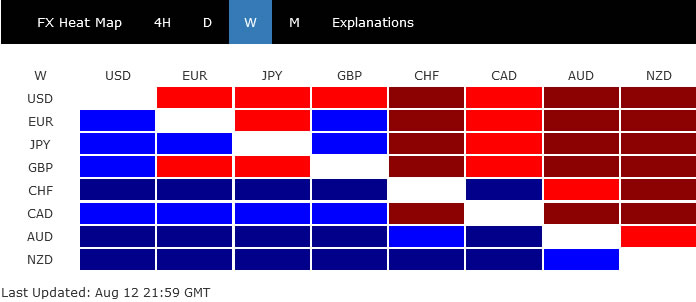

Expectations on the size of next Fed rate hike shifted again last week, with stocks cheering lower than expected consumer inflation reading in the US. Dollar ended as the worst performer but it did have a late come back following rebound in benchmark treasury yields. Indeed, it was the late selloff in Sterling and Euro, the second and third last, that worth more attention.

Meanwhile, return of risk-on sentiment lifted commodity currencies with New Zealand and Australian Dollars being the best performer. Swiss Franc was the third with help from buying against other European majors.

Looking ahead, countering forces could keep Dollar going nowhere in general. The downside breakout in Sterling and Euro in crosses could take a front seat for the near term at least.

