Selloff in Pound catches most currency related headlines today, as it slumped to a 37-year low against Dollar. The decline came after data showed retail sales contracted in both volume and value term in August, indicating that inflation was already biting into spending. In the background, the UK economic is already in recession. Still for now, commodity are even worse for the week. Dollar is the biggest winner, followed by Swiss Franc and Yen. The final picture will depend on development in risk sentiment in the last few hours.

Technically, EUR/USD is so far resilient. But being capped below 4 hour 55 EMA, risk remains mildly on the downside for the near term. Retest of 0.9863 is in favor. Break there will resume larger down trend, and align the outlook with GBP/USD.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.32%. DAX is down -1.73%. CAC is down -1.49%. Germany 10-year yield is down -0.006 at 1.763. Earlier in Asia, Nikkei dropped -1.11%. Hong Kong HSI dropped -0.89%. China Shanghai SSE dropped -2.30%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield dropped -0.0001 to 0.257.

Canada wholesale sales dropped -0.6% mom in Jul, led by personal and household goods

Canada wholesale sales dropped -0.6% mom in July to CAD 80.2B, worse than expectation of -0.4% mom. That followed two consecutive months of record-high sales in May and June.

Declines in the personal and household goods subsector led the losses for July, followed by the building material and supplies, and the motor vehicle and motor vehicle parts and accessories subsectors. Sales fell in five of seven subsectors, which represented 63% of wholesale sales.

ECB de Guindos hopes recent depreciation in Euro is reversed in near future

ECB Vice President Luis de Guindos told a Portuguese newspaper Expresso, “the slowdown of the economy is not going to ‘take care’ of inflation on its own.”

“The slowdown of the economy will reduce demand pressures, which will lower inflation,” he added. “But, simultaneously, we have to act from the monetary policy standpoint to keep inflation expectations anchored and avoid second-round effects.”

“We need to continue the normalization of monetary policy,” he said. “More hikes might come in the next few months — how many times and by how much will depend fundamentally on the data — and we underscore our full determination to make inflation converge toward our definition of price stability”

“Further depreciation of the euro could be detrimental to inflationary pressures. On the contrary, if the euro stopped depreciating, this could be positive and support the fight against inflation. I hope that the recent depreciation trend is reversed in the near future”, he also noted.

Eurozone CPI finalized at 9.1% yoy in Aug, core CPI at 4.3% yoy

Eurozone CPI was finalized at 9.1% yoy in August, up from 8.9% yoy in July. A year earlier, the rate was only 3.0% yoy. CPI core (all item ex-energy, food, alcohol and tobacco) was finalized at 4.3%, up from prior month’s 4.0% yoy. The highest contribution to the annual Eurozone inflation rate came from energy (3.95%), followed by food, alcohol & tobacco (2.25%), services (1.62%) and non-energy industrial goods (1.33%).

EU CPI was finalized at 10.1%, up from 9.8% a month ago. The lowest annual rates were registered in France (6.6%), Malta (7.0%) and Finland (7.9%). The highest annual rates were recorded in Estonia (25.2%), Latvia (21.4%) and Lithuania (21.1%). Compared with July, annual inflation fell in twelve Member States and rose in fifteen.

UK retail sales volume dropped -1.6% mom in Aug, sales value also down -1.7% mom

UK retail sales volume dropped -1.6% mom, -5.4% yoy in August, worst than expectation of -0.6% mom, -4.2% yoy. Ex-fuel sales volume dropped -1.6% mom, -5.0% yoy, versus expectation of -0.7% mom, -3.4% yoy.

Retail sales value also dropped -1.7% mom while ex-fuel sales value dropped -1.4% mom. On a year earlier, headline sales value rose 5.4% yoy while ex-fuel sales value rose 3.7% yoy.

RBA Lowe: Rate at 2.35% is still too low

RBA Governor Philip Lowe told the House of Representatives Standing Committee on Economics, interest rate at 2.35% is “still too low”. He added that over the longer term, the cash rate “should at least average the mid point of the inflation target”, which is 2.5%, if not a bit higher. Also, an average interest rate of about 3% was “possible”, and we’ll cycle around some number between 2.5 and 3.5.”

Lowe also warned that the longer inflation stays above 3%, “the more difficult it’s going to become” for Australians. If that. happens “then we have higher interest rates and a recession, which is damaging. “So we’ve got two difficult kind of positions at the moment: some pain now and hopefully real wages start rising again next year against the risk of not doing anything, just sitting on our hands and having inflation stay higher.”

NZ BusinessNZ manufacturing rose to 54.9, improving tone around underlying growth

New Zealand BusinessNZ Performance of Manufacturing Index rose slightly from 53.5 to 54.9 in August. Production rose from 50.8 to 54.6. Employment rose from 52.9 to 53.6. New orders rose from 50.8 to 59.2. Finished stocks rose from 48.7 to 50.8. Deliveries rose from 50.1 to 53.7.

BNZ Senior Economist, Craig Ebert stated ” that manufacturing production, in general, was holding its own in Q2, rather than drooping, was portrayed in the PMI readings for April May and June. And in July and August the PMI has moved on to suggest an improving tone around underlying growth.”

