Yen is finally recovering slightly today, as selloff in bonds ease. That is by no means an indication of reversal. But the Japanese currency should be turning into a consolidation phase after recent massive selloff. Dollar is also firming up slightly too, except versus Yen and Aussie. On the other hand, the rebound in Sterling seems to have lost all its momentum, except versus Euro, which is turning weaker again too.

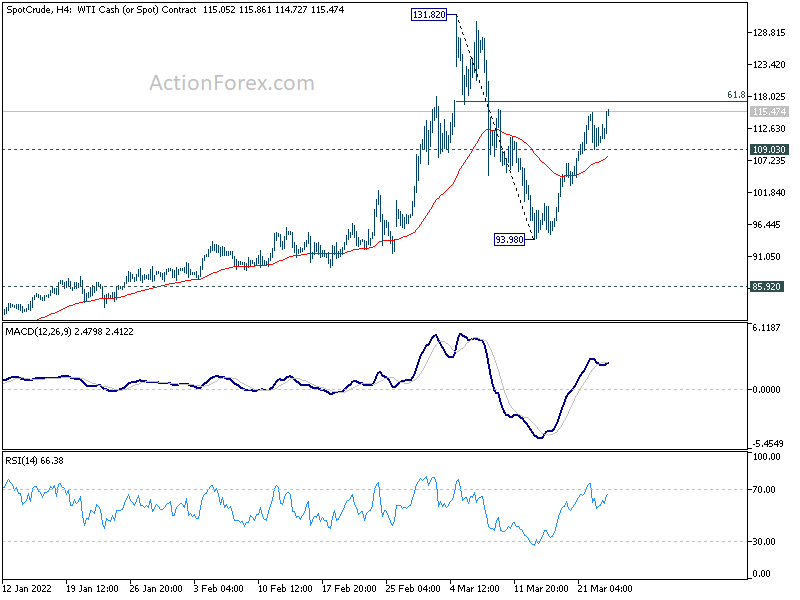

Technically, WTI crude oil’s rebound from 93.98 resumes after brief retreat and it’s back above 115.5. For now further rise is in favor as long as 109.03 minor support holds. Firm break of 61.8% retracement of 131.82 to 93.98 at 117.36 could pave the way back to 131.82 high. Such development could have a knock on the rebound in stocks, or at least cap the momentum.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -1.30%, CAC is down -1.00%. Germany 10-year yield is down -0.0193 at 0.487. Earlier in Asia, Nikkei rose 3.00%. Hong Kong HSI rose 1.21%. China Shanghai SSE rose 0.34%. Japan 10-year JGB yield rose 0.0063 to 0.226.

UK CPI rose to 6.2% yoy in Feb, core CPI up to 5.2% yoy

UK CPI rose 0.8% mom in February, above expectation of 0.6% mom. That’s also the largest monthly rise since 2009. On a 12-month basis, CPI surged from 5.5% to 6.2% yoy, above expectation of 5.9% yoy. That’s the highest on record since 1997, and the highest rate is historic modelled series since March 1992. CPI core also rose from 4.4% yoy to 5.2% yoy, above expectation of 4.8% yoy.

Also release, PPI input was at 1.4% mom, 14.6% yoy in February, versus expectation of 1.2% mom, 13.9% yoy. PPI output was at 0.8% mom, 10.1% yoy, versus expectation of 0.7% mom, 10.2% yoy. PPI output core was at 0.7% mom, 9.9% yoy, versus expectation of 0.9% mom, 10.0% yoy.

