Swiss Franc remains the strongest one for the week and stays firm into US session. Dollar is also regaining some ground, as the second best. On the other than, commodity currencies are the worst performing one, as led by Canadian. In other markets, European indexes are mildly in black while US futures are nearly flat. Trading might turn quiet ahead of a long weekend in the US.

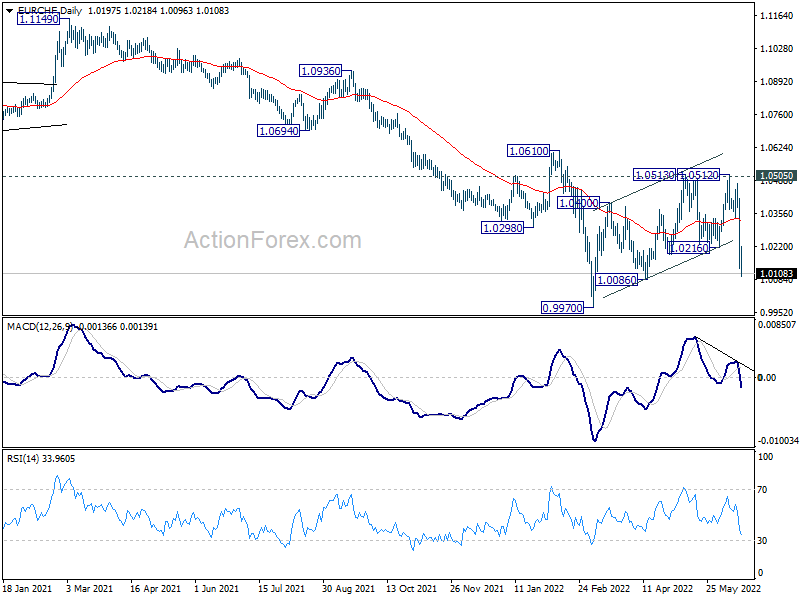

Technically, EUR/CHF is getting close to 1.0086 support. Firm break there will raise the chance of larger down trend resumption through parity and 0.9970 low. The question is, if that happens, whether it would be accompanied by more broad based decline is Euro. In particular, EUR/USD is still in favor to break through 1.0339 low at a later stage.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.51%. DAX is up 0.49%. CAC is up 0.45%. Germany 10-year yield is down -0.027 at 1.689. Earlier in Asia, Nikkei dropped -1.77%. Hong Kong HSI rose 1.10%. China Shanghai SSE rose 0.96%. Singapore Strait Times rose 0.02%. Japan 10-year JGB yield dropped -0.0377 to 0.233.

BoE Pill: There’s a conditionality for forceful policy actions

BoE Chief Economist Huw Pill told BloombergTV that in yesterday policy decision statement, “the word ‘forcefully’ – which clearly is the word the market is focused on, you focused on, and has a meaning – it’s also important to see that that was put in the context of ‘if necessary we will act forcefully’, and so there’s a conditionality there.”

“If we do see greater evidence that the current high level of inflation is becoming embedded in pricing behavior by firms, in wage setting behavior by firms and workers, then that will be the trigger for this more aggressive action,” he added.

But he also indicated that the statement had “a certain level of flexibility because it had to encompass those different views… we were trying to emphasise is that that flexibility also applies to what the decisions are. I don’t think it’s all about August. We talked about the pace, timing and scale of future decisions.”

Eurozone CPI finalized at 8.1% yoy in may, core CPI at 3.8% yoy

Eurozone CPI was finalized at 8.1% yoy in May, up from April’s 7.4% yoy. All-items excluding energy rose from 4.1% yoy to 4.6% yoy. All-item excluding energy, food, alcohol and tobacco rose from 3.5% yoy to 3.8% yoy. Energy prices accelerated from 37.5% yoy to 39.1% yoy. Food, alcohol and tobacco prices accelerated from 6.3% yoy to 7.5% yoy.

EU CPI was finalized at 8.8% yoy, up from April’s 8.1% yoy. The lowest annual rates were registered in France, Malta (both 5.8%) and Finland (7.1%). The highest annual rates were recorded in Estonia (20.1%), Lithuania (18.5%) and Latvia (16.8%). Compared with April, annual inflation fell in one Member State and rose in twenty-six.

BoJ leaves rate unchanged at -0.1%, keeps 0.25% 10-yr yield cap

BoJ left short-term policy interest rate unchanged at -0.10%, and 10-year JGB target at around 0% under the yield curve control. It will continue to defend the 0.25% 10-year JGB yield cap, by offering to purchase it at the rate on every business day through fixed-rate purchase operations.

