Euro turns slightly softer after poor German business climate reading, in particular against Swiss Franc, Aussie and Loonie. Dollar is also weak except versus Yen. Yen is trying to recover but there is no clear follow through buying. It’s the the runaway loser of the week. Overall, Aussie is set to end as the week as the best performer.

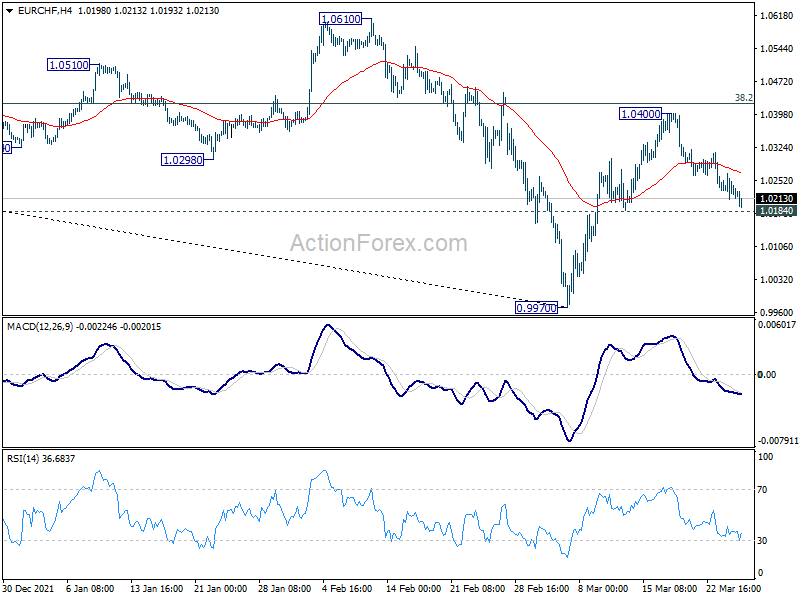

Technical, 1.0815 support in EUR/CHF is worth a watch early next week. Firm break there should confirm completion of the rebound from 0.9970, and retest of this low should be seen next. The development could be accompanied by downside breakout in both EUR/CAD and EUR/AUD for down trend resumption too.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.87%. CAC is up 0.68%. Germany 10-year yield is up 0.0268 at 0.561. Earlier in Asia, Nikkei rose 0.14%. Hong Kong HSI dropped -2.47%. China Shanghai SSE dropped -1.17%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield closed flat at 0.240.

Germany Ifo business climate dropped to 90.8, record collapse in expectations

Germany Ifo Business Climate dropped from 98.5 to 90.8 in March, below expectation of 94.5. Current Situation index dropped from 98.6 to 97.0, below expectation of 97.3. Expectations index dropped from 98.4 to 85.1, well below expectation of 97.2, and a record collapse.

By sector, manufacturing dived from 23.1 to -3.3. Services dropped from 13.6 to 0.7. Trade dropped from 6.6 to -12.0. Construction dropped from 8.0 to -12.2.

UK retail sales dropped -0.3% mom in Feb, ex-fuel sales down -0.7% mom

UK retail sales volume dropped -0.3% mom in February, much worse than expectation of 1.0% mom rise. On a 12-month basis, sales rose 7.0% yoy, below expectation of 7.8% yoy. Also, sales volume was 3.7% above pre-pandemic level in February 2020.

Ex-fuel sales volume dropped -0.7% mom, below expectation of 0.5% mom. On a 12-month basis, sales rose 4.6% yoy, below expectation of 5.0% yoy. Ex-fuel sales volume was 4.0% above pre-pandemic level in February 2020.

Auto fuel sales volume rose 3.6% mom, above pre-pandemic level (by 0.9%) for the first time, on lifting of restrictions and increased travel.

UK Gfk consumer confidence dropped to -31, a wall of worry is confronting

UK Gfk Consumer Confidence Index dropped from -26 to -31 in March. That’s the lowest level since November 2020. Personal Financial Situation over last 12 months dropped from -11 to -13. Personal Financial Situation over next 12 months dropped from -14 to -18. General Economic Situation over last 12 months dropped slightly from -50 to -51. Genera Economic Situation over next 12 months dropped from -43 to -49.

Joe Staton, Client Strategy Director GfK, says: “A wall of worry is confronting consumers this month and there is an unmistakable sense of crisis in our numbers. Consumers across the UK are experiencing the impact of soaring living costs with 30-year-high levels of inflation, record-high fuel and food prices, a recent interest-rate hike and the prospect of more increases to come, and higher taxation too – all against a background of stagnant pay rises that cannot compensate for the financial duress. This is the fourth month in a row that UK consumer confidence has dropped.”

