Yen’s selloff intensifies today, following extended rally in major benchmark treasury yields. US 10-year yields breaks 2.75% handle for the first time since March2 019. Germany 10-year bund yield also breaches 0.8% handle. On the other hand, Japan 10-year JGB yield is staying comfortably below BoJ’s 0.25% cap. Euro and Dollar are currently the strongest one for today. Sterling is not performing too badly despite GDP miss. Commodity currencies are following risk-off sentiments lower.

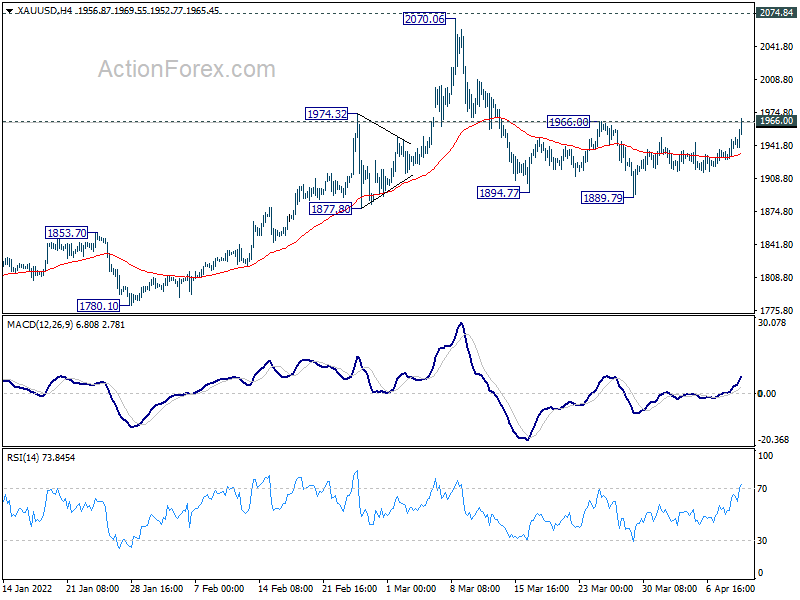

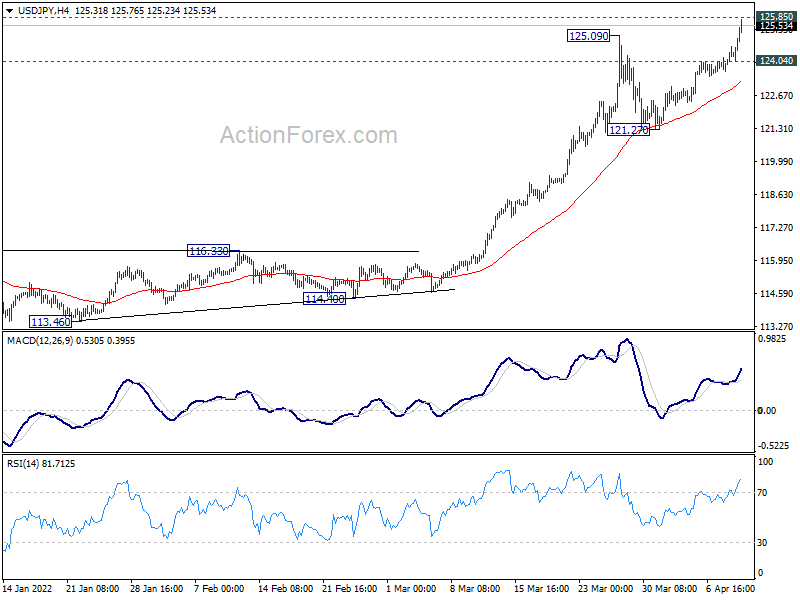

Technically, USD/JPY’s break of 125.09 resistance confirms long term up trend resumption. Now, it’s the time for EUR/JPY to break through 137.49 resistance, and for GBP/JPY to break through 164.61 resistance to alight the outlook. Meanwhile, Gold’s break of 1966.00 resistance now argues that correction from 2070.06 has completed at 1889.79. It could try to head back to 2000 handle if risk aversion picks up.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.66%. DAX is down -0.87%. CAC is up 0.26%. Germany 10-year yield is up 0.092 at 0.799. Earlier in Asia, Nikkei dropped -0.61%. Hong Kong HSI dropped -3.03%. China Shanghai SSE dropped -2.61%. Singapore Strait Times dropped -0.58%. Japan 10-year JGB yield rose 0.0081 to 0.239.

