The forex markets are overall mixed. Dollar retreated overnight following the rebound in stocks, but regained some ground in Asian session. Traders are holding their bets for now, ahead of the meetings of four major central banks later in the week, including Fed, BoE, SNB and BoJ. Canadian inflation data, nevertheless, could trigger some volatility in Loonie today first.

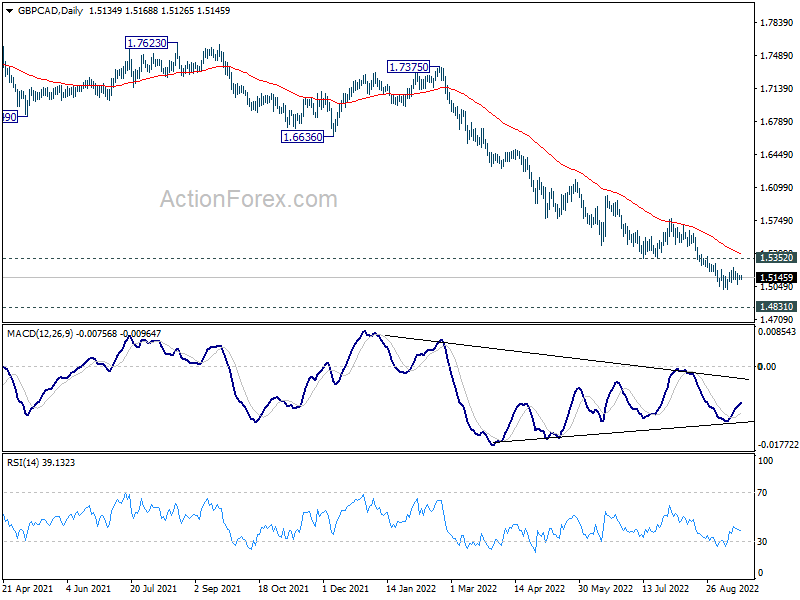

Technically, GBP/CAD is one that worth watching in the coming days. While the Pound has been weak, even GBP/USD could’s get rid of 1.14 handle (pandemic low) cleanly for now. Considering loss of downside momentum in GBP/CAD, as seen in daily MACD, and the proximity to 2010 low at 1.4831, there is prospect of a bounce. But, break of 1.5352 support turned resistance is needed to confirm short term bottoming first. The development will hinge on today’s Canada CPI data, and BoE rate decision on Thursday.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.39%. Hong Kong HSI is up 1.41%. China Shanghai SSE is up 0.40%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is down -0.0071 at 0.250. Overnight, DOW rose 0.64%. S&P 500 rose 0.69%. NASDAQ rose 0.76%. 10-year yield rose 0.042 to 3.490.

Japan CPI core rose to 3% yoy in Aug, highest in 31 years

Japan CPI accelerated from 2.6% yoy to 3.0% yoy in August, above expectation of 2.6% yoy. CPI core (ex-fresh food), rose from 2.4% yoy to 2.8% yoy, above expectation of 2.7% yoy. CPI core-core (ex-fresh food, energy), also rose from 1.2% yoy to 1.6% yoy, but missed expectation of 1.7% yoy.

CPI core, the BoJ watched reading, hit the highest level in 31 years since 1991, excluding the effect of sales tax hike. Even including the impact of sales tax, the reading was still the highest in nearly 8 years.

BoJ is widely expected to continue to stand pat, and maintain negative interest rate later this week. But there are expectations that core inflation could hit 3% later in the year, and stay above the 2% target in the near term. That might start to change BoJ’s view on prices and policy at a later stage.

RBA minutes: Slower tightening comes with higher rates

Minutes of RBA’s September 6 meeting revealed that there were discussions on whether to hike by 25bps or 50bps. But, “given the importance of returning inflation to target, the potential damage to the economy from persistent high inflation and the still relatively low level of the cash rate, the Board decided to increase the cash rate by a further 50 basis points.”

RBA reiterated that there will be further interest rate hikes “over the months ahead”, but it’s it “not on a pre-set path”. The full effects of higher interest rates were “yet to be felt” on mortgages, activity and inflation.

The board was “mindful” that the path to bring inflation back to target “needed to account for the risks to growth and employment. RBA is seeking to return inflation to target “while keeping the economy on an even keel”.

Size of timing of future rate hikes will be “guided by the incoming data” and outlook for inflation and job market, and risks. “All else equal, members saw the case for a slower pace of increase in interest rates as becoming stronger as the level of the cash rate rises”.

Looking ahead

Germany PPI, Swiss SECO economic forecasts, and Eurozone current account will be released in European session. Later in the day, Canada CPI will take center stage. US will publish building permits and housing starts.