{kind=link}

Stocks firm, yield resilient, Dollar going nowhere

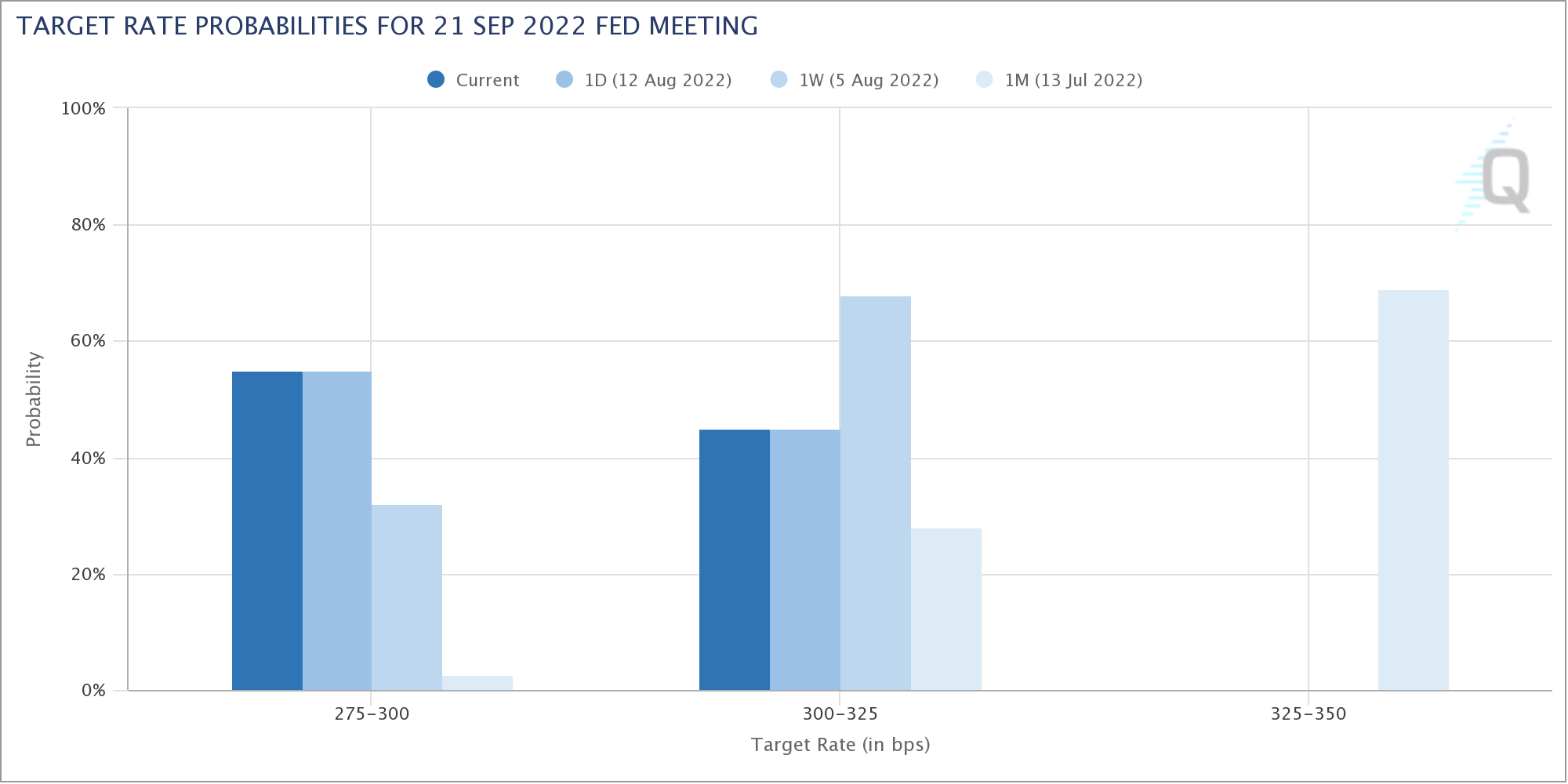

Investors pared back bet on a 75bps rate hike by Fed in September, after lower than expected CPI reading last week, which indicated that inflation might have finally peaked. Fed fund futures are pricing in only 45% chance of 75bps hike, down from 68% a week ago. Instead, there is 55% chance of just a 50bps hike, up from 32% a week ago.

Nevertheless, it should be noted that before September FOMC meeting, there will be one more set of non-farm payroll and CPI data. Thus, it’s still too early to conclude anything for that meeting. Sentiment could still flip-flop once more.

{kind=link}

The development gave risk sentiment a lift as major US stock indexes ended the week notably higher. S&P 500’s close above 55 week EMA was a bullish sign. That added to the case that correction from 4818.62 has completed completed with three waves down to 3636.87 already. Further rally is now expected as long as 4112.09 support holds. Next target is 61.8% retracement of 4818.62 to 3636.87 at 4367.19. Sustained break there should pave the way to 4637.30/4818.62 resistance zone later in the year. Such development would cap Dollar’s rally attempt, in particular against commodity currencies.

{kind=link}

{kind=link}

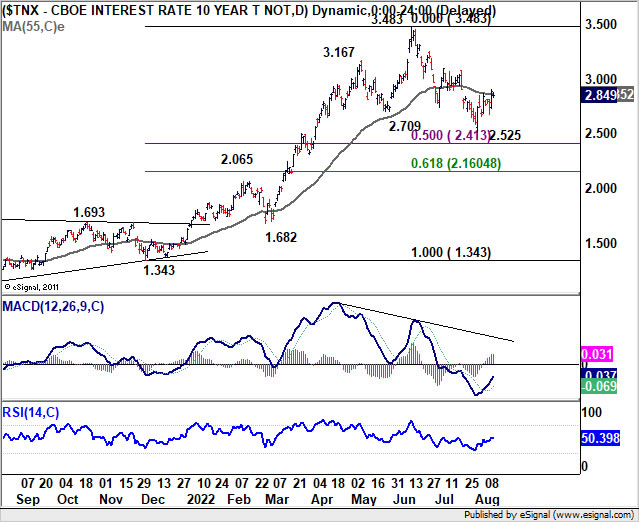

While US 10-year yield dipped initially last week, it managed to rebound quickly to close the week slightly higher at 2.849. There is no change in the view that the first leg of the consolidation pattern from 3.483 has completed at 2.525. TNX is now in the second leg of the consolidation. Sustained trading above 55 day EMA (now at 2.860), will pave the way back to 3.000 handle and above. Such development will give Dollar some support in case, and keep Yen’s rebound capped.

{kind=link}

Dollar index extended the correction from 109.29 to 104.63, but quickly recovered. DXY is still holding on to 55 day EMA (now at 105.28) and medium term channel support. Outlook isn’t bearish for now, as DXY is still seen as engaging in a near term correction pattern. This is inline with the above views that risk-on sentiment will cap Dollar’s rally while resilience in yield will limit downside. That is, Dollar is going nowhere overall.