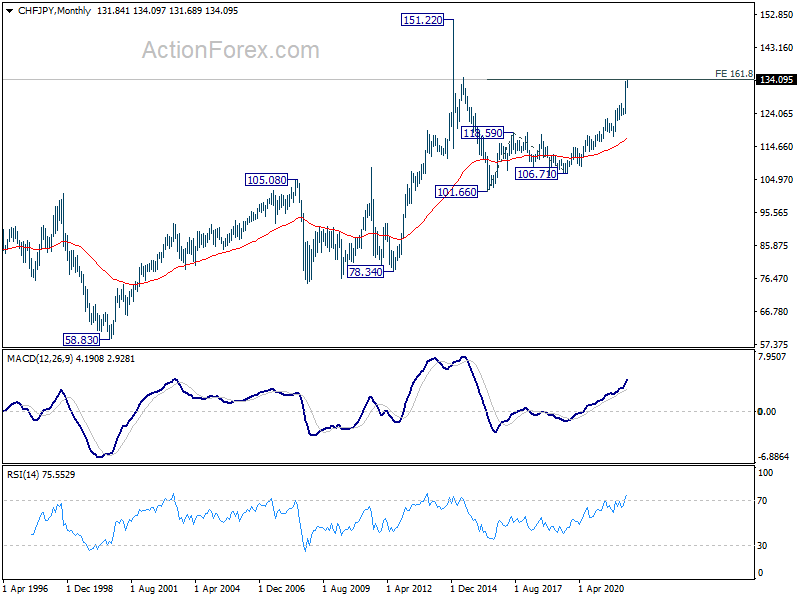

CHF/JPY upside breakout as Yen selloff intensifies

Yen selloff steps up a gear today and even CHF/JPY breaks through short term top at 133.53 to resume its long term up trend. For now, short term outlook will remain bullish as long as 130.74 support holds. There is prospect of upside acceleration to next target at 161.8% projection of 117.51 to 127.05 from 124.23 at 139.66.

More importantly, as seen in the monthly chart, CHF/JPY is now trying to break through 161.8% projection of 101.66 to 118.59 from 106.71 at 134.10. Sustained trading above this level could set up the for medium term upside acceleration towards 151.22 (2014 spike high).

{kind=link}

{kind=link}

UK GDP grew only 0.1% mom in Feb, production contracted

UK GDP grew 0.1% mom only in February, below expectation of 0.3% mom. Services was the main contributor to growth, up 0.2% mom. But that was offset by -0.6% mom contraction in production, and -0.1% mom in construction.

Overall monthly GDP was 1.5% above its pre-coronavirus level in February 2020. Services was 2.1% above that level while construction was 1.1% above. However, production was -1.9% below.

Also published, manufacturing production came in at -0.4% mom, 3.6% yoy, versus expectation of 0.4% mom, 2.5% yoy. Industrial production came in at -0.6% mom, 1.6% yoy, versus expectation of 0.4% mom, 1.4% yoy. Goods trade deficit narrowed to GBP -20.6B, larger than expectation of GBP -16.8B.

BoJ Kuroda: Economy to continue to recover despite rising commodity prices

BoJ Governor Haruhiko Kuroda said in the quarterly branch manager meeting, “Japan’s economy has picked up as a trend, although some weakness has been seen in part, mainly due to the impact of COVID-19.”

“As downward pressure on service consumption and the impact of supply shortages diminish, a pickup in overseas demand, accommodative monetary policy, and the government’s economic stimulus will likely help the Japanese economy recover despite being affected by rising commodity prices,” he added.

Kuroda also cautioned that “extremely high uncertainties” remain over how the crisis in Ukraine will impact commodity prices and the Japanese economy. But he also indicated that commodity inflation is unlikely to trigger a change in the central bank’s ultra-loose policy, because it wouldn’t last long.

China PPI slowed to 8.3% yoy, CPI rose to 1.5% yoy in Mar

China PPI slowed from 8.8% yoy to 8.3% yoy, but still beat expectation of 7.9% yoy. However, the monthly rise of 1.1% mom in PPI was the fastest in five months, driven by surges in oil prices and non-ferrous metals.

CPI accelerated from 0.9% yoy to 1.5% yoy in March, above expectation of 1.2% yoy. Core CPI, excluding food and energy, rose 1.1% yoy, unchanged from February’s reading. Prices of some food like flour, vegetable oil, fresh vegetables and eggs rose and were “affected by the rise in international prices of wheat, corn and soybeans and the domestic [coronavirus] outbreaks”, noted senior NBS statistician Dong Lijuan.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 123.74; (P) 124.21; (R1) 124.75; More…

USD/JPY’s break of 125.09 resistance confirms resumption of larger up trend from 102.58. Intraday bias is now on the upside. Decisive break of 125.86 long term resistance will pave the way to 130.04 long term projection level next. On the downside, below 123.44 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 121.27 support holds.

{kind=link}

In the bigger picture, up trend from 98.97 (2016 low) is in progress for retesting 125.85 (2015 high). Sustained break there will confirm long term up trend resumption. Next target will be 61.8% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 130.04. This will now remain the favored case as long as 116.34 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Mar | 1.50% | 1.20% | 0.90% | |

| 01:30 | CNY | PPI Y/Y Mar | 8.30% | 7.90% | 8.80% | |

| 06:00 | GBP | GDP M/M Feb | 0.10% | 0.30% | 0.80% | |

| 06:00 | GBP | Manufacturing Production M/M Feb | -0.40% | 0.40% | 0.80% | 0.90% |

| 06:00 | GBP | Manufacturing Production Y/Y Feb | 3.60% | 2.50% | 3.60% | 5.30% |

| 06:00 | GBP | Industrial Production M/M Feb | -0.60% | 0.40% | 0.70% | |

| 06:00 | GBP | Industrial Production Y/Y Feb | 1.60% | 1.40% | 2.30% | 3.00% |

| 06:00 | GBP | Index of Services 3M/3M Feb | 0.10% | 0.90% | 1.00% | 0.80% |

| 06:00 | GBP | Goods Trade Balance (GBP) Feb | -20.6B | -16.8B | -26.5B | |

| 13:00 | GBP | NIESR GDP Estimate Mar | 1.00% | 1.00% |