Dollar is staying soft in consolidation today, as traders are clearly still cautiously waiting for rate clues from Fed Chair Jerome Powell’s Jackson Hole speech tomorrow. Yen is also mixed despite surging benchmark treasury yields. Movements are mainly found in Aussie and Kiwi, on rallies, which are lifted by China’s new stimulus plan. On the other hand, European majors the weakest ones for now.

Technically, while Dollar’s retreat could extend further, some levels need to be broken to indicate persistence in selling. Otherwise, Dollar rally could come back any time. The levels include 1.0121 resistance in EUR/USD, 1.2002 resistance in GBP/USD, 0.9500 support in USD/CHF, and 1.2826 support in USD/CAD.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is up 0.05%. CAC is down -0.21%. Germany 10-year yield is down -0.018 at 1.353. Earlier in Asia, Nikkei Rose 0.58%. Hong Kong HSI rose 3.63%. China Shanghai SSE rose 0.97%. Singapore Strait Times rose 0.44%. Japan 10-year JGB yield rose 0.0059 to 0.230.

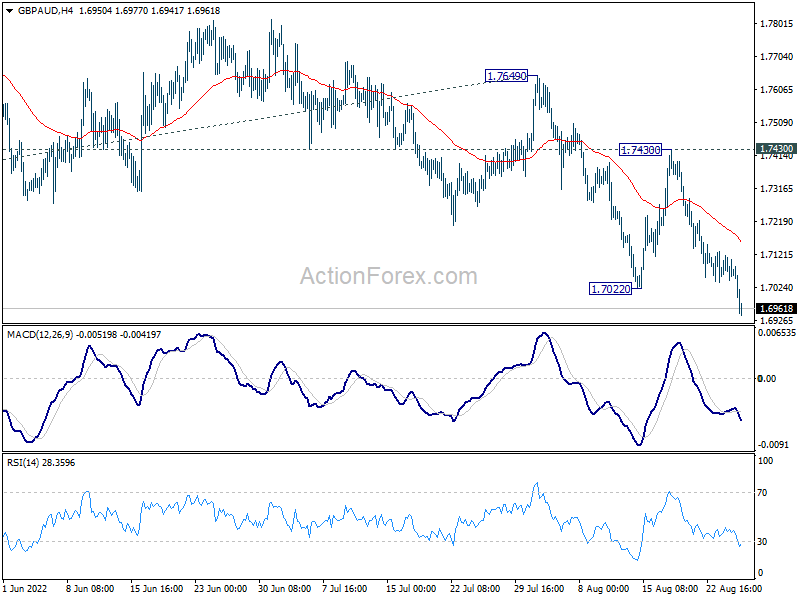

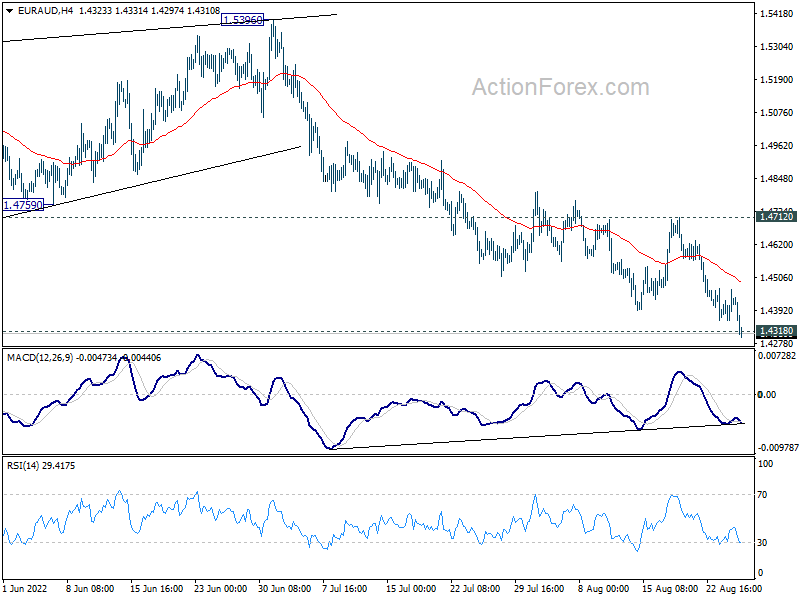

GBP/AUD resumes down trend, EUR/AUD breaking down

While Dollar is consolidating ahead of Jackson Hole Symposium, Australian Dollar is taking up some buying, in particular against Europeans. The Aussie is apparently given a lift after China unveiled new stimulus package of RMB 300B (around USD 44B). The news also lifted Hong Kong HSI up 3.63 today. On the other hand, Euro and Sterling are feeling heavy as concern over further weaponization of natural gas supply by Russia.

