Euro is knocked down in early US session after ECB left interest rates unchanged. The central bank leaves the option to continue the asset purchases program after June, even though it will be concluded in Q3. The announcement disappoints some Euro traders who are eager for more hawkish tone. At the time of writing, Aussie is still the worst performing one for the day, followed by Swiss Franc and Euro. Kiwi is the strongest one but Yen and Dollar are also striking back.

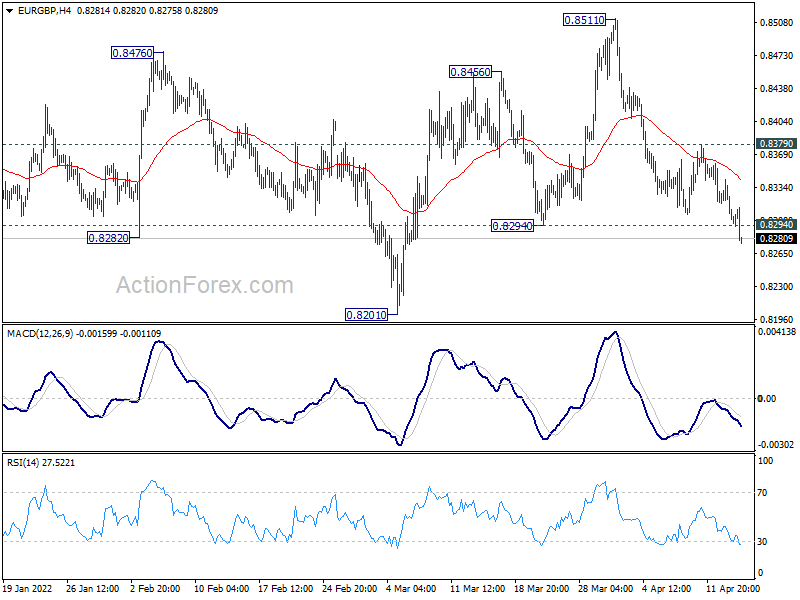

Technically, EUR/GBP’s break of 0.8294 support suggests that whole rebound from 0.8201 has completed as a three-wave correction at 0.8511. The development revives medium term bearishness and deeper decline could be seen through 0.8201 low for down trend resumption. Immediate focus will now be on whether EUR/USD would drop through 1.0808 temporary low too.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.62%. CAC is up 0.61%. Germany 10-year yield is up 0.027 at 0.793. Earlier in Asia, Nikkei rose 1.22%. Hong Kong HSI rose 0.67%. China Shanghai SSE rose 1.22%. Singapore Strait Times dropped -0.19%. Japan 10-year JGB yield rose 0.0028 to 0.243.

US retail sales rose 0.5% mom in Mar, ex-auto sales up 1.1% mom

US retail sales rose 0.5% mom to USD 665.7B in March, slightly below expectation of 0.5% mom. Ex-auto sales rose 1.1% mom, above expectation of 0.7% mom. Ex-gasoline sales dropped -0.3% mom. Ex-auto, ex-gasoline sales rose 0.2% mom.

Total sales for January through March period were up 12.9% yoy.

US initial claims rose to 185k, continuing claims dropped to 1.475m

US initial jobless claims rose 18k to 185k in the week ending April 9, above expectation of 175k. Four-week moving average of initial claims rose 2k to 172k.

Continuing claims dropped -48k to 1475k in the week ending April 2. Four-week moving average of continuing claims dropped -30k to 1512k.

ECB to conclude asset purchases in Q3, keeps rates unchanged

ECB announced that the Asset Purchase Program “should be concluded in the third quarter. Monthly net purchases under the APP will continue to be EUR 40B in April, EUR 30B in May and EUR 20B in June. The calibration of net purchases for Q3 will be data-dependent and depend on the outlook.

Interest rates are held unchanged with main refinancing rate, marginal lending facility rate and deposit rate at 0.00%, 0.25% and -0.50% respectively. Adjustments to rates will take place “some time” after ending the APP and will be “gradual”.

Australia employment rose 17.9k in Mar, unemployment rate unchanged at 4%

Australia employment grew 17.9k in March, below expectation of 30.0k. Full-time jobs rose 20.5k while part-time jobs dropped -2.7k. Unemployment rate was unchanged at 4.0%, above expectation of 3.9%. Participation rate was unchanged at 66.4%. Monthly hours worked dropped -0.6% mom.

Bjorn Jarvis, head of labour statistics at the ABS, said: “With employment increasing by 18,000 people and unemployment falling by 12,000, the unemployment rate decreased slightly in March, though remained at 4.0 per cent in rounded terms.

“4.0 per cent is the lowest the unemployment rate has been in the monthly survey. Lower rates were seen in the series before November 1974, when the survey was quarterly.”

New Zealand BNZ manufacturing rose to 53.8

New Zealand BNZ Performance of Manufacturing Index rose slightly from 53.6 to 53.8 in March. Production dropped from 51.7 to 50.9. Employment rose from 52.0 to 52.4. New orders rose from 58.6 to 61.0. Finished stocks rose from 50.2 to 53.5. Deliveries dropped from 53.1 to 51.9.

BNZ Senior Economist, Doug Steel stated that “Omicron’s impact may not be as harsh as the first 2020 COVID lockdown or last year’s Delta lockdown, but it’s there. Production has struggled, with the index slipping to 50.9 in March and a bit further below its long-term average.”

