The lift from ECB rate hike to Euro was rather brief yesterday. The common currency remains range bound again most currencies and turns slightly softer today. Dollar, on the other hand, is regaining some ground with Canadian and Swiss Franc. Overall, the greenback is still the weakest one for the week, followed by Yen. Aussie is the strongest, followed by Canadian. There is prospect of reinforcing the positions if global stock markets can surge before weekly close, after all major even risks are past.

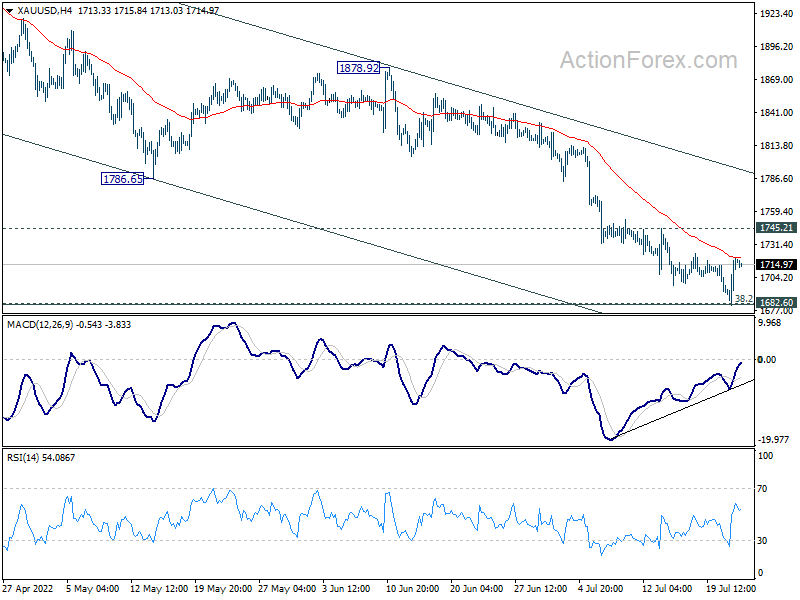

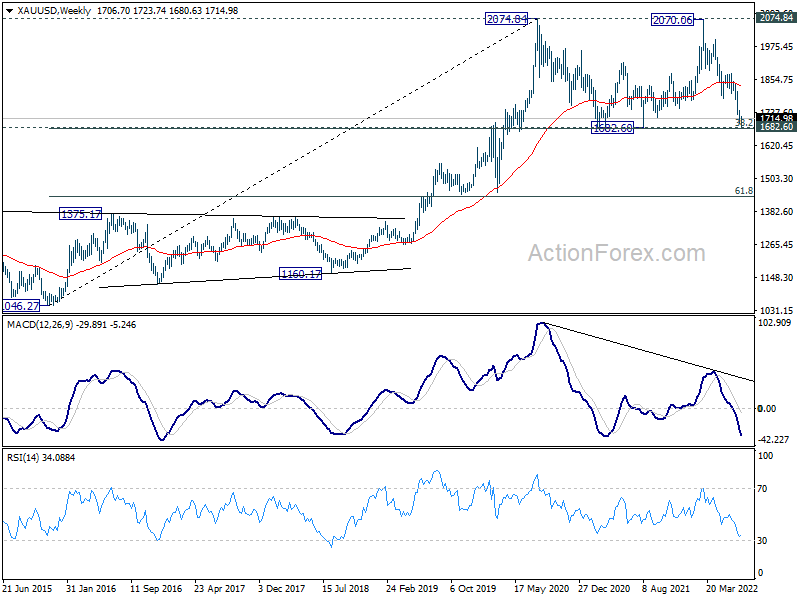

Technically, one focus is on Gold, which dipped to as low as 1680.63 yesterday, but rebounded quickly from there. It’s now back above 1700 handle. We’d maintain the view that 1682.60 long term level should provide strong support to complete the fall from 2070.06. Break of 1745.21 resistance will be the first sign of bullish reversal. Let’s see if that will happen within the next few days.

