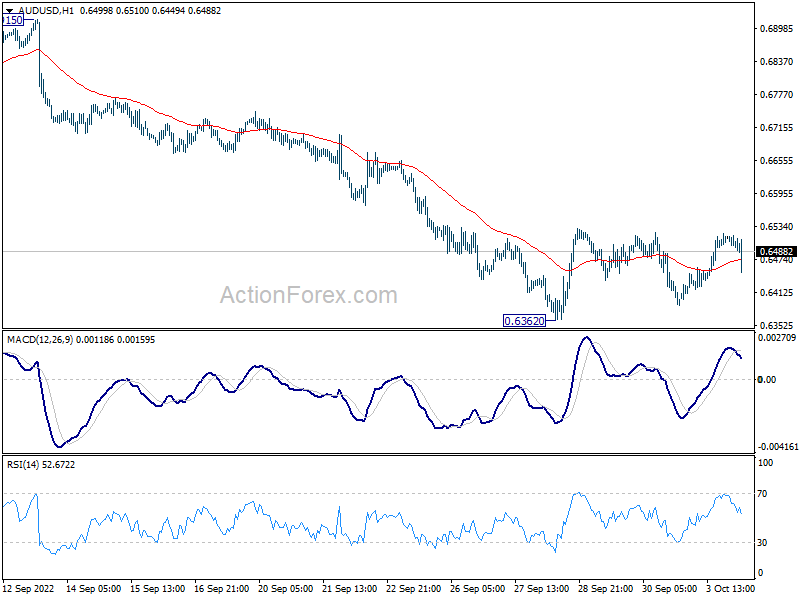

AUD/USD dips slightly after the smaller than expected rate hike, but there is no follow through selling. Consolidation pattern from 0.6362 is still in progress with bearish bias for downside breakout at a later stage.

{kind=link}

BoE Mann: Premature to judge how mini-budget affect monetary policy trajectory

BoE MPC member Catherine Mann said yesterday that it’s “premature” to judge the extent of UK Prime Minister Liz Truss’s budget is going to affect “monetary policy trajectory decisions”.

“I people don’t have to spend their money on heating their apartments, or homes, they are now we’re in a position to redirect some of that spending on to other goods and services,” she added. “So it’s that ability to redirect expenditures on goods and services, that becomes an important consideration for the monetary policy trajectory.”

Mann also expressed her concern that inflation expectations are “drifting” away from BoE’s anchor. “I do see increasingly embedded inflation, I do see inflation expectations drifting, I do see a sterling depreciation spillover and I do see daylight between real incomes and real consumption possibilities,” she said.

Fed Williams: Our job on inflation is not yet done

New York Fed President John Williams said yesterday, “Clearly, inflation is far too high, and persistently high inflation undermines the ability of our economy to perform at its full potential. Tighter monetary policy has begun to cool demand and reduce inflationary pressures, but our job is not yet done.”

He expects inflation to ease to 3% next year, and move “close to our 2% goal in the next few years”. “To help rein in demand to levels consistent with supply—and therefore bring inflation down—monetary policy needs to do its job,” Williams said. “The FOMC is taking strong actions toward that end.”

On the data front

New Zealand NZIER business confidence rose from -65 to -42 in Q3. Australia AiG performance of manufacturing index rose from 49.3 to 50.2 in September. Japan Tokyo CPI core rose from 2.6% yoy to 2.8% yoy in September, matched expectations.

Looking ahead, Eurozone PPI and US factor orders will be featured.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1159; (P) 1.1247; (R1) 1.1408; More…