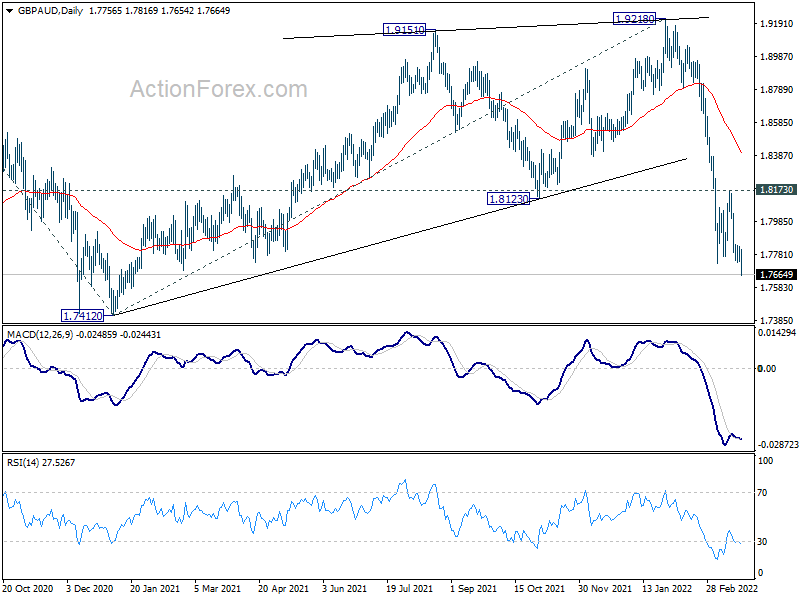

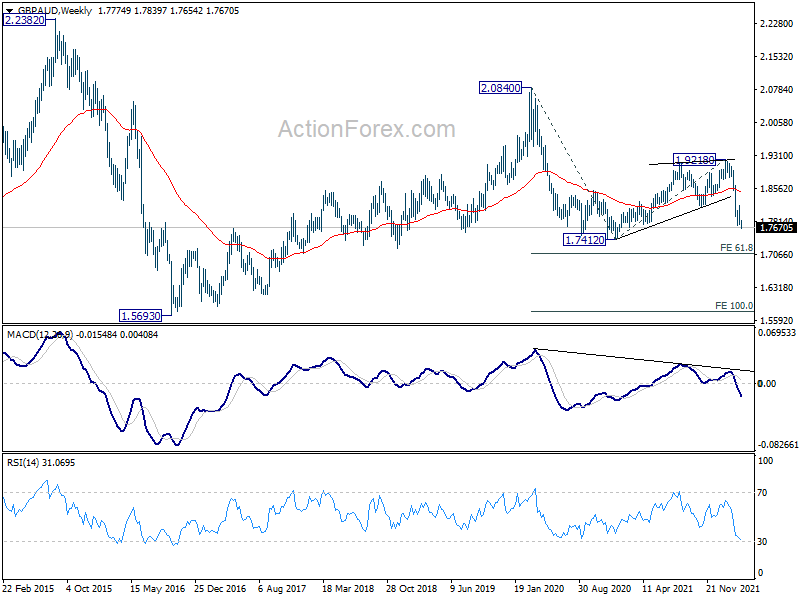

GBP/AUD heading to 1.74 as near term fall resumes

GBP/AUD’s fall from 1.9218 resumed by breaking through 1.7729 support last today. For now, near term outlook stays bearish as long as 1.8173 resistance holds, next target is 1.7412 low.

Current fall from 1.9812 is seen as resuming the medium term down trend from 2.0840 (2020 high). Break of 1.7412 will target 61.8% projection of 2.0840 to 1.7412 from 1.9218 at 1.7099.

{kind=link}

{kind=link}

Nikkei gained 3%, broke near term structural resistance

Nikkei staged another power full rally today after a gap up, gained 3.00% or 816.05 pts to 28040.16. Export-oriented shares led the rally, with help from recent decline in Yen exchange rate. Japan Prime Minister Fumio Kishida also promised to carry out solid counter-measures for rising prices of oil, raw materials and goods, to revive Japan’s economy”.

Nikkei’s break of 27880.69 resistance argues that corrective pull back from 30795.66 might have finished at 24681.74 already. Sustained of falling channel resistance (now at 26650) will affirm this bullish case and pave the way to retest 30795.77 high.

In the bigger picture, 38.2% retracement of 16358.19 to 30795.77 at 25280.61 is seen as being defended already, despite a brief breach earlier this month. The break above 55 week EMA is also a positive sign. Up trend from 16358.19 might be ready to resume during next quarter.