However, sustained trading below 55 day EMA would mean that DXY is in a medium term corrective pattern that would extend to 101.29 cluster support (38.2% retracement of 89.20 to 109.29 at 101.61).

{kind=link}

Downside breakout in some Euro and Sterling crosses

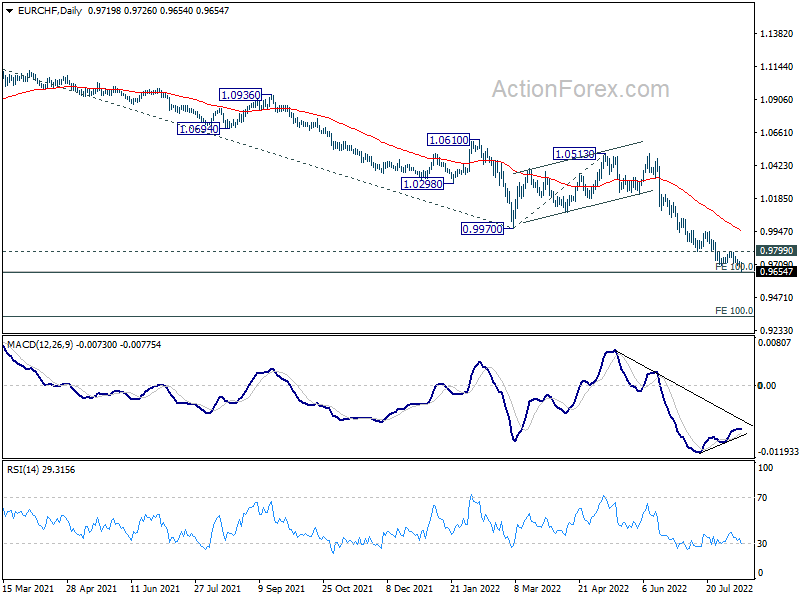

The selloffs in Euro and Sterling were more apparent, in particular against Swiss Franc and Aussie. EUR/CHF’s down trend resumed last week and hit as low as 0.9654. It doesn’t look like long term projection level 0.9650 will provide enough support for a rebound. And, in any case, outlook will stay bearish as long as 0.9799 resistance holds. Sustained break of 0.9650 will target 100% projection of 1.1149 to 0.9970 from 1.0513 at 0.9334.