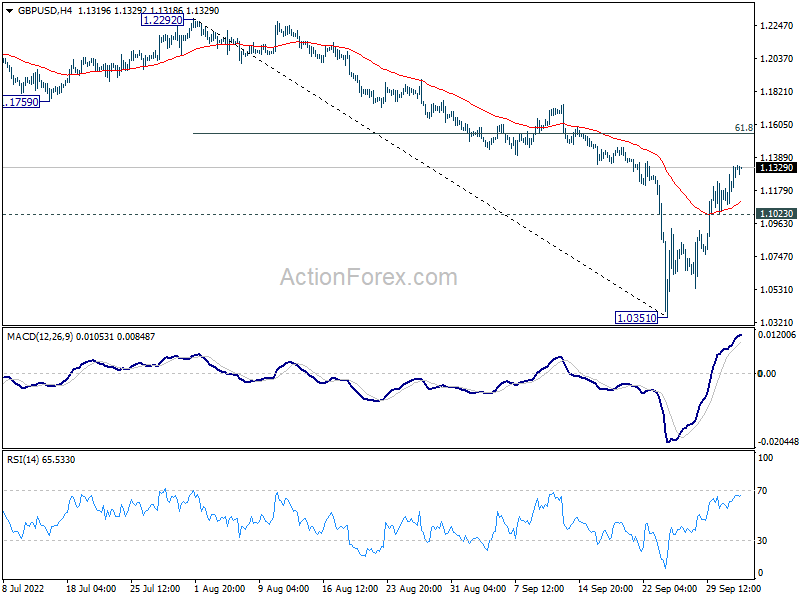

Intraday bias in GBP/USD stays on the upside at this point. Rise from 1.0351 short term bottom is in progress. Further rally would be seen to 61.8% retracement of 1.2292 to 1.0351 at 1.1551. Strong resistance could be seen around 55 day EMA (now at 1.1614) to limit upside on first attempt. On the downside, below 1.1023 minor support will turn intraday bias neutral first.

{kind=link}

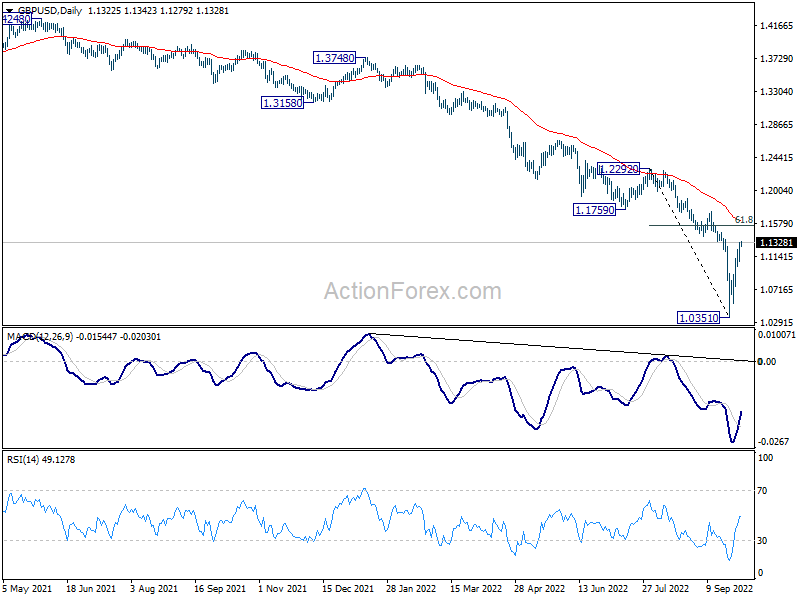

In the bigger picture, fall from 1.4248 (2018 high) is resuming long term down trend from 2.1161 (2007 high). Next target is 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. There is no scope of a medium term rebound as long as 1.1759 support turned resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q3 | -42 | -65 | ||

| 21:30 | AUD | AiG Performance of Mfg Index Sep | 50.2 | 49.3 | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Sep | 2.80% | 2.80% | 2.60% | |

| 23:50 | JPY | Monetary Base Y/Y Sep | -3.30% | 0.60% | 0.40% | |

| 00:30 | AUD | Building Permits M/M Aug | 28.10% | 9.00% | -17.20% | -18.20% |

| 03:30 | AUD | RBA Interest Rate Decision | 2.60% | 2.85% | 2.35% | |

| 09:00 | EUR | Eurozone PPI M/M Aug | 4.90% | 4.00% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Aug | 43.20% | 37.90% | ||

| 14:00 | USD | Factory Orders M/M Aug | 0.30% | -1.00% |