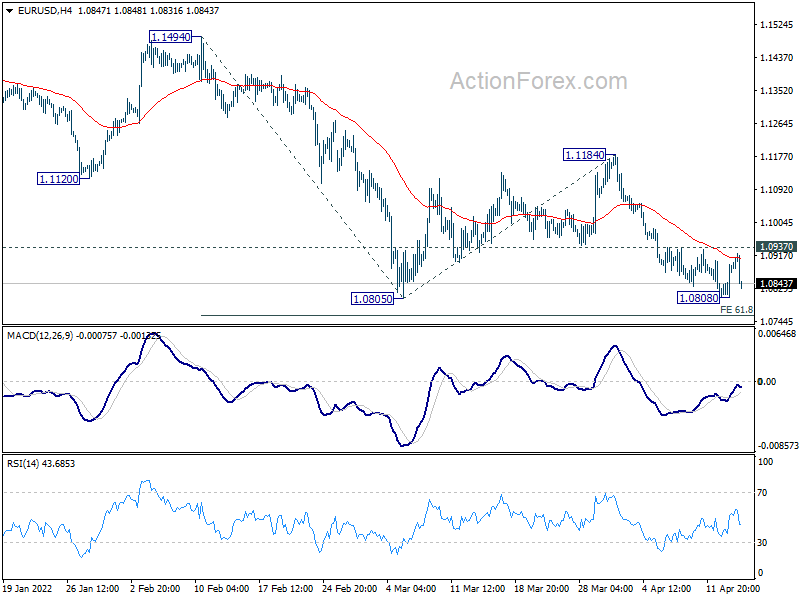

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0836; (P) 1.0865 (R1) 1.0921; More…

EUR/USD retreats sharply after failing to break through 1.0937 minor resistance. Intraday bias remains neutral first. On the downside, sustained break of 1.0805 low will resume larger down trend to 61.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0758, and then 100% projection at 1.0495. On the upside, break of 1.0937 minor resistance will extend the consolidation pattern from 1.0805 with another rising leg. Intraday bias will be back on the upside for stronger rebound. But overall outlook will stay bearish as long as 1.1184 resistance holds.

{kind=link}

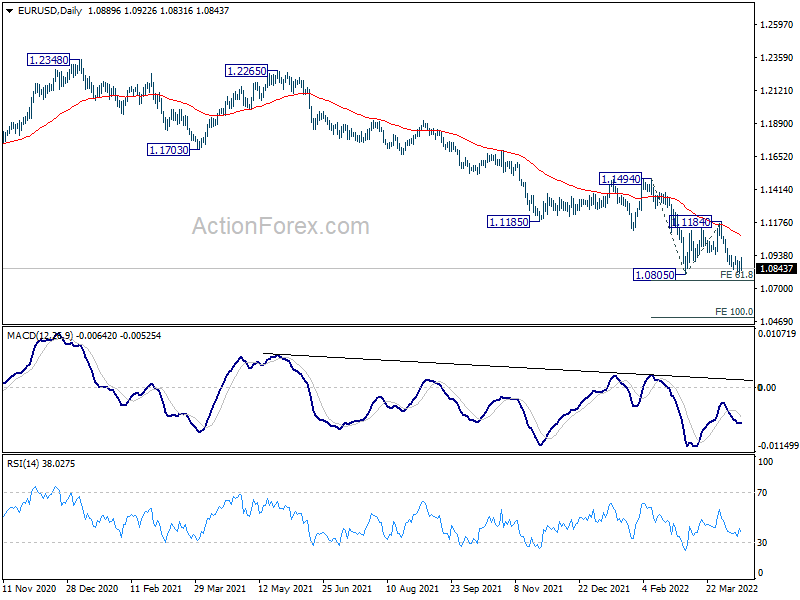

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Manufacturing Index Mar | 53.8 | 53.6 | ||

| 23:01 | GBP | RICS Housing Price Balance Mar | 74% | 78% | 79% | |

| 01:00 | AUD | Consumer Inflation Expectations Apr | 5.20% | 4.90% | ||

| 01:30 | AUD | Employment Change Mar | 17.9K | 30.0K | 77.4K | |

| 01:30 | AUD | Unemployment Rate Mar | 4.00% | 3.90% | 4.00% | |

| 06:30 | CHF | Producer and Import Prices M/M Mar | 0.80% | 0.00% | 0.40% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Mar | 6.10% | 4.90% | 5.80% | |

| 11:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | 0.00% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | CAD | Manufacturing Sales M/M Feb | 4.20% | 0.00% | 0.60% | |

| 12:30 | CAD | Wholesale Sales M/M Feb | -0.40% | 0.70% | 4.20% | |

| 12:30 | USD | Initial Jobless Claims (Apr 8) | 185K | 175K | 166K | |

| 12:30 | USD | Retail Sales M/M Mar | 0.50% | 0.60% | 0.30% | 0.80% |

| 12:30 | USD | Retail Sales ex Autos M/M Mar | 1.10% | 0.70% | 0.20% | 0.60% |

| 12:30 | USD | Import Price Index M/M Mar | 2.60% | 2.30% | 1.40% | 1.60% |

| 14:00 | USD | Michigan Consumer Sentiment Index Apr P | 58.8 | 59.4 | ||

| 14:00 | USD | Business Inventories Feb | 1.00% | 1.10% | ||

| 14:30 | USD | Natural Gas Storage | 15B | -33B |