Euro and Sterling are the relatively stronger ones today, but gains are so far limited. The rallies are still capped by the war uncertainties. Economic data is not really playing a role here, considering the UK job data was solid while German economic sentiment plunged. Meanwhile, Canadian Dollar and Swiss Franc are the softest ones, followed by Dollar. Yen’s selling looks exhausted ahead of a key resistance level against the greenback.

Technically, a focus will be on whether Euro and Sterling could real stage a sustainable rebound. EUR/CHF and EUR/JPY are performing well. But EUR/USD is still limited below 1.1120 resistance. For Sterling, GBP/USD is held below 1.3193 resistance, GBP/JPY below 155.20 resistance. These levels need to be broken to confirm a short term turnaround in both currencies.

In Europe, at the time of writing, FTSE is down -0.62%. DAX is down -0.62%. CAC is down -0.64%. Germany 10-year yield is down -0.035 at 0.333. Earlier in Asia, Nikkei rose 0.15%. Hong Kong HSI dropped -5.72%. China Shanghai SSE dropped -4.95%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield rose 0.0154 at 0.211.

US PPI rose 0.8% mom, 10.0% yoy in Feb

US PPI for final demand rose 0.8% mom in February, below expectation of 1.0% mom. On an unadjusted basis, final demand prices moved up 10.0 yoy for the 12 months ended in February, matched expectations. Prices for final demand goods was up 2.4% mom while prices for final demand services was unchanged.

Empire State Manufacturing index dropped sharply from 3.1 to -11.8 in March, well below expectation of 7.3.

Canada manufacturing sales rose 0.6% mom in Jan

Canada manufacturing sales rose 0.6% mom to CAD 64.8B in January, below expectation of 1.3% mom. That’s nonetheless the fourth consecutive month of increase. Sales rose in 14 of 21 industries, led by the petroleum and coal (+6.8%) and wood (+6.5%) product industries. The gain was partially offset by lower sales of motor vehicles (-17.5%).

German ZEW had largest fall on record, expect a stagflation in the coming months

German ZEW Economic Sentiment tumbled sharply from 54.3 to -39.3 in March, well below expectation of 10.3. That -93.6 pts decline was the largest on record, since the survey began in December 1991. That’s even worse than the -58.2 pts fall at the beginning of the pandemic. Current Situation Index dropped from -8.1 to -21.4, slightly better than expectation of -22.5.

Eurozone ZEW Economic Sentiment dropped from 48.6 to -38.7, below expectation of 49.3. Current Situation Index dropped 22.5 pts to -21.9.

Inflation expectations indicator stands at jumped sharply from -35.1 to 69.5. 76.5 per cent of the experts expect the inflation rate to increase in the next six months.

“A recession is becoming more and more likely. The war in Ukraine and the sanctions against Russia are significantly dampening the economic outlook for Germany. The collapsing economic expectations are accompanied by an extreme rise in inflation expectations. The experts therefore expect a stagflation in the coming months. The worsened outlook affects practically all sectors of the German economy, but especially the energy-intensive sectors and the financial sector,” comments ZEW President Achim Wambach on current expectations.

Eurozone industrial production flat in Jan, EU rose 0.4% mom

Eurozone industrial production rose 0.0% mom in January, below expectation of 0.4% mom. Production of non-durable consumer goods rose by 3.1%, while production of intermediate goods and energy both fell by -0.3%, durable consumer goods by -0.5% and capital goods by -2.4%.

EU industrial production rose 0.4% mom. Among Member States for which data are available, the largest monthly increases were registered in Austria (+6.2%), Czechia (+3.1%) and Poland (+3.0%). The highest decreases were observed in Estonia (-6.1%), Portugal (-5.0%) and Greece (-4.1%).

UK payrolled employees rose 275k in Feb, unemployment rate dropped to 3.9% in Jan

UK number of payrolled employees rose 275k in February. Comparing with prepandemic level in February 2020, number of payrolled employees was up 662k. Claimant count dropped -48.1k, versus expectation of 20.3k rise.