{kind=link}

{kind=link}

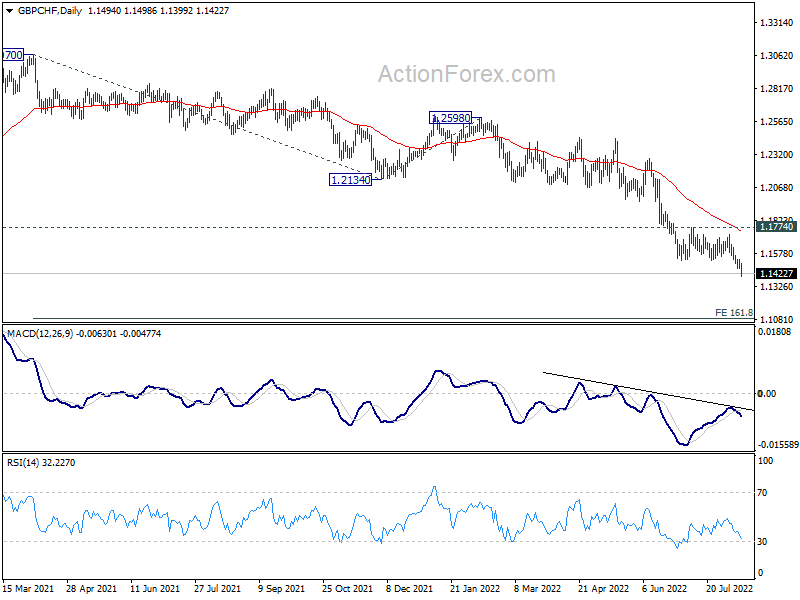

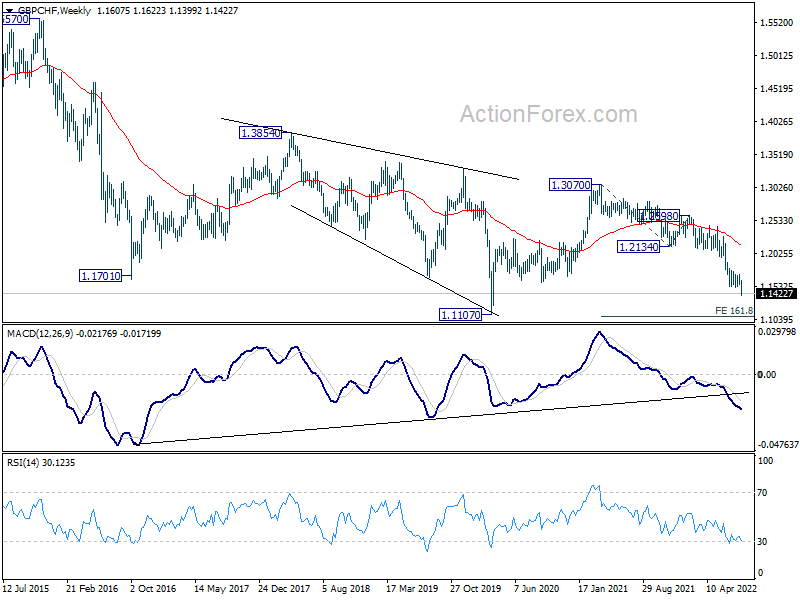

GBP/CHF has also resumed the long term down trend and hit as low as 1.1399. Outlook will stay bearish as long as 1.1774 resistance holds. Next target is 161.8% projection of 1.3070 to 1.2134 from 1.2598 at 1.1084, which is close to 1.1107 (2020 low).

