The forex markets are engaging in sideway trading in tight range in Asia today. The selling climax on Yen should have passed for the near term, with Yen pairs turned into consolidation mode. But the Japanese currency remains the runaway loser for the week, followed by Euro at a distant, and then Swiss Franc and Dollar. Australian Dollar is still the strongest one, together with other commodity currencies and Sterling.

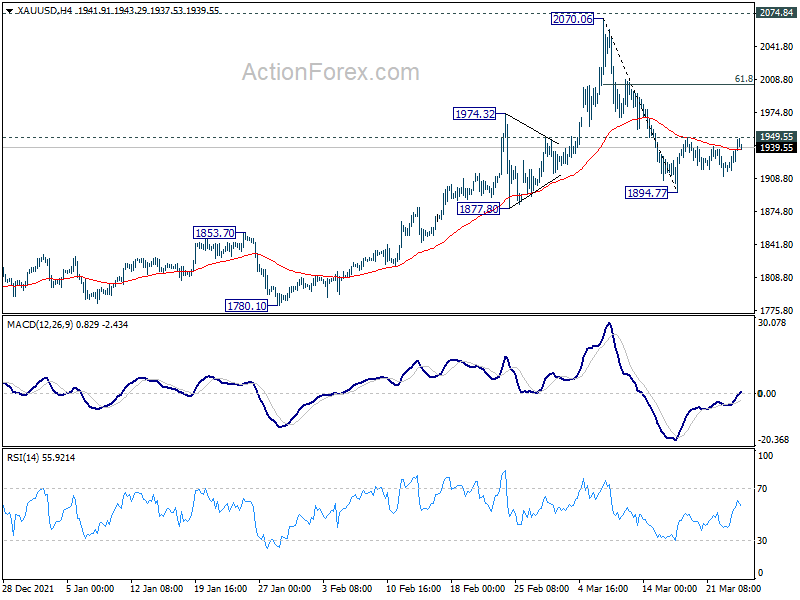

Technically, Gold’s break of 4 hour 55 EMA is a near term positive sign. Yet, it still has to break through 1949.55 minor resistance to resume the rebound from 1894.77. In that case, Gold should target 61.8% retracement of 2070.06 to 1894.77 at 2003.09, which is close to 2000 handle. Such development, if happens, could be accompanied by resumption of EUR/USD’s rebound from 1.0805.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.25%. Hong Kong HSI is up 0.19%. China Shanghai SSE is down -0.54%. Singapore Strait Times is up 0.80%. Japan 10-year JGB yield is up 0.005 at 0.231. Overnight, DOW dropped -1.29%. S&P 500 dropped -1.23%. NASDAQ dropped -1.32%. 10-year yield dropped -0.052 to 2.321.

Fed Mester: We’re going to need to do some 50 basis-point moves

Cleveland Fed President Loretta Mester reiterated yesterday that Fed should “front-load” interest rate hikes in the first of of the year, and start quantitative tightening at the same time. “We have to recognize that inflation is very elevated. It is well above our goal. We have to do what we can with both our policy tools to get inflation under control,” she emphasized.

“I think we’re going to need to do some 50 basis-point moves,” Mester added. “I don’t want to presuppose every meeting from here to July, but I do think we need to be more aggressive earlier rather than later.”

Fed Daly: If we need to do 50, that is what we’ll do

San Francisco Fed President Mary Daly said she has “everything on the table” for the May FOMC meeting. “If we need to do 50, that is what we’ll do,” she added. “We’re prepared to do whatever it takes to ensure that we get price stability, which clearly no one thinks we have right now.”

Daly pointed to the new dot plot projection that interest rate will rise to 1.9% this year, and 2.8% by the end of next. “Relative to previous periods of tightening, this is quite a bit of front-loading just as the SEP (Summary of Economic Projections) has indicated.”

“I don’t think it’s appropriate to you, you know, really ratchet up so quickly, that we forget about the risks out there, but rather we be data dependent,” she said.

“We could get a lot of tightening in financial conditions globally and that is something we have to think about,” she said. “Some increase in the policy rate above neutral is likely to be required. That’s down the road in 2023. Right now I don’t think we need to be so decisional on what that looks like.”

BoJ Kataoka: Pay attention to downside risks to economy, upside risks to prices

BoJ board member Goushi Kataoka warned in a speech to business leaders, “disruptions in Russia-related trade will weigh not just on Russia’s economy but global growth by prolonging worldwide supply constraints.” And for the time being, “we must pay attention to downside risks to Japan’s economy…as well as upside risks to prices.”

