Dollar recovers mildly in quiet Asian session today, but it’s bounded inside Friday’s range except versus Canadian. The greenback will most probably wait until Fed Chair Jerome Powell’s comment, after another 75bps this week, before taking another firm move. As for today, Euro is so far the firmer ones, follow by Yen. New Zealand Dollar is leading commodity currencies lower. Sterling and Swiss Franc are mixed.

Technically, Dollar’s selloff lost some momentum towards the end of the week. But for now, further decline will remain in favor. Levels to watch include 1.0118 minor support in EUR/USD, 0.9738 minor resistance in USD/CHF, 0.6858 minor support in AUD/USD and 1.2988 minor resistance in USD/CAD. As long as these levels hold, near term risks stay on the downside for the greenback.

In Asia, at the time of writing, Nikkei is down -0.76%. Hong Kong HSI is down -0.75%. China Shanghai SSE is down -0.71%. Singapore Strait Times is up 0.32%. Japan 10-year JGB yield is down -0.0230 at 0.191, back below 0.2% handle.

ECB Lagarde will keep raising rates for as long as necessary

In a blog post, ECB President Christine Lagarde said that last week 50bps rate hike, the first rate increase in 11 years, was “only the latest step in our journey to unwind the special measures we had to take to fight a series of crises”, following the end of the net asset purchase programs.

“With these actions, we are sending a clear message to companies, workers and investors: inflation will return to our 2% target over the medium term,” she added. “We will keep raising rates for as long as necessary to bring inflation down to our target over the medium term.”

While Europe is facing great uncertainty, “not least over the war and energy prices… the Governing Council will review the situation and decide on the right pace for our next steps depending on the incoming data.”

ECB Holzmann: We’ll need in autumn to decide to do another 0.5% or less

ECB Governing Council member Robert Holzmann told Austrian broadcaster ORG on Sunday, “the economy will grow less strongly, the forecasts point in this direction, that has made us somewhat cautious.”

“We will see in the autumn what the economic situation is. Then we can probably decide if we do another 0.5% (rate hike) or less,” he added.

He also noted that ECB might have to accept a moderate recession to curb inflation. “We hope that won’t become necessary,” he said.

WTI heading back to 90 as rebound lost momentum

WTI crude oil turns weaker today as the recovery from 90.97 lost momentum ahead of 106.19 resistance. The selloff came on the back on gloomy economic outlook, as indicated by the poor PMI data from Eurozone and US released last week. There’s growing expectation that a global recession is inevitable as central banks move to tighten monetary policy to curb inflation.

Development in WTI suggests that fall from 124.12 is still in progress and further decline would be seen to 90.97 support and below. Current decline from 134.12 is seen as the third leg of the corrective pattern from 131.82. Deeper fall could be seen to 85.92 resistance turn support (100% projection of 131.82 to 93.47 from 124.12 at 85.77). Stronger support should be seen there to finally complete the pattern to bring sustainable rebound. This will remain the favored case as long as 106.19 resistance holds.

{kind=link}

{kind=link}

Fed to hike 75bps; GDP from US, Eurozone and Canada

FOMC rate decision in a major focus this week and Fed is widely expected to hike by 75bps. Given recent poor PMI and consumer sentiment data, it’s likely for Fed to deliver a larger hike. The question is indeed on whether Chair Jerome Powell would signal a slowdown in tightening after this move, and his view on recession risks. On central bank front, BoJ will release meeting minutes and summary of opinions.

Also, attention will be on GDP data from US, Eurozone and Canada. CPI from Australia and Eurozone will also be watched, as well as US PCE inflation. Some focuses will also be on Germany Ifo business climate and Gfk consumer sentiment; US consumer confidence and durable goods orders. Here are some highlights for the week:

- Monday: Germany Ifo business climate.

- Tuesday: BoJ minutes, corporate services prices; US house price index, consumer confidence, new homes sales.

- Wednesday: Australia CPI; Germany Gfk consumer climate; Swiss Credit Suisse economic expectations; Eurozone M3; US durable goods orders, goods trade balance, pending home sales, FOMC rate decision.

- Thursday: New Zealand ANZ business confidence; Australia import prices, retail sales; Germany CPI flash; US Q2 advance GDP, jobless claims.