BoJ Kuroda: Weak yen is generally positive for Japan’s economy

BoJ Governor Haruhiko Kuroda told the parliament, “there’s no change now to my view a weak yen is generally positive for Japan’s economy.”

He also reiterated the view that “cost-push inflation that is not accompanied by wage hikes will hurt Japan’s economy.” And as such, “it won’t lead to sustained achievement of our price target. That’s why the BOJ will continue to maintain powerful monetary easing.”

Released from Japan, Tokyo CPI core rose from 0.5% yoy to 0.8% yoy in March, above expectation of 0.7% yoy. Corporate service price index rose 1.1% yoy in February, below expectation of 1.2% yoy.

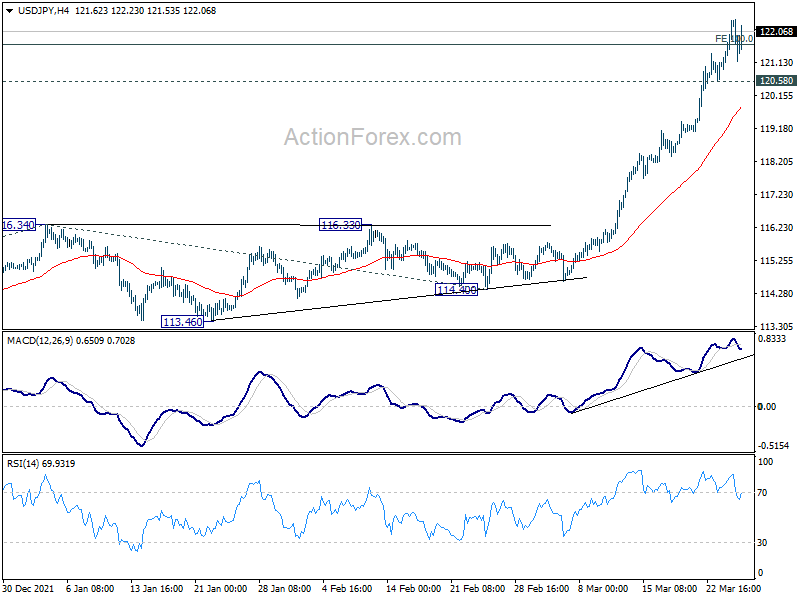

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 121.41; (P) 121.91; (R1) 122.86; More…

USD/JPY is losing some upside momentum as seen in 4 hour MACD. But with 120.58 minor support intact, intraday bias stays on the upside. Sustained trading above 100% projection of 109.11 to 116.34 from 114.40 at 121.63, will pave the way to 125.85 long term resistance. On the downside, however, below 120.58 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

{kind=link}

In the bigger picture, the break of 118.65 resistance (2016 high) suggest that up trend from 98.97 (2016 low) is resuming, with rise from 101.18 (2020 low) as the third leg. Medium term outlook will remain bullish as long as 116.34 resistance turned support holds. Next target is 125.85 (2015 high).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Mar | 0.80% | 0.70% | 0.50% | |

| 23:30 | JPY | Corporate Service Price Index Y/Y Feb | 1.10% | 1.20% | 1.20% | |

| 00:01 | GBP | GfK Consumer Confidence Mar | -31 | -30 | -26 | |

| 07:00 | GBP | Retail Sales M/M Feb | -0.30% | 1.00% | 1.90% | |

| 05:30 | GBP | Retail Sales Y/Y Feb | 7.00% | 7.80% | 9.10% | 9.40% |

| 07:00 | GBP | Retail Sales ex-Fuel M/M Feb | -0.70% | 0.50% | 1.70% | |

| 05:30 | GBP | Retail Sales ex-Fuel Y/Y Feb | 4.60% | 5.00% | 7.20% | 7.50% |

| 09:00 | EUR | Germany IFO Business Climate Mar | 90.8 | 94.5 | 98.9 | 98.5 |

| 09:00 | EUR | Germany IFO Current Assessment Mar | 97 | 97.4 | 98.6 | |

| 09:00 | EUR | Germany IFO Expectations Mar | 85.1 | 97.2 | 99.2 | 98.4 |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 6.30% | 6.30% | 6.40% | |

| 14:00 | USD | Pending Home Sales M/M Feb | 1.40% | -5.70% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Mar F | 59.7 | 59.7 |