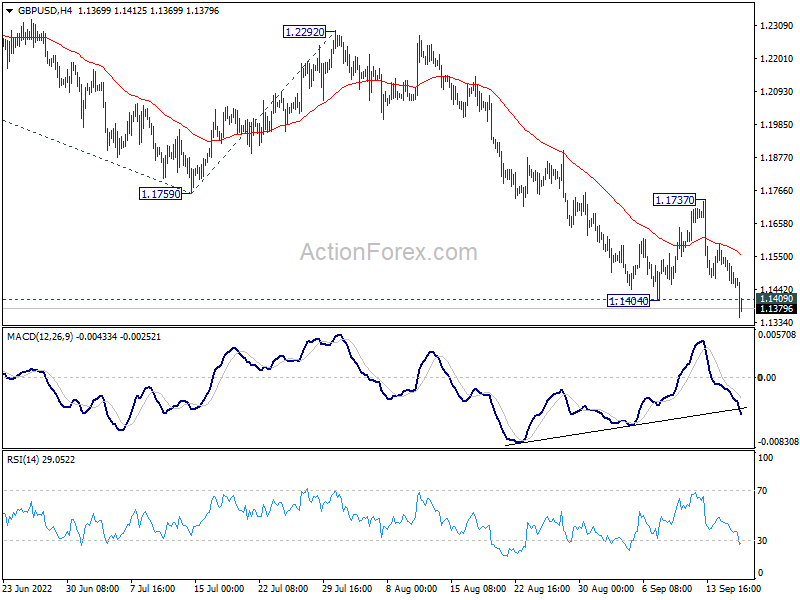

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1434; (P) 1.1495; (R1) 1.1529; More…

Break of 1.1404/9 support zone indicates down trend resumption in GBP/USD. Intraday bias is back on the downside for 61.8% projection of 1.3748 to 1.1759 from 1.2292 at 1.1063. On the upside, break of 1.1737 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

{kind=link}

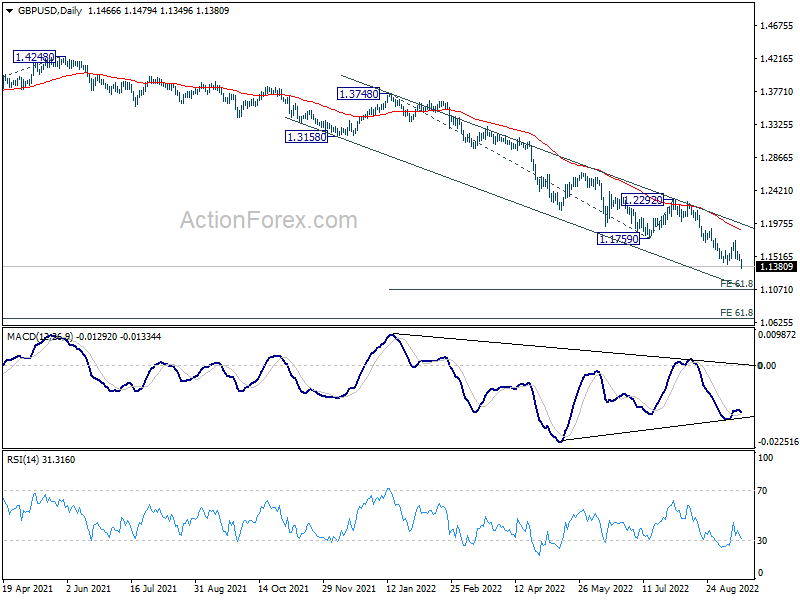

In the bigger picture, based on current momentum, fall from 1.4248 (2018 high) is probably resuming long term down trend from 2.1161 (2007 high). Sustained break of 1.1409 will target 61.8% projection of 1.7190 (2014 high) to 1.1409 (2020 low) from 1.4248 (2021 high) at 1.0675. This will remain the favored case for now as long as 1.2292 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Aug | 54.9 | 52.7 | ||

| 02:00 | CNY | Retail Sales Y/Y Aug | 5.40% | 3.20% | 2.70% | |

| 02:00 | CNY | Industrial Production Y/Y Aug | 4.20% | 4.00% | 3.80% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Aug | 5.80% | 5.60% | 5.70% | |

| 06:00 | GBP | Retail Sales M/M Aug | -1.60% | -0.60% | 0.30% | 0.40% |

| 06:00 | GBP | Retail Sales Y/Y Aug | -5.40% | -4.20% | -3.40% | -3.20% |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Aug | -1.60% | -0.70% | 0.40% | |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Aug | -5.00% | -3.40% | -3.00% | |

| 08:00 | EUR | Italy Trade Balance (EUR) Jul | -0.36B | -1.50B | -2.17B | -2.51B |

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | 9.10% | 9.10% | 9.10% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | 4.30% | 4.30% | 4.30% | |

| 12:30 | CAD | Wholesale Sales M/M Jul | -0.60% | -0.40% | 0.10% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Sep P | 59.8 | 58.2 |