- Friday: BoJ summary of opinions, Japan Tokyo CPI, unemployment rate, retail sales, consumer confidence, housing starts; Australia PPI, private sector credit; France consumer spending, GDP; Germany GDP, import prices, unemployment; Swiss retail sales, KOF economic barometer; Italy GDP; UK mortgage approvals, M4 money supply; Eurozone GDP; Canada GDP; US personal income and spending, and PCE inflation, Chicago PMI.

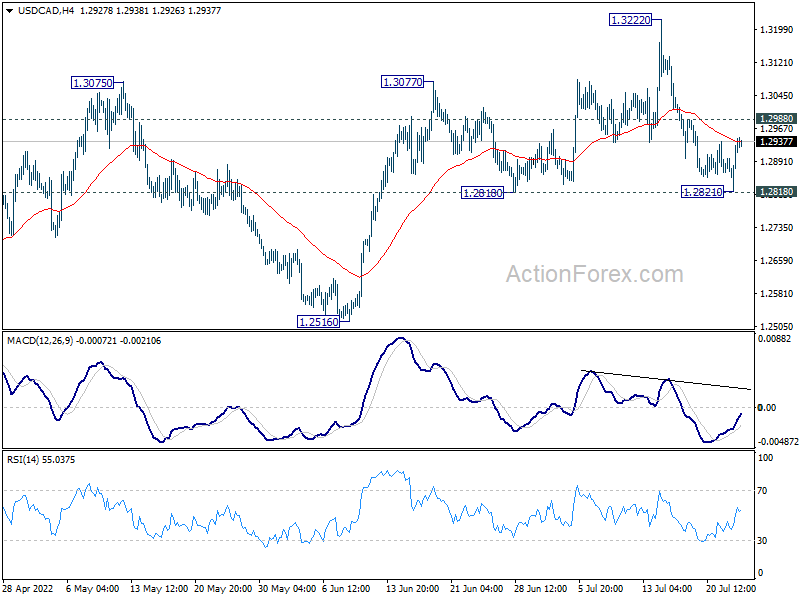

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2849; (P) 1.2889; (R1) 1.2954; More…

Intraday bias in USD/CAD stays neutral at this point. On the downside, break of 1.2818 support will bring deeper fall back to 1.2516 key support. On the upside, above 1.2988 minor resistance will reinforce near term bullishness, and turn bias back to the upside for retesting 1.3222 instead.

{kind=link}

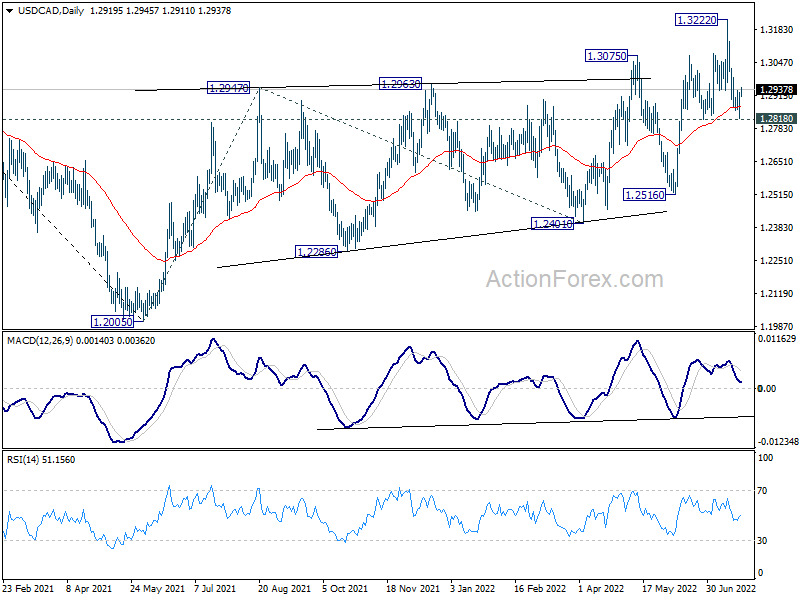

In the bigger picture, down trend from 1.4667 (2020 high) should have completed at 1.2005, after defending 1.2061 long term cluster support. Rise from there should target 61.8% retracement of 1.4667 to 1.2005 (2021 low) at 1.3650. This will remain the favored case now as long as 1.2516 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Jul | 90.5 | 92.3 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jul | 98.2 | 99.3 | ||

| 08:00 | EUR | Germany IFO Expectations Jul | 83 | 85.8 |