{kind=link}

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.50%. Hong Kong HSI is down -0.22%. China Shanghai SSE is down -0.54%. Singapore Strait Times is up 0.82%. Japan 10-year JGB yield is down -0.0170 at 0.224. Overnight, DOW rose 0.51%. S&P 500 rose 0.99%. NASDAQ rose 1.36%. 10-year yield dropped -0.126 to 2.910.

Japan CPI core ticked up to 2.2% yoy, core-core up to 1.0% yoy

Japan all-item CPI dropped from 2.5% yoy to 2.4% yoy in June. CPI core (all-items ex-fresh food), rose from 2.1% yoy to 2.2% yoy, matched expectations. CPI core-core (all-items ex-fresh food, energy) rose from 0.8% yoy to 1.0% yoy.

The CPI core reading has now stayed above BoJ’s 2% target for a third consecutive month. The core-core reading was also the strongest since February 2016.

BoJ left monetary policy unchanged yesterday. According to the new economic forecasts, core CPI will hit 2.3% this year, but then slowed back to 1.4% in fiscal 2023, and then 1.3% in fiscal 2024.

Japan PMI manufacturing dropped to 52.2 in July, services down to 51.2

Japan PMI Manufacturing dropped from 52.7 to 52.2 in July, below expectation of 53.1. PMI Services dropped from 54.0 to 51.2. PMI Composite output dropped from 53.0 to 50.6.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: “Flash PMI data indicated that activity at Japanese private sector businesses rose at a softer rate during July. The expansion in output was the softest recorded since March and only marginal as companies noted that shortages of raw materials and rising energy and wage costs had increasingly dampened output and new order inflows. This was notably evident at manufacturers, who recorded a reduction in production levels for the first time in five months. Service providers meanwhile reported the slowest rise in activity since April”.

Australia PMI composite dropped to 6-mnth low, further deceleration in growth

Australia PMI Manufacturing dropped from 56.2 to 55.7 in July. PMI Services dropped from 52.6 to 50.4, a 6-month low. PMI Composite dropped from 52.6 to 50.6, also a 6-month low.

Laura Denman, Economist at S&P Global Market Intelligence said: “Latest survey data has pointed to a further deceleration in the rate of private sector growth. Panellists suggested that interest rate increases, alongside persistent inflationary pressures, have been a pivotal factor contributing to the weakened private sector improvement this month. Further interest rate increases by Australia’s central bank present a downside risk to the private sector, with sentiment slipping to a 27-month low.”

Looking ahead

PMI data from Eurozone and UK will be the main focus in European session. UK retail sales will also be released. Later in the data, Canada retail sales and US PMIs will be published.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0135; (P) 1.0204; (R1) 1.0252; More…