In the three months to January, unemployment rate dropped from 4.1% to 3.9% in the three months to January, better than expectation of 4.0%.

Average earnings including bonus rose 4.8% 3moy in January, above expectation of 4.6%. Average earnings excluding bonus rose 3.8% 3moy, also above expectation of 3.7%.

China industrial production and retail sales growth unexpectedly strong

For the two months of January and February, China industrial production grew 7.5% yoy, well above expectation of 3.9% yoy. That’s the fastest pace since June 2021. Retail sales rose 6.7% yoy, also well above expectation of 3.0% yoy, also the fastest since June 2021. Fixed asset investment rose 12.2% yoy, above expectation of 5.0% yoy, highest since July 2021.

Separately, PBoC unexpectedly kept the rate of CNY 200B worth of one-year medium term lending facility (MLF) loans to some financial institutions unchanged at 2.85%. The operation resulted in a net injection of CNY 100B funds to the market. The central bank said it is for “maintaining banking system liquidity reasonably ample”.

RBA minutes reiterate patient stance on interest rate

In the minutes of March 1 meeting, RBA reiterated that it will not hike cash rate “until actual inflation is sustainably within the 2 to 3 per cent target band. Now, it was “too early to conclude that” inflation is “sustainably within the target band”.

There were “uncertainties about how persistent the pick-up in inflation”. Wage growth “remained modest”, and “it was likely to be some time before aggregate wages growth would be at a rate consistent with inflation being sustainably at target.”

Thus, RBA is “prepared to be patient” on lifting interest rate.

New Zealand BNZ services index rose to 48.6, pain is accumulating

New Zealand BNZ Performance of Services Index rose slightly from 46.0 to 48.6 in February. Activity/sales rose from 44.6 to 50.7. Employment dropped from 47.0 to 45.0. New orders/business rose from 41.2 to 53.6. Stocks/inventories rose from 48.0 to 50.0. Supplier deliveries dropped from 43.4 to 34.4.

BNZ Senior Economist Doug Steel said that “February marks the PSI’s seventh consecutive month below the breakeven 50 mark. Pain is accumulating. While there were some overs and unders in the components, all remain below their respective long-term averages.”