{kind=link}

{kind=link}

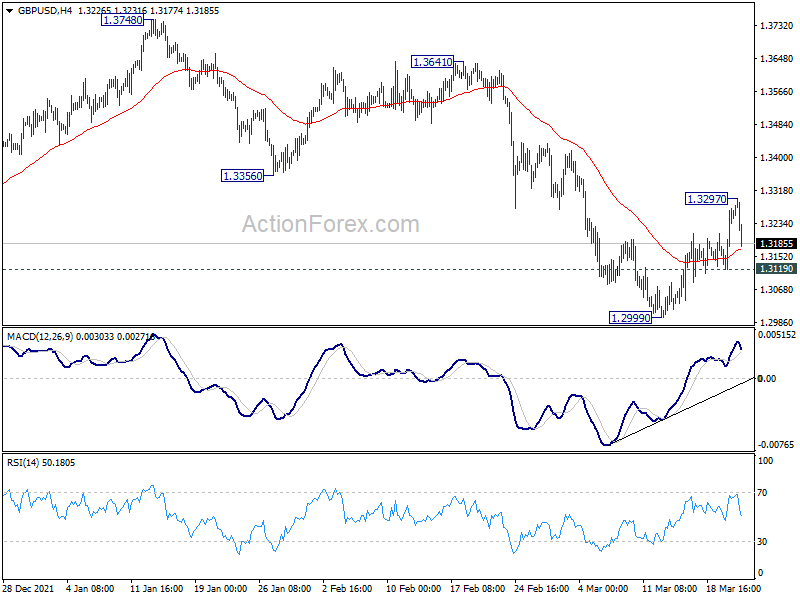

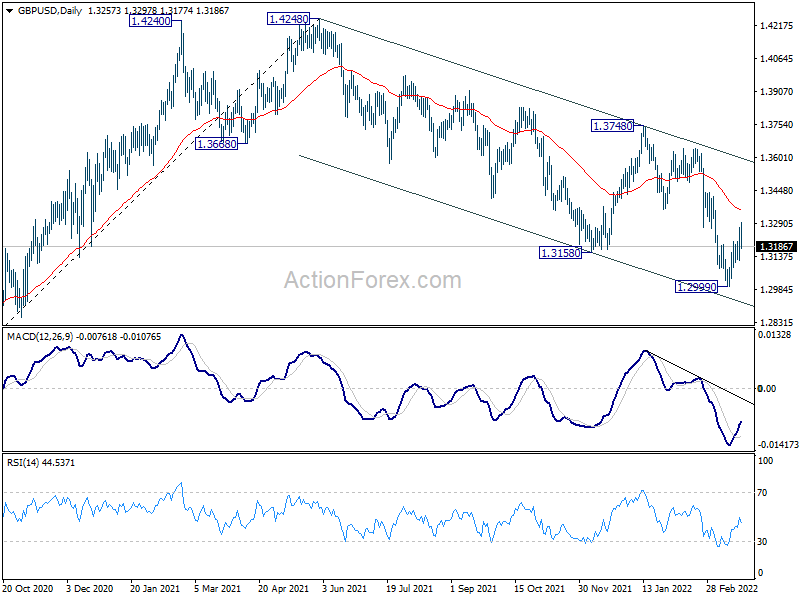

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3164; (P) 1.3219; (R1) 1.3318; More…

Intraday bias in GBP/USD is turned neutral as it retreated sharply after hitting 1.3297. On the downside, break of 1.3119 minor support will turn bias back to the downside for retesting 1.2999. Firm break there will resume larger down trend from 1.4248. On the upside, above 1.3297 will resume the rebound to 55 day EMA (now at 1.3355). Sustained break there will target medium term channel resistance (now at 1.3590).

{kind=link}

In the bigger picture, current development suggests that the up trend from 1.1409 (2020 low) has completed at 1.4248. Decline from 1.4248 could still be a corrective move, or it could be the start of a long term down trend. In either case, deeper decline would be seen back to 61.8% retracement of 2.1161 to 1.1409 at 1.2493. In any case, break of 1.3748 resistance is needed to indicate medium term bottoming, or outlook will stay bearish.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | GBP | CPI M/M Feb | 0.80% | 0.60% | -0.10% | |

| 07:00 | GBP | CPI Y/Y Feb | 6.20% | 5.90% | 5.50% | |

| 07:00 | GBP | CPI Core Y/Y Feb | 5.20% | 4.80% | 4.40% | |

| 07:00 | GBP | RPI M/M Feb | 0.80% | 0.70% | 0.00% | |

| 07:00 | GBP | RPI Y/Y Feb | 8.20% | 8.10% | 7.80% | |

| 07:00 | GBP | PPI Input M/M Feb | 1.40% | 1.20% | 0.90% | 1.50% |

| 07:00 | GBP | PPI Input Y/Y Feb | 14.70% | 13.90% | 13.60% | 14.20% |

| 07:00 | GBP | PPI Output M/M Feb | 0.80% | 0.70% | 1.20% | |

| 07:00 | GBP | PPI Output Y/Y Feb | 10.10% | 10.20% | 9.90% | |

| 07:00 | GBP | PPI Core Output M/M Feb | 0.70% | 0.90% | 1.10% | 1.20% |

| 07:00 | GBP | PPI Core Output Y/Y Feb | 9.90% | 10.00% | 9.30% | 9.50% |

| 14:00 | USD | New Home Sales Feb | 815K | 801K | ||

| 14:30 | USD | Crude Oil Inventories | -0.7M | 4.3M | ||

| 15:00 | EUR | Eurozone Consumer Confidence Mar P | -13 | -9 |