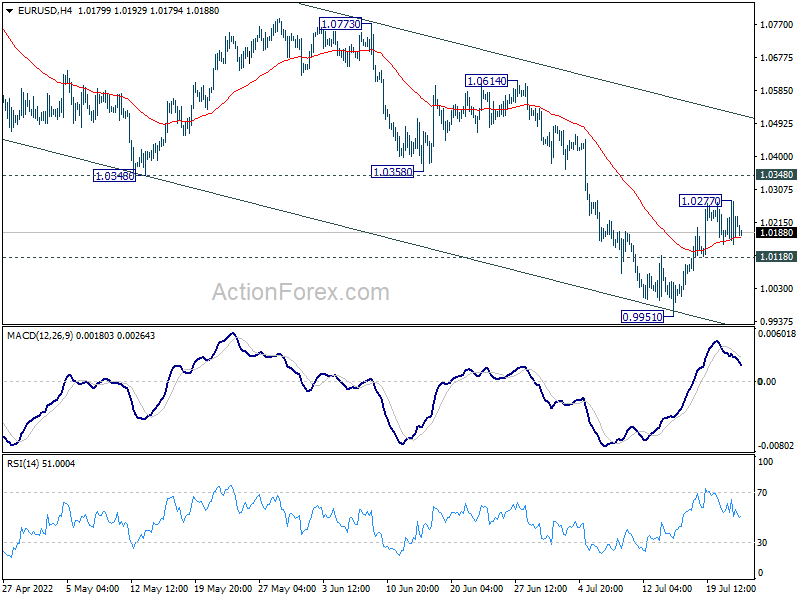

EUR/USD quickly retreated after edging 1.0277 and intraday bias is turned neutral again. On the upside, above 1.0277 will resume the rebound from 0.9951 to 1.0348 support turned resistance, and then channel resistance at 1.0514. Nevertheless, break of 1.0118 minor support will argue that larger down trend is ready to resume, and should bring retest of 0.9951 low first.

{kind=link}

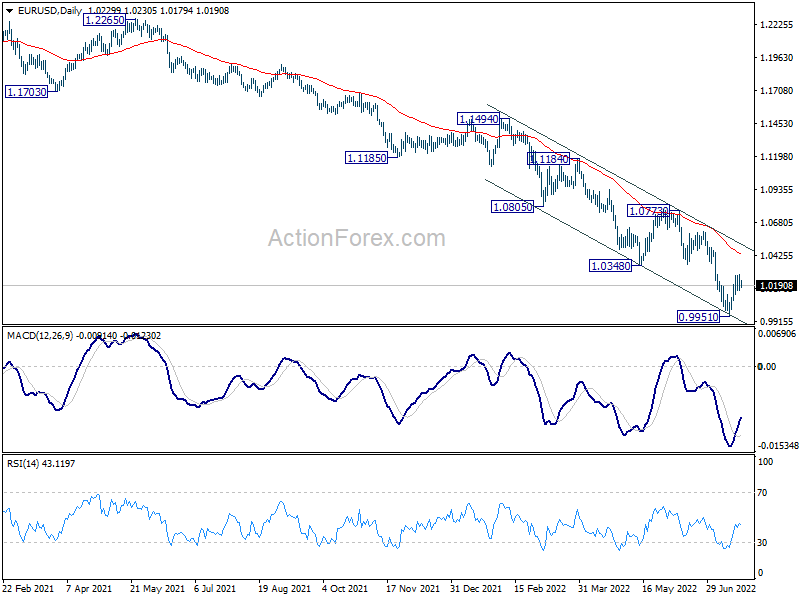

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0773 resistance holds, in case of rebound.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jul P | 55.7 | 56.2 | ||

| 23:00 | AUD | Services PMI Jul P | 50.4 | 52.6 | ||

| 23:01 | GBP | GfK Consumer Confidence Jul | -41 | -42 | -41 | |

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.20% | 2.20% | 2.10% | |

| 00:30 | JPY | Manufacturing PMI Jul P | 52.2 | 53.1 | 52.7 | |

| 06:00 | GBP | Retail Sales M/M Jun | -0.30% | -0.50% | ||

| 06:00 | GBP | Retail Sales Y/Y Jun | -5.30% | -4.70% | ||

| 06:00 | GBP | Retail Sales ex-Fuel M/M Jun | -0.30% | -0.70% | ||

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Jun | -6.20% | -5.70% | ||

| 07:15 | EUR | France Manufacturing PMI Jul P | 50.6 | 51.4 | ||

| 07:15 | EUR | France Services PMI Jul P | 52.7 | 53.9 | ||

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 50.6 | 52 | ||

| 07:30 | EUR | Germany Services PMI Jul P | 51.3 | 52.4 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 51 | 52.1 | ||

| 08:00 | EUR | Eurozone Services PMI Jul P | 52 | 53 | ||

| 08:30 | GBP | Manufacturing PMI Jul P | 52 | 52.8 | ||

| 08:30 | GBP | Services PMI Jul P | 53.2 | 54.3 | ||

| 12:30 | CAD | Retail Sales M/M May | 1.60% | 0.90% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M May | 1.80% | 1.30% | ||

| 13:45 | USD | Manufacturing PMI Jul P | 52.5 | 52.7 | ||

| 13:45 | USD | Services PMI Jul P | 52.1 | 52.7 |