GBP/AUD’s down trends resumes today by breaking through 1.7022 low. While the rebound from 1.7022 was strong, it was limited well below 1.7649 resistance, as well as 55 day EMA. Near term bearishness is clearly maintained.

For now, outlook will stay bearish as long as 1.7430 resistance holds, even in case of another strong recovery. Next target is 61.8% projection of 1.9218 to 1.7171 from 1.7649 at 1.6384.

{kind=link}

{kind=link}

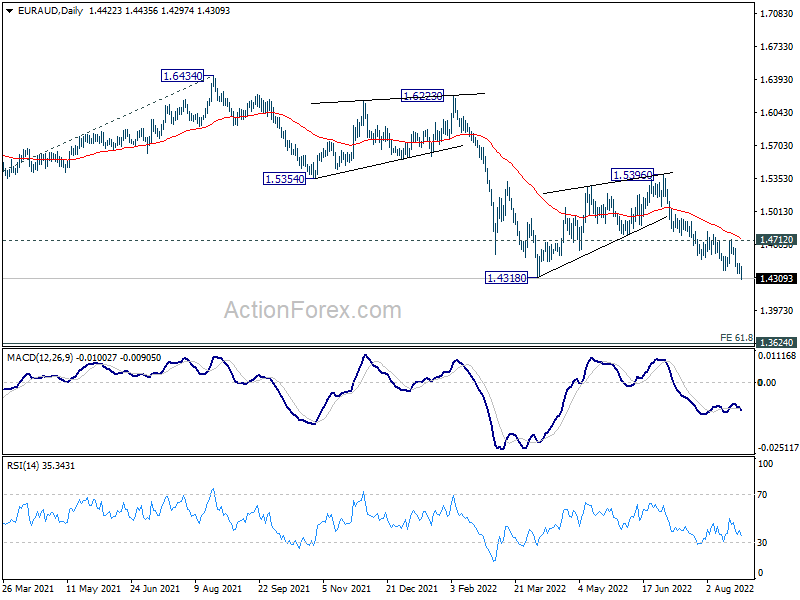

EUR/AUD is also trying to break through 1.4318 low. Sustained trading below there will confirm resumption of larger down trend. Next target is 1.3624 (2017 low). Outlook will stay bearish as long as 1.4712 resistance holds, in case of recovery.

{kind=link}

{kind=link}

US initial jobless claims dropped to 243k, below expectations

US initial jobless claims dropped -2k to 243k in the week ending August 2, below expectation of 256k. Four-week moving average of initial claims rose 1.5k to 247.

Continuing claims dropped -19k to 1415k in the week ending August 13. Four-week moving average of continuing claims rose 12.5k to 1425k.

US GDP contracted -0.6% annualized in Q2, less than first estimate

Based on the second estimate, US GDP contracted at -0.6% annualized rate in Q2, comparing to first estimate of -0.9%, PCE price index and core PCE price index were left unchanged at 7.1% and 4.4% respectively.

BEA said: “The decrease in real GDP reflected decreases in private inventory investment, residential fixed investment, federal government spending, and state and local government spending, that were partly offset by increases in exports and consumer spending. Imports, which are a subtraction in the calculation of GDP, increased”.

