Dollar, Yen and Swiss Franc are both under some selling pressure today, as overall risk sentiment improved. Sterling is currently the winner and Euro is not too far behind. Canadian Dollar leads commodity currencies, as Kiwi is somewhat lagging despite strong inflation data. The picture will depend on whether stock markets in the US could extend Friday’s strong rebound, in sustainable way.

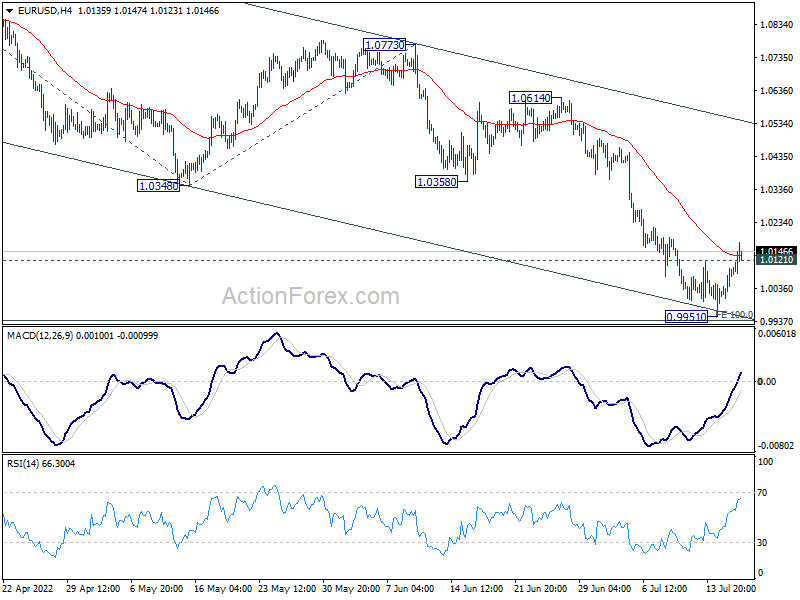

Technically, EUR/USD’s break of 1.0121 minor resistance suggests that a short term bottoming is formed at 0.9951, after defending parity. Further rebound is in favor towards 1.0348 support turned resistance. Such development could also help GBP/USD through 1.2055 minor resistance and AUD/USD through 0.6873 minor resistance to confirm short term bottoming. Let’s see.

In Europe, at the time of writing, FTSE is up 0.99%. DAX is up 0.82%. CAC is up 1.05%. Germany 10-year yield is up 0.0885 at 1.221. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 2.70%. China Shanghai SSE rose 1.55%. Singapore Strait Times rose 0.73%.

BoE Saunders: Tightening cycle may still have some way to go

BoE MPC member Michael Saunders said in a speech, “my own view is that further monetary tightening is likely, and indeed, as evident from my votes at the MPC’s recent policy meetings, my preference has been to tighten relatively quickly.”

“This partly reflects my view that risks are tilted on the side of a more persistent period of excess demand and domestic inflation pressures than implied by the most recent MPR forecast (published in early May),” he said.

“Unless restrained by tighter monetary policy, the relatively high level of longer-term inflation expectations implies that domestic cost growth and firms’ pricing strategies may remain above target-consistent rates even if capacity pressures ease to more normal levels.”

Also, the cost of “not tightening promptly enough – would be relatively high at present”, and “such an outcome would increase the costs of returning inflation to target in coming years.”

“rather than focus on a precise forecast for Bank Rate over the next year, the key point is that the tightening cycle may (in my view) still have some way to go.”

New Zealand BusinessNZ services rose slightly to 55.4, sustained improvement

New Zealand BusinessNZ Performance of Services Index ticked up from 55.3 to 55.4 in June, staying above long term average of 53.6 or the survey. Activity/sales dropped from 59.4 to 56.5. But employment improved notably from 49.0 to 53.1. New orders/business rose from 62.0 to 61.7. Stocks/inventories dropped from 54.7 to 54.1. Supplier deliveries rose from 45.6 to 47.8.

BNZ Senior Economist Craig Ebert said that “the move to traffic light Orange in mid-April, along with the expedited opening of the border, is clearly providing a basis for sustained improvement in New Zealand’s services sector”.

New Zealand CPI jumped to 32-yr high at 7.3% yoy in Q2

New Zealand CPI rose 1.7% qoq, 7.3% yoy in Q2, above expectation of 1.5% qoq, 7.1% yoy. The annual inflation accelerated from 6.9% yoy to 7.3%, a 32-year high, after 7.6% in Q2 1990.

StatsNZ said, “the main driver for the 7.3 percent annual inflation to the June 2022 quarter was the housing and household utilities group, due to rising prices for construction and rentals for housing… Transport was also a main driver of the quarterly rise, driven by petrol and diesel.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0031; (P) 1.0064; (R1) 1.0122; More…

EUR/USD’s break of 1.0121 minor resistance suggests short term bottoming at 0.9951. That comes after breaching parity and missing 100% projection of 1.1184 to 1.0348 from 1.0773 at 0.9937. Intraday bias is now mildly on the upside for 1.0348 support turned resistance. Break will target channel resistance at 1.0514. On the downside, firm break of 0.9951 will resume larger down trend to 161.8% projection at 0.9420.

{kind=link}

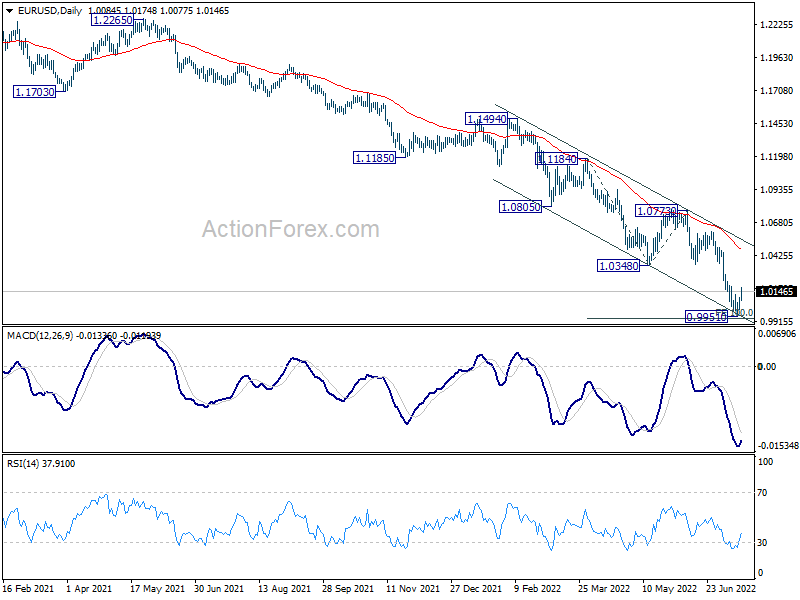

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0773 resistance holds, in case of rebound.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | 55.4 | 55.2 | 55.3 | |

| 22:45 | NZD | CPI Q/Q Q2 | 1.70% | 1.50% | 1.80% | |

| 22:45 | NZD | CPI Y/Y Q2 | 7.30% | 7.10% | 6.90% | |

| 08:00 | EUR | Italy Trade Balance (EUR) May | -0.01B | -2.32B | -3.67B | -3.64B |

| 12:15 | CAD | Housing Starts Y/Y Jun | 274K | 285K | 287K | 282K |

| 14:00 | USD | NAHB Housing Market Index Jul | 68 | 67 |