Sterling falls broadly today after BoE hikes by 50bps but indicates that a prolonged recession will start in the UK in Q4. But the selloff in the Pound is not helping Euro and Swiss Franc much, as both are mixed. Dollar and Canadian are following Sterling as next weakest. Meanwhile, Yen is leading Aussie and Kiwi higher.

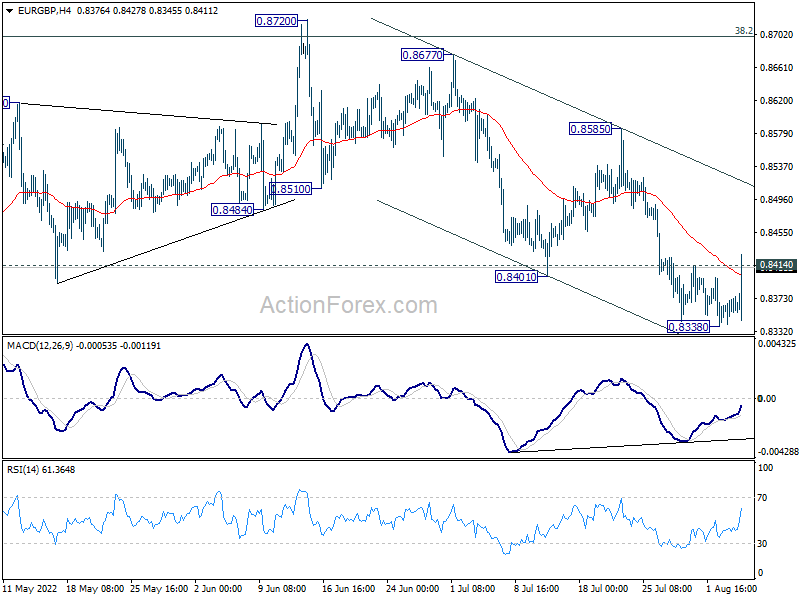

Technically, EUR/GBP’s break of 0.8414 minor resistance suggests short term bottoming at 0.8338 and stronger recovery could be seen. But to solidify Sterling’s weakness, GBP/USD will need to break through 1.2062 minor support. GBP/CHF will also need to break through 1.1525 low. Otherwise, bearishness in not confirmed.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.49%. DAX is up 1.08%. CAC is up 0.78%. Germany 10-year yield is down -0.075 at 0.803. Earlier in Asia, Nikkei rose 0.69%. Hong Kong HSI rose 2.06%. China Shanghai SSE rose 0.80%. Singapore Strait Times rose 0.55%. Japan 10-year JGB yield dropped -0.0143 to 0.175.

US initial jobless claims rose to 260k, continuing claims rose to 1416k

US initial jobless claims rose 6k to 260k in the week ending July 30, above expectation of 250k. Four-week moving average of initial claims rose 6k to 255k.

Continuing claims rose 48k to 1416k in the week ending July 23. Four-week moving average of continuing claims rose 11k to 1375k.

US exports of goods and services rose 1.7% or USD 4.3B in June to USD 260.8B. Imports dropped -0.3% or USD 1B to USD 340.4B. Trade deficit decreased by 6.2% to USD -79.6B.

BoE hikes 50bps, CPI to peak at over 13%, GDP to contract -1% in Q4

BoE raises Bank Rate by 50bps to 1.75% by 8-1 vote. Known dove Silvana Tenreyro voted for just 25bps hike. In the accompanying statement, BoE said the MPC will “take the actions necessary to return inflation to the 2% target sustainably in the medium term”. Policy is “not on a pre-set path”. But it will be “particularly alert to indications of more persistent inflationary pressures”, and will “if necessary act forcefully in response.”

In the Monetary Policy Report, CPI is projected to peak at “just over 13%” in Q4, due to Russia restricting the supply of gas to Europe and the risk of further curbs. It’s projected to fall to 5.5% by the end of 2023, and back at 2% in Q3 2024.

GDP growth is expected to slow further from Q2’s 0.5% to 0.2% in Q3, and then decline by nearly -1% in Q4. GDP is also forecast to all further, by -1.50% in 2023, and then -0.25% in 2024.

BoE Bailey: Faster tightening will help, but policy not on predetermined path

In the post meeting press conference, BoE Governor Andrew Bailey said, “overall a faster pace of policy tightening at this meeting will help to bring inflation back to the 2% target sustainably in the medium term,” he said.

“Looking ahead, that does not mean we’re now moving to a predetermined path of raising bank rate by 50 basis points per meeting, or indeed any other number for that matter.”

“Policy is not on a preset path. And what we do this time does not tell you what we’re going to do next time. All options are on the table for our September meeting, and beyond that.”

UK PMI construction dropped to 48.9, first contraction since since start of 2021

UK PMI Construction dropped from 52.6 to 48.9 in July, below expectation of 52.1. That’s the first contraction reading since January 2021, and worst since May 2020.

Tim Moore, Economics Director at S&P Global Market Intelligence, said:

“July data illustrated that cost of living pressures, higher interest rates and increasing recession risks for the UK economy are taking a toll on construction activity. Total industry output fell for the first time since the start of 2021 as civil engineering joined house building in contraction territory…. Expectations for output growth in the next 12 months are far less exuberant than those seen over the past two years, amid concerns that elevated inflation and higher borrowing costs will constrain demand.”

