The financial markets should have completed the first climax reaction to Russia to Ukraine. Both oil prices and gold spiked higher initially last week but pulled back since then. Stocks, in particular major European indexes, also staged a strong rebound after initial dive. Global benchmark treasury yields also rebounded.

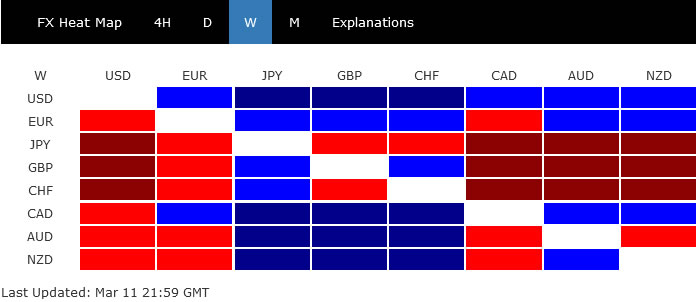

In the currency markets, Euro also attempted for a rebound, but was apparently capped. The common currency has indeed closed lower again Dollar and Canadian, which were the strongest two. The greenback was lifted by rise in yields, risk aversion, and expectation of Fed hike. Loonie was strongly support by stellar job data which reinforces BoC’s tightening. On the other hand, Yen closed as the weakest one on divergence in monetary policy with others. Swiss Franc was the second weakest, but Sterling was not too far away.

With upside breakout in USD/JPY, there is prospect of more rally in Dollar and selloff in Yen ahead. Meanwhile, European majors would likely stay under pressure, with a question on whether the tide of Swiss Franc is turning. Aussie and Loonie could be mixed overall until there is drastic moves in commodity prices again.

{kind=link}

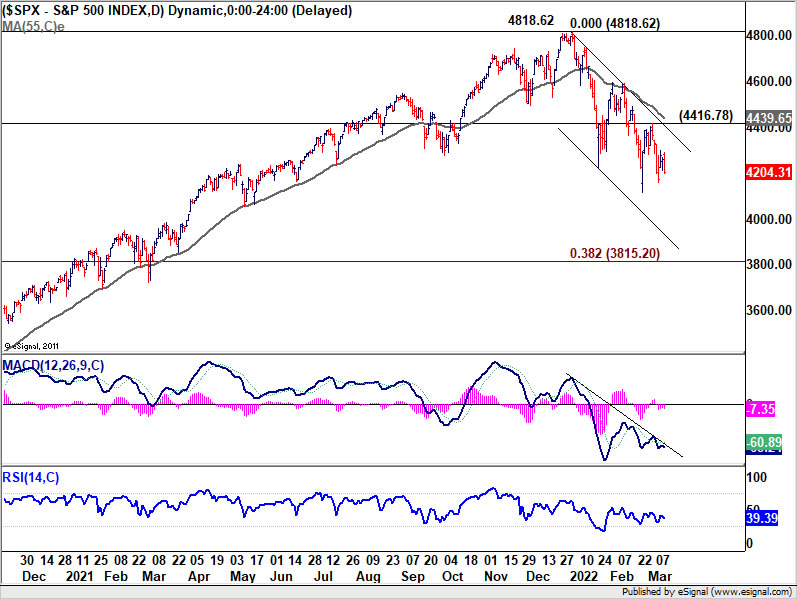

S&P 500 still in medium term correction, 10-year yield rebounded

S&P 500 gyrated lower last week but there was so far no pick-up in downside momentum. Still, as long as 4416.78 resistance holds, the medium term corrective fall from 4818.62 will more likely extend lower than not. Such decline would target 38.2% retracement of 2191.86 to 4818.62 at 3815.20 before completion.

Nevertheless, firm break of 4416.78 (corresponding level at 34719.07 in DOW and 13837.58 in NASDAQ), SPX should stage an interim rebound as the second leg of the corrective pattern from 4818.62. It should then be followed by another falling leg to completion the pattern.

{kind=link}

{kind=link}

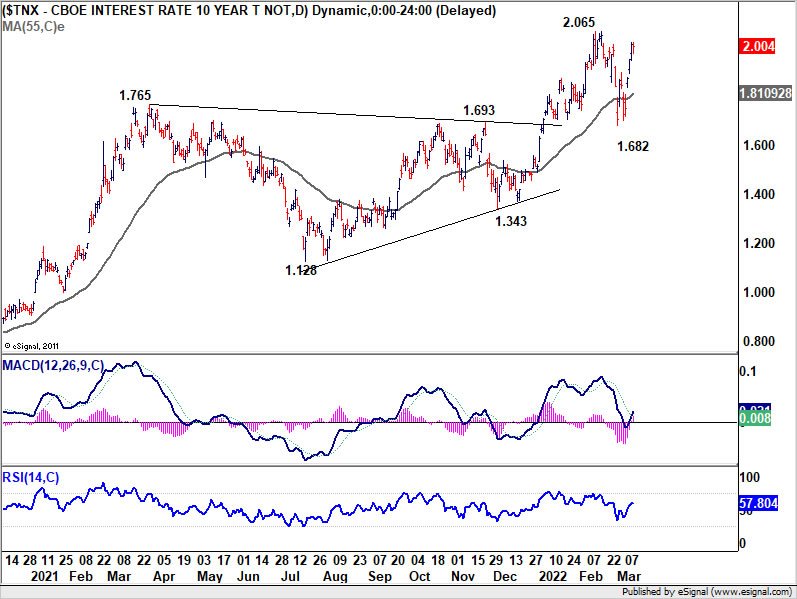

10-year yield’s strong rebound last week suggests that pull back from 2.065, while slightly deeper than expected, has completed at 1.682. The development keeps near term outlook bullish. 2.065 resistance will be in focus very soon and firm break there will resume larger up trend from 0.398.

Next target is cluster resistance level at 2.159/2.187 (61.8% retracement of 3.248 to 0.398 at 2.159, 61.8% projection of 0.398 to 1.765 to 1.343 at 2.187). Current upside momentum doesn’t warrant a strong break of this cluster level yet. This, strong resistance will likely be seen there to set the top of the range of a medium term consolidation.

However, strong break of 2.159/2.187 will suggest some dramatic underlying development. In such case, coupled with extending risk aversion, the greenback could be given a strong, sustainable boost.

{kind=link}

{kind=link}