{kind=link}

{kind=link}

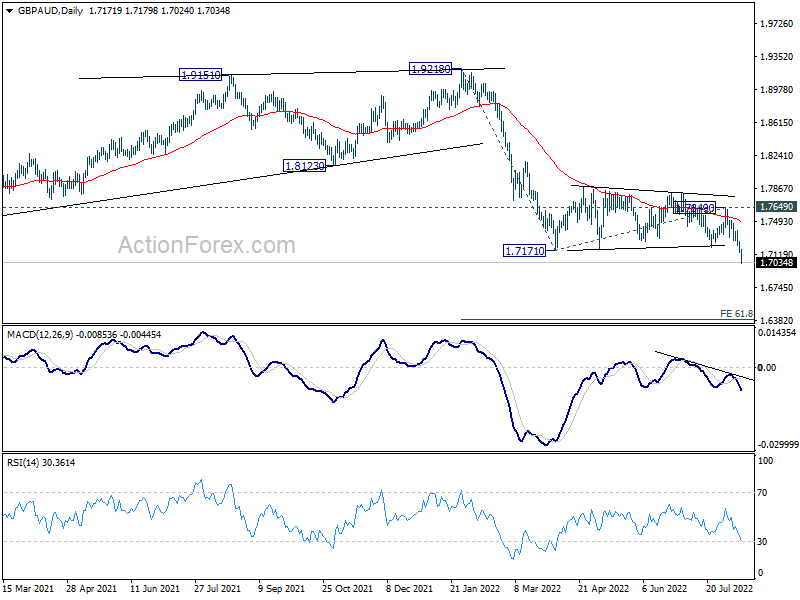

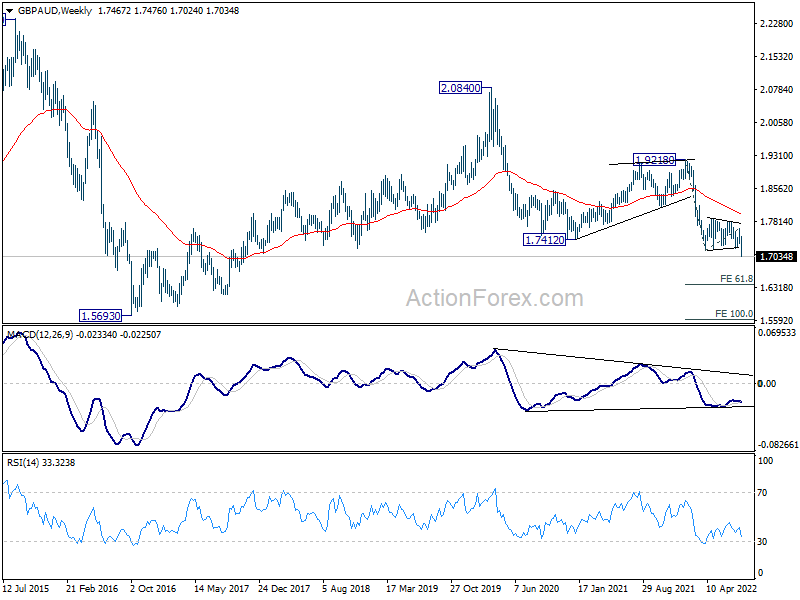

GBP/AUD broke out of near term consolidation pattern last week and hit as low as 1.7024. It’s resuming the down trend from 1.9218 (2022 high), as well as that from 2.0840 (2020 high). Near term outlook will stay bearish as long as 1.7649 resistance holds. Next target is 61.8% projection of 1.9218 to 1.7171 from 1.7649 at 1.6384.