ECB accounts: A very large number of members supported 50bps hike

In the accounts of ECB’s July 20-21 meeting, it’s noted that “a very large number of members” agreed that it was appropriate to hike interest rates by 50bps. The 50bps hike was seen as “warranted in view of the worsening of the inflation outlook since the Governing Council’s June meeting”.

“Some members” argued in favor of a 25bps hike as that was the “intended move communicated” at the June meeting. Also, “with recession risks looming25bps hike was seen as more in line with a “gradual monetary policy normalization.” It’s also warned that deviation from earlier guidance would “add to the prevailing market uncertainties”. But some also argued that a 50bps hike provided more clarity for market participants.

It’s also emphasized that the 50bps hike “did not constitute an upward shift in the interest rate path but rather a frontloading of the policy normalisation.” As for September meeting, there was broad support to move to a “meeting-by-meeting approach” to interest rates.

Germany Ifo Business Climate ticked down to 88.5, trade deteriorates further

Germany Ifo Business Climate dropped slightly from 88.7 to 88.5 in August, above expectation of 86.7. Current Assessment index ticked down from 97.7 to 97.5. Expectations Index also edged down from 80.4 to 80.3.

By sector, manufacturing was unchanged at -6.9. Services rose from 1.0 to 1.3. Trade dropped further from -21.6 to -25.8. Constructions improved from -16.2 to -14.5.

Ifo said, “uncertainty among the companies remains high, and the German economy as a whole is expected to shrink in the third quarter.”

For trade, Ifo said that “many enterprises are facing a dilemma: high inflation is dragging down their business, but they can hardly avoid raising prices due to increased costs.”

BoJ Nakamura: Cannot achieve price target in a sustained, stable fashion yet

BoJ board member Toyoaki Nakamura said in a speech that “Japan’s economy is still in the midst of recovering from the pandemic-induced slump.”

“Shifting to a monetary tightening stance, at a time when demand remains short of supply, would hurt the economy and act as a big restraint to household and business activity,” he said.

“While core consumer inflation may accelerate toward year-end due to rising prices of energy, food and durable goods, such a boost will likely dissipate,” he noted. “Japan is not yet in a situation where it can achieve our price target in a sustained, stable fashion”.

New Zealand retail sales volume down -2.3% qoq in Q2, sales value relatively unchanged

New Zealand retail sales volume declined -2.3% qoq in Q2 to NZD 26B, worse than expectation of 1.7% qoq rise. 10 of 15 industries had lower seasonally adjusted sales volumes comparing with Q1.

Retail sales value was relatively unchanged, up slightly by NZD 1.1m to NZD 29B. 8 of 15 industries had lower seasonally adjusted sales values.