ECB consumer survey: Inflation expectations up, growth expectations down

In ECB’s Consumer Expectations Survey, consumers’ mean perceived inflation over the past 12 months increased markedly from May’s 8.2% to June’s 8.6%. Median inflation perceptions over the previous 12 months rose from 6.6% to 7.2%.

Mean inflation expectations for 12 month ahead rose from 6.3% to 6.6%. Median inflation expectations for 12 months ahead rose from 4.9% to 5.0%.

Mean economic growth expectations for the next 12 months dropped from -1.0% to -1.3%. Median economic growth expectations was unchanged at 0%.

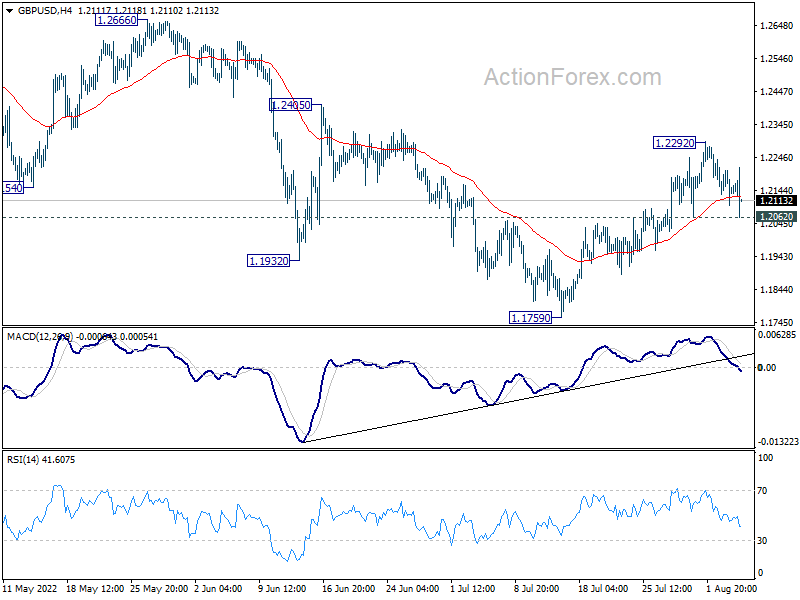

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2096; (P) 1.2152; (R1) 1.2203; More…

GBP/USD is still staying above 1.2062 minor support despite today’s dip. Intraday bias stays neutral first. On the downside, firm break of 1.2062 minor support will argue that the rebound from 1.1759 is over, and turn bias back to the downside for retesting 1.1759 low. On the upside, above 1.2292 will resume the rebound to 1.2405 resistance.

{kind=link}

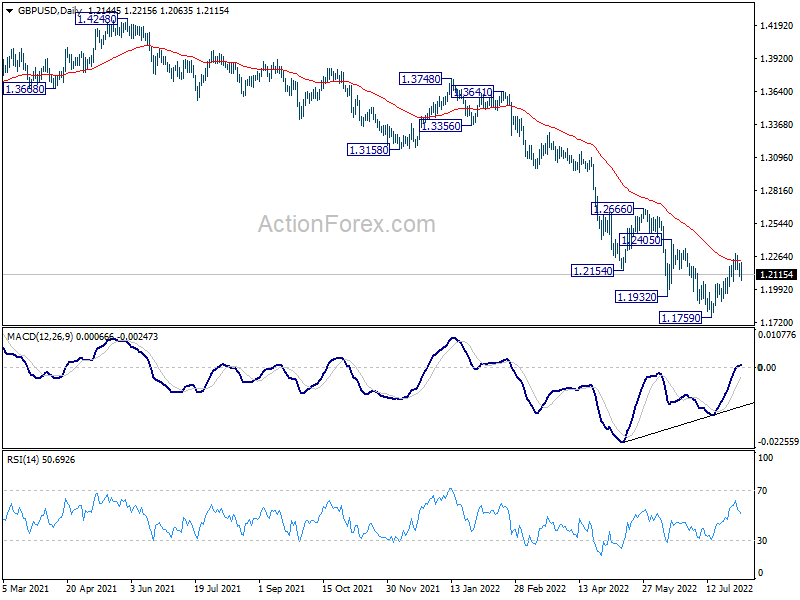

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2666 resistance holds. Next target is 1.1409 low. However, firm break of 1.2666 will bring stronger rise back to 55 week EMA (now at 1.2957).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jun | 17.67B | 14.00B | 15.97B | 15.02B |

| 06:00 | EUR | Germany Factory Orders M/M Jun | -0.40% | -0.70% | 0.10% | -0.20% |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Construction PMI Jul | 48.9 | 52.1 | 52.6 | |

| 11:00 | GBP | BoE Interest Rate Decision | 1.75% | 1.75% | 1.25% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 9–0–0 | 9–0–0 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | 36.30% | 58.80% | ||

| 12:30 | CAD | Building Permits M/M Jun | -1.50% | -2.00% | 2.30% | |

| 12:30 | CAD | International Merchandise Trade (CAD) Jun | 5.05B | 5.0B | 5.3B | |

| 12:30 | USD | Initial Jobless Claims (Jul 29) | 260K | 250K | 256K | 254K |

| 12:30 | USD | Goods and Services Trade Balance (USD) Jun | -79.6B | -81.5B | -85.5B | -84.9B |

| 14:30 | USD | Natural Gas Storage | 25B | 15B |