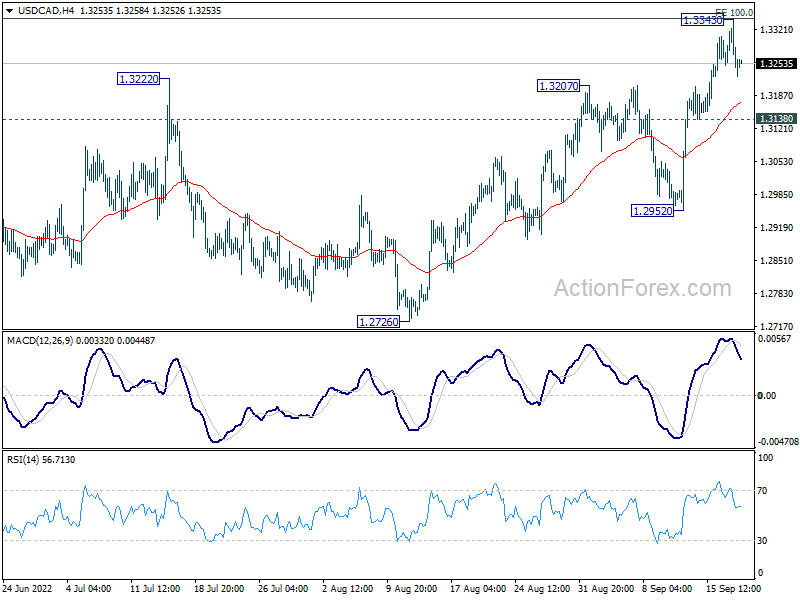

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3217; (P) 1.3281; (R1) 1.3316; More…

USD/CAD retreated after hitting 1.3343, meeting 100% projection of 1.2005 to 1.2947 from 1.2401 at 1.3343. Intraday bias is turned neutral for consolidations first. Downside of retreat should be contained by 1.3138 support to bring another rally. Sustained break of 1.3343 will pave the way to medium term fibonacci level at 1.3650. However, firm break of 1.3138 will bring deeper pull back towards 1.2952 support instead.

{kind=link}

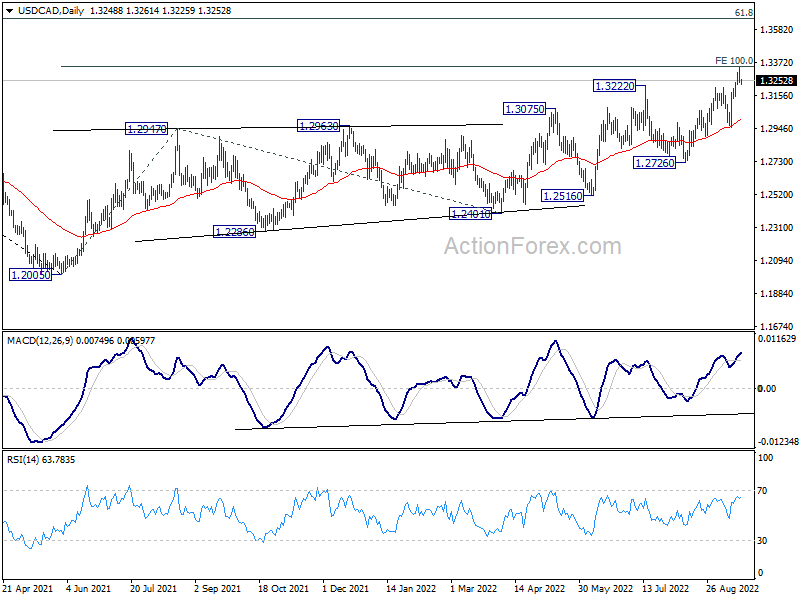

In the bigger picture, down trend from 1.4667 (2020 high) should have completed at 1.2005, after defending 1.2061 long term cluster support. Rise from there should target 61.8% retracement of 1.4667 to 1.2005 (2021 low) at 1.3650. This will remain the favored case now as long as 1.2716 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Aug | 2.80% | 2.70% | 2.40% | |

| 01:30 | AUD | RBA Minutes | ||||

| 06:00 | EUR | Germany PPI M/M Aug | 1.50% | 5.30% | ||

| 06:00 | EUR | Germany PPI Y/Y Aug | 37.50% | 37.20% | ||

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 08:00 | EUR | Current Account (EUR) Jul | 5.3B | 4.2B | ||

| 12:30 | USD | Building Permits Aug | 1.62M | 1.69M | ||

| 12:30 | USD | Housing Starts Aug | 1.46M | 1.45M | ||

| 12:30 | CAD | CPI M/M Aug | -0.10% | 0.10% | ||

| 12:30 | CAD | CPI Y/Y Aug | 7.30% | 7.60% | ||

| 12:30 | CAD | CPI Common Y/Y Aug | 5.60% | 5.50% | ||

| 12:30 | CAD | CPI Median Y/Y Aug | 5.10% | 5.00% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 5.50% | 5.40% |