{kind=link}

{kind=link}

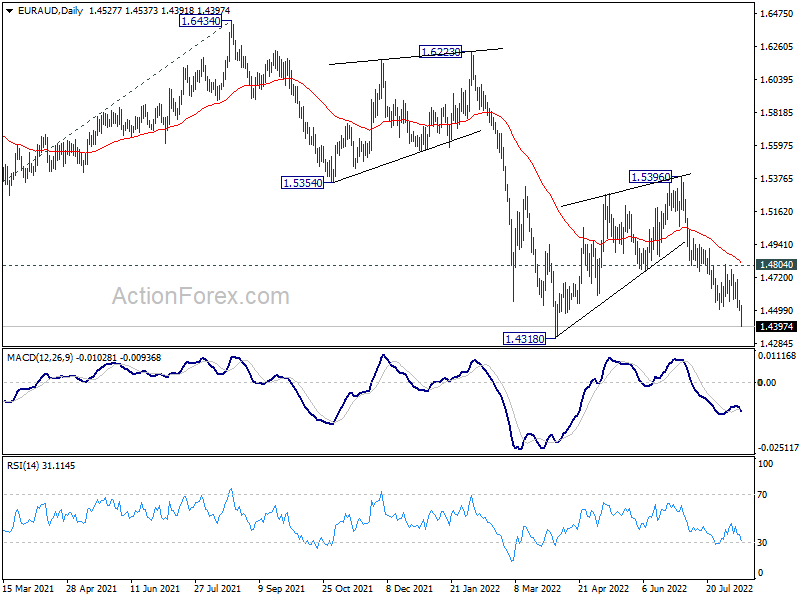

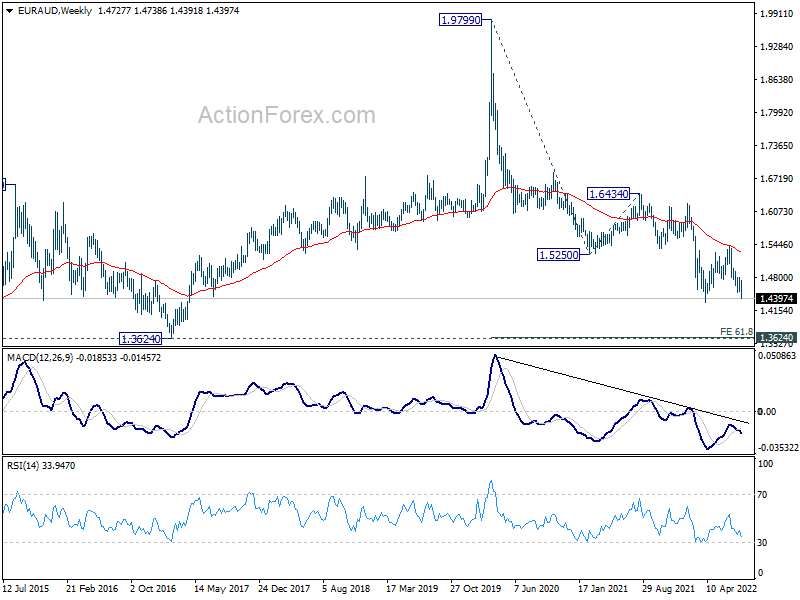

EUR/AUD also resumed the near term decline from 1.5396 and hit as low as 1.4391. It’s on track to retest 1.4318 low. Firm break there will resume the down trend from 1.6434 (2021 high), and that from 1.9799 (2020 high). Next target will be 61.8% projection of 1.9799 to 1.5250 from 1.6434 at 1.3623, which is close to 1.3624 long term support (2017 low).

{kind=link}

{kind=link}

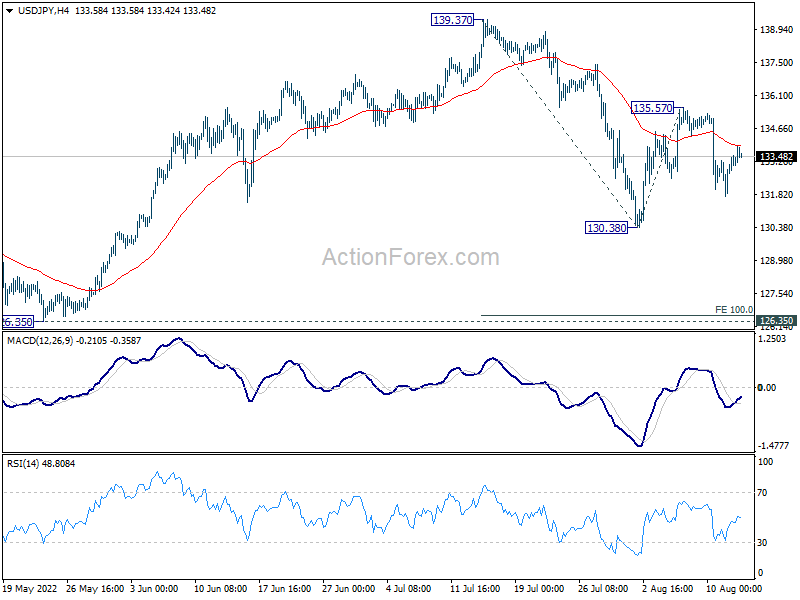

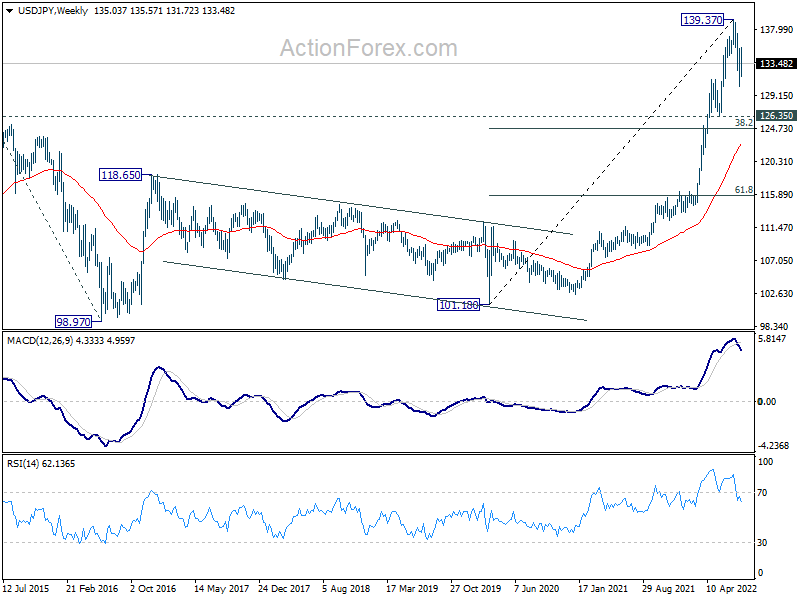

USD/JPY Weekly Outlook

USD/JPY edged higher to 135.57 last week but dropped sharply from there. Yet, downside was contained above 130.38 support. Initial bias stays neutral this week first. Outlook is unchanged that corrective pattern from 139.37 is still unfolding. Range trading between 126.35/139.37 will continue for a while. On the downside, break of 130.38 will target 100% projection of 139.37 to 130.38 from 135.57 at 126.58. On the upside, above 135.57 will resume the rebound form 130.38 to retest 139.37.