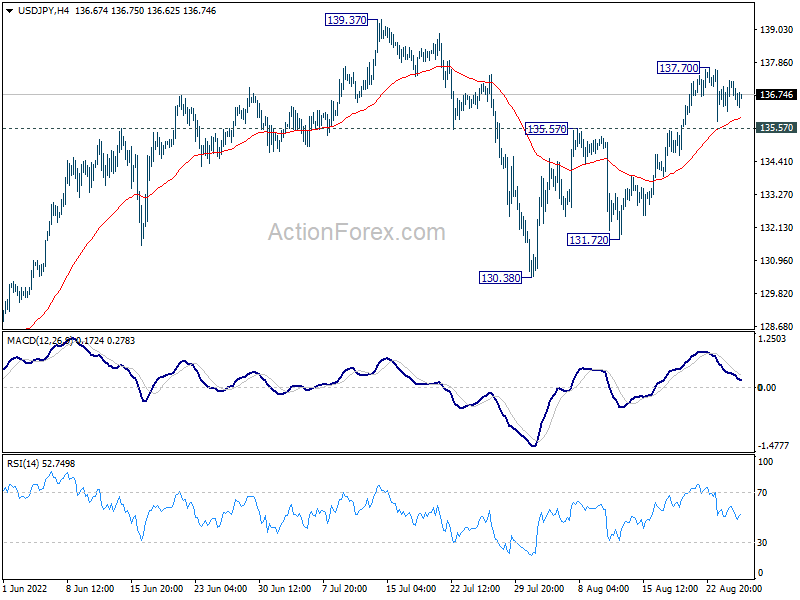

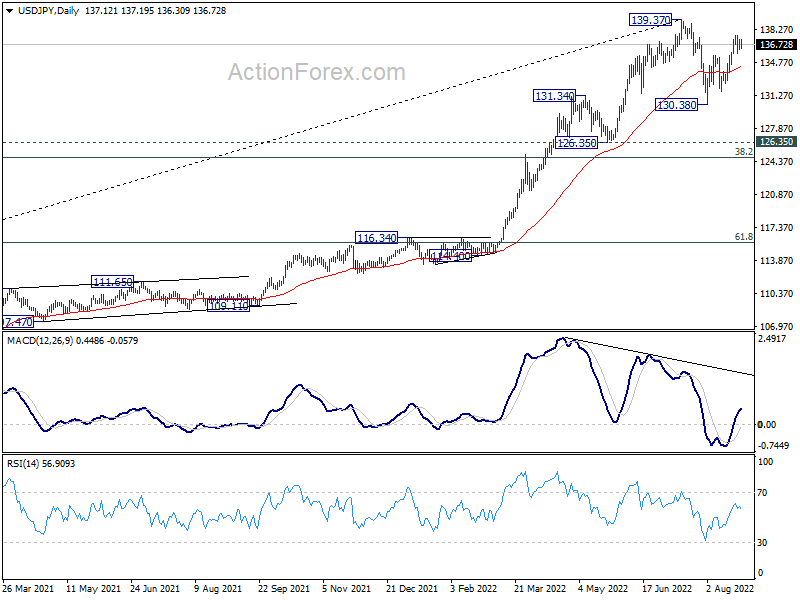

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 136.46; (P) 136.86; (R1) 137.53; More…

USD/JPY is staying in consolidation from 137.70 and intraday bias stays neutral. Overall, price actions from 139.37 are seen as a corrective pattern, with rise from 130.38 has the second leg. Above 137.70 will extend the rebound but upside should be limited by 139.37. On the downside, firm break of 135.57 will suggest that the third leg of the pattern has started, and turn intraday bias back to the downside for 131.72 support first.

{kind=link}

In the bigger picture, price actions from 139.37 medium term top are seen as a corrective pattern to up trend from 101.18 (2020 low). While deeper decline cannot be ruled out, outlook will stays bullish as long as 55 week EMA (now at 123.21) holds. Long term up trend is expected to resume through 139.37 at a later stage, after the correction finishes.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | -2.30% | 1.70% | -0.50% | |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -1.60% | 1.80% | 0.00% | -0.30% |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 2.10% | 2.20% | 2.00% | |

| 06:00 | EUR | Germany GDP Q/Q Q2 F | 0.10% | 0.00% | 0.00% | |

| 08:00 | EUR | Germany IFO Business Climate Aug | 88.5 | 86.7 | 88.6 | 88.7 |

| 08:00 | EUR | Germany IFO Current Assessment Aug | 97.5 | 96 | 97.7 | |

| 08:00 | EUR | Germany IFO Expectations Aug | 80.3 | 78.6 | 80.3 | 80.4 |

| 11:30 | EUR | ECB Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Aug 19) | 243K | 256K | 250K | 245K |

| 12:30 | USD | GDP Annualized Q2 P | -0.60% | -0.70% | -0.90% | |

| 12:30 | USD | GDP Price Index Q2 P | 9.00% | 8.70% | 8.70% | |

| 14:30 | USD | Natural Gas Storage | 54B | 18B |