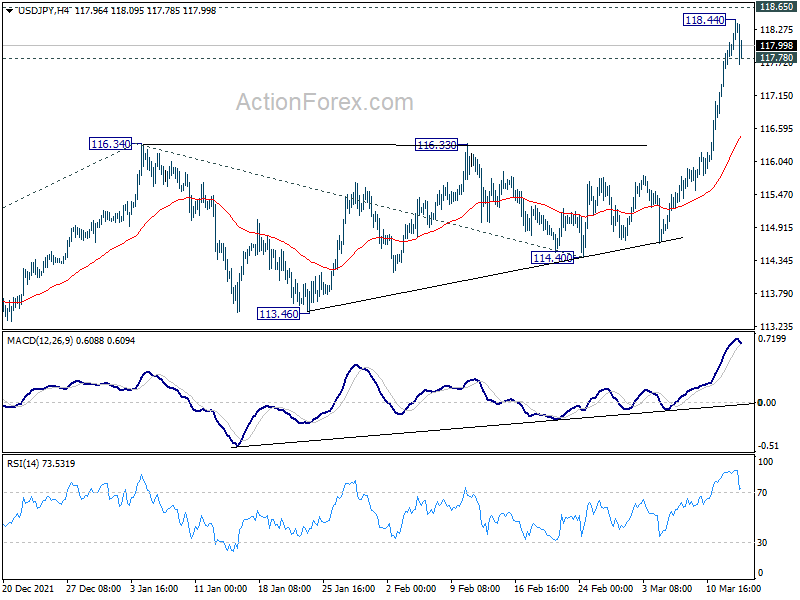

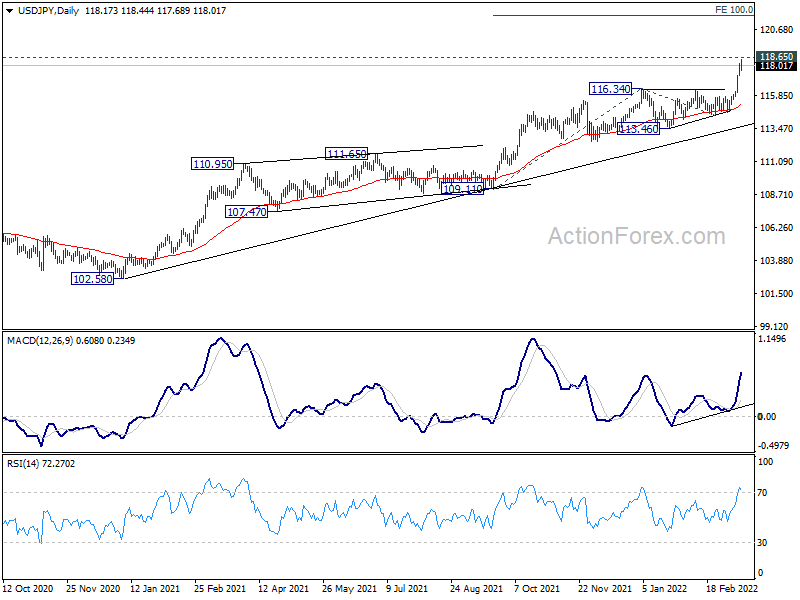

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 117.60; (P) 117.91; (R1) 118.52; More…

A temporary top is formed at 118.44, ahead of 118.65 long term resistance. Intraday bias is turned neutral for some consolidations first. Downside of retreat should be contained above 116.34 resistance turned support to bring another rally. On the upside, firm break of 118.65 will target 100% projection of 109.11 to 116.34 from 114.40 at 121.63.

{kind=link}

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 125.85 (2015 high) and raise the chance of long term up trend resumption. This will remain the favored case as long as 113.46 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 00:30 | AUD | House Price Index Q/Q Q4 | 4.70% | 3.90% | 5.00% | |

| 02:00 | CNY | Retail Sales Y/Y Feb | 6.70% | 3.00% | 1.70% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Feb | 12.20% | 5.00% | 4.90% | |

| 02:00 | CNY | Industrial Production Y/Y Feb | 7.50% | 3.90% | 4.30% | |

| 07:00 | GBP | Claimant Count Change Feb | -48.1K | 20.3K | -31.9K | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 3.90% | 4.00% | 4.10% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 4.80% | 4.60% | 4.30% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 3.80% | 3.70% | 3.70% | |

| 07:30 | CHF | Producer and Import Prices M/M Feb | 0.40% | 0.40% | 0.60% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Feb | 5.80% | 5.10% | 5.40% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Jan | 0.00% | 0.40% | 1.20% | 1.30% |

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | -39.3 | 10.3 | 54.3 | |

| 10:00 | EUR | Germany ZEW Current Situation Mar | -21.4 | -22.5 | -8.1 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | -38.7 | 49.3 | 48.6 | |

| 12:15 | CAD | Housing Starts Y/Y Feb | 247K | 235K | 231K | 230K |

| 12:30 | CAD | Manufacturing Sales M/M Jan | 0.60% | 1.30% | 0.70% | |

| 12:30 | USD | Empire State Manufacturing Index Mar | -11.8 | 7.3 | 3.1 | |

| 12:30 | USD | PPI M/M Feb | 0.80% | 1.00% | 1.00% | |

| 12:30 | USD | PPI Y/Y Feb | 10.00% | 10.00% | 9.70% | |

| 12:30 | USD | PPI Core M/M Feb | 0.20% | 0.60% | 0.80% | |

| 12:30 | USD | PPI Core Y/Y Feb | 8.40% | 8.10% | 8.30% |