{kind=link}

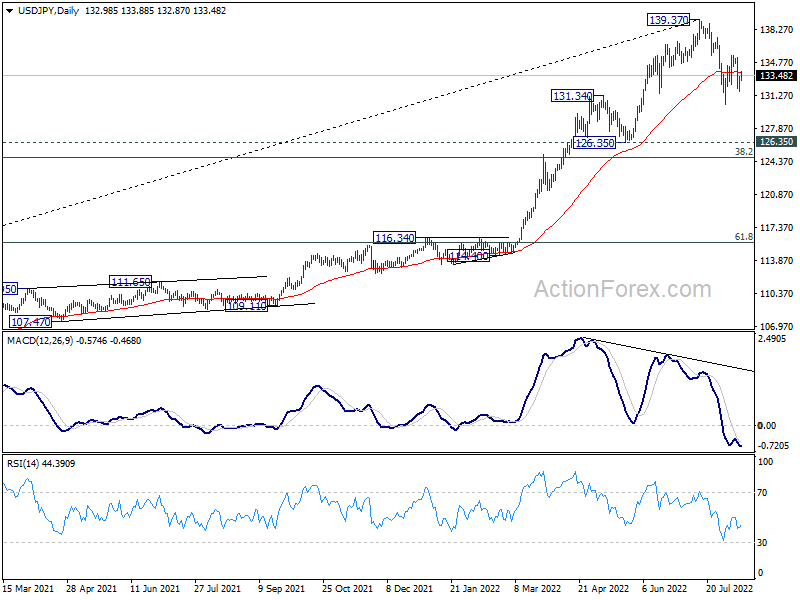

In the bigger picture, fall from 139.37 medium term top is seen as correcting whole up trend from 101.18 (2020 low). While deeper decline cannot be ruled out, outlook will stays bullish as long as 55 week EMA (now at 122.70) holds. Long term up trend is expected to resume through 139.37 at a later stage, after the correction finishes.

{kind=link}

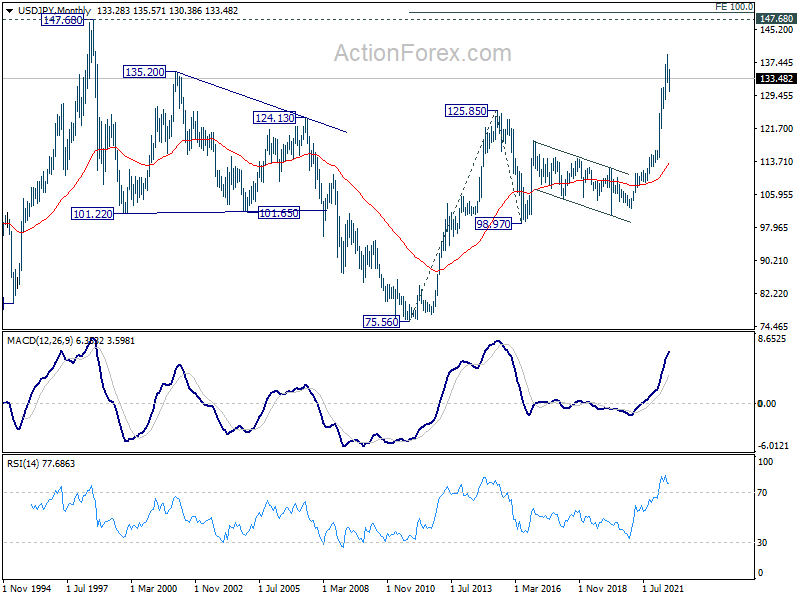

In the long term picture, rise from 101.18 is seen as part of the up trend from 75.56 (2011 low). Further rally is expected to 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 55 week EMA (now at 122.70) holds.

{kind=link}

{kind=link}