Separately, meeting of January BoJ meeting noted one member said, “We’re seeing stock prices rise for companies that hike prices. Price hikes may broaden, and heighten medium- to long-term inflation expectations.”

Another member said, “many companies are feeling the limit of sticking to a business model that was effective deflation. As they change their price-setting behaviour, inflationary pressure may heighten.”

However, “nominal wage growth must exceed 2per cent for Japan to stably meet the BOJ’s price target,” on member was quoted.

Japan PMI manufacturing rose to 53.2 in March, PMI services rose to 48.7

Japan PMI Manufacturing rose from 52.7 to 53.2 in March. Manufacturing output rose from 49.3 to 50.6. PMI Services rose from 44.2 to 48.7. PMI Composite rose from 45.8 to 49.3.

Usamah Bhatti, Economist at S&P Global, said: “Flash PMI data indicated that activity at Japanese private sector businesses fell for the third month running during March. The decline in output eased from the previous survey period however, and was only marginal as companies noted that COVID-19 cases had continued to reduce, allowing the lifting of the quasi-state of emergency across Japan. By sector, manufacturers noted a renewed rise in output in at the end of the first quarter, while service providers indicated a softer deterioration in business activity.

Australia PMI composite rose to 57.1, 10-mth high

Australia PMI Manufacturing rose from 57.0 to 57.3 in March. PMI Services rose from 57.4 to 57.9, a 10-month high. PMI Composite rose from 56.6 to 57.1, also a 10-month high.

Jingyi Pan, Economics Associate Director at S&P Global said: “The Australian economy continued to expand strongly in March… reflecting robust business conditions post the COVID-19 Omicron wave. Price pressures worsened, however, unsurprisingly aggravated by the slew of issues including floodings in Australia, the Ukraine war and broader supply chain constraints…

“Higher employment levels in March had been a positive sign, though firms also widely reported higher wages. Meanwhile the reopening of the international borders led to the first new export business growth in the service sector since June 2021.”

IMF: RBNZ should continue swift policy normalization

In a report, IMF urged RBNZ to have “significant increases” in interest range in the near term to address inflation as a priority.

IMF said, “with the recovery well-entrenched, tight labor market conditions, and elevated inflation, it is appropriate to withdraw fiscal and monetary support as envisaged.”

Fiscal policy should “remain agile”. “While the scheduled tightening of fiscal policy is appropriate, the authorities should calibrate the fiscal stance to the evolution of the pandemic and economic conditions, providing additional, targeted support where needed.”

As for monetary policy, IMF said it should remain “data dependent, and continued, swift policy normalization will be appropriate under baseline conditions.”

“Given New Zealand’s strong cyclical position and inflationary pressures, significant increases in the Official Cash Rate in the near term are appropriate, signaling the RBNZ’s commitment to addressing inflation as a priority.”

Looking ahead

SNB is expected to keep interest rate unchanged at -0.75% today, and reiterate the need for negative rate and readiness for intervention. ECB will release monthly economic bulletin.

On the data front, PMIs from Eurozone and UK will be featured. US will release jobless claims, durable goods orders, current account and PMIs.