The decision was made by 8-1 vote. Goushi Kataoka dissented again, pushing for further strengthening monetary easing by lowering short- and long-term interest rate.

The central bank also said “it is necessary to pay due attention to developments in financial and foreign exchange markets and their impact on Japan’s economic activity and prices.”

BoJ Kuroda: 10-yr JGB yields above 0.25% would diminish effect of monetary easing

BoJ Governor Haruhiko Kuroda said in the post-meeting press conference, “the recent rapid weakening of the yen is raising uncertainty over the outlook and making it hard for companies to draw up business plans so it is negative and undesirable for the economy.”

“We will have to closely watch developments in financial and currency markets and their impact on the economy and prices,” he added.

Kuroda also added, “policy tightening is not appropriate at this point.” And he warned, “if the 10-year JGB yield exceeds 0.25%, that would diminish the effect of our monetary easing.”

New Zealand BusinessNZ manufacturing rose to 52.9, excess demand abating

New Zealand BusinessNZ Performance of Manufacturing index rose from 51.2 to 52.9 in May. Production rose from 49.4 to 52.8. Employment rose from 49.8 to 53.0. New orders dropped from 55.2 to 53.0. Finished stocks dropped from 54.0 to 53.1. Deliveries rose from 49.7 to 55.4.

BNZ Senior Economist, Craig Ebert stated that “The net result of the sub-index values was the inference that excess demand alleviated during May. New orders are perhaps the cleanest representation of demand, while deliveries speak more to the supply side. To the extent excess demand is abating, so too will be core inflation pressure”.

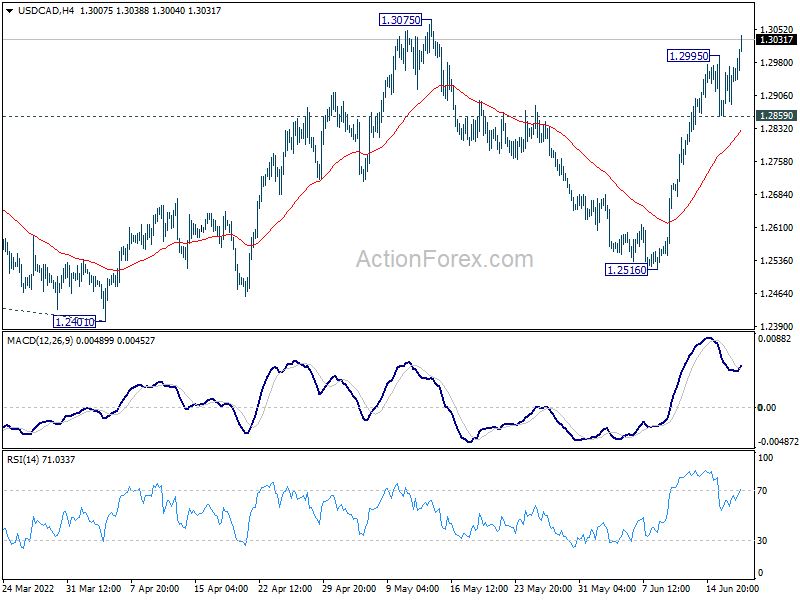

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2882; (P) 1.2927; (R1) 1.2992; More…

USD/CAD’s rally resumed after brief consolidation and intraday bias is back on the upside. Firm break of 1.3075 will resume medium term rally and sustained trading above 1.3022 fibonacci level will carry larger bullish implications. Next target is 100% projection of 1.2005 to 1.2947 from 1.2401 at 1.3343. On the downside, below 1.2859 minor support will turn bias neutral again first.

{kind=link}

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 09:00 | EUR | Italy Trade Balance (EUR) Apr | -3.67B | -2.26B | -0.08B | -0.23B |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 8.10% | 8.10% | 8.10% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 3.80% | 3.80% | 3.80% | |

| 12:30 | CAD | Industrial Product Price M/M May | 1.70% | 0.10% | 0.80% | |

| 12:30 | CAD | Raw Material Price Index May | 2.50% | 1.70% | -2.00% | |

| 13:15 | USD | Industrial Production M/M May | 0.20% | 0.40% | 1.10% | 1.40% |

| 13:15 | USD | Capacity Utilization May | 79.00% | 79.20% | 79.00% | 78.90% |