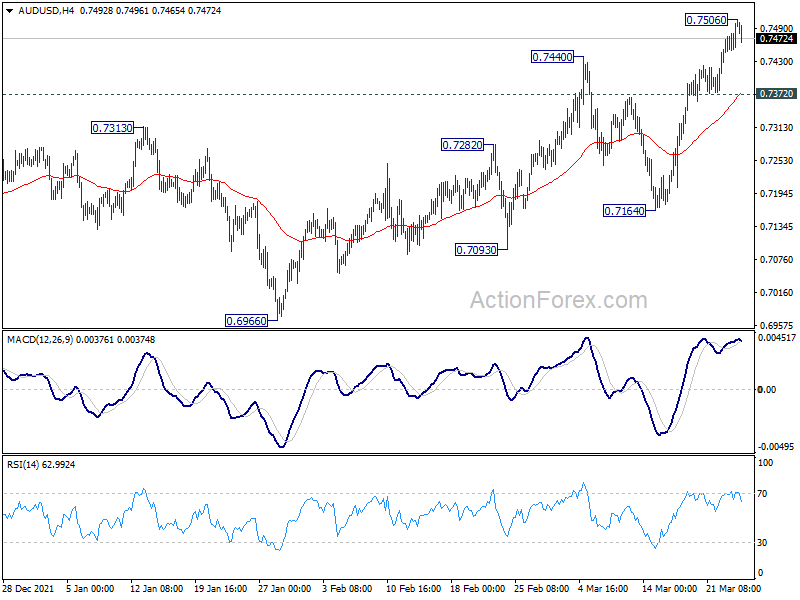

AUD/USD Daily Report

Daily Pivots: (S1) 0.7464; (P) 0.7486; (R1) 0.7521; More…

A temporary top is formed at 0.7506 on loss of upside momentum. Intraday bias in AUD/USD is turned neutral first. Further rally is expected as long as 0.7372 support holds. On the upside, above 0.7506 will target 0.7555 resistance. Decisive break there should confirm that whole corrective decline from 0.8006 has completed at 0.6966. On the downside, however, break of 0.7372 will dampen this bullish case, and turn bias back to the downside for 0.7164 support.

{kind=link}

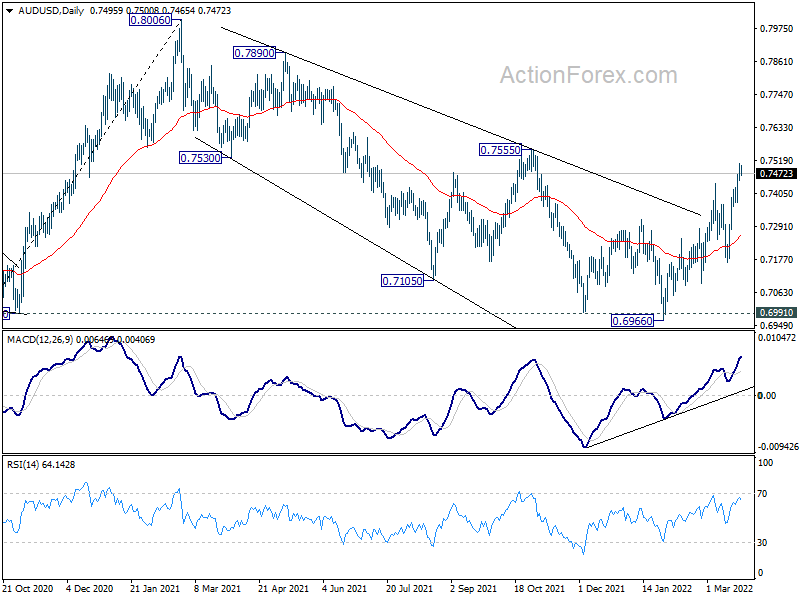

In the bigger picture, focus remains on 0.6991 key structural support. Sustained break there will argue that the whole up trend from 0.5506 might be finished at 0.8006, after rejection by 0.8135 long term resistance. Deeper decline would then be seen back to 61.8% retracement of 0.5506 to 0.8006 at 0.6461. Meanwhile, strong rebound from 0.6991 will retain medium term bullishness. That is, whole up trend from 0.5506 is still in progress for another rise through 0.8006 at a later stage.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Mar P | 57.3 | 57 | ||

| 22:00 | AUD | Services PMI Mar P | 57.9 | 57.4 | ||

| 23:50 | JPY | BoJ Minutes | ||||

| 00:30 | JPY | Manufacturing PMI Mar P | 53.2 | 52.7 | ||

| 07:45 | EUR | France Manufacturing PMI Mar P | 55.1 | 57.2 | ||

| 08:15 | EUR | France Services PMI Mar P | 55.2 | 55.5 | ||

| 08:15 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | ||

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 55.9 | 58.4 | ||

| 08:30 | EUR | Germany Services PMI Mar P | 54.3 | 55.8 | ||

| 08:30 | EUR | ECB Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 56 | 58.2 | ||

| 09:00 | EUR | Eurozone Services PMI Mar P | 54.3 | 55.5 | ||

| 09:00 | GBP | Manufacturing PMI Mar P | 57.7 | 58 | ||

| 09:30 | GBP | Services PMI Mar P | 58 | 60.5 | ||

| 12:30 | USD | Initial Jobless Claims (Mar 18) | 210K | 214K | ||

| 12:30 | USD | Current Account (USD) Q4 | -218B | -215B | ||

| 12:30 | USD | Durable Goods Orders Feb | -0.60% | 1.60% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Feb | 0.50% | 0.70% | ||

| 13:45 | USD | Manufacturing PMI Mar P | 55 | 57.3 | ||

| 13:45 | USD | Services PMI Mar P | 56 | 56.5 | ||

| 13:45 | USD | Natural Gas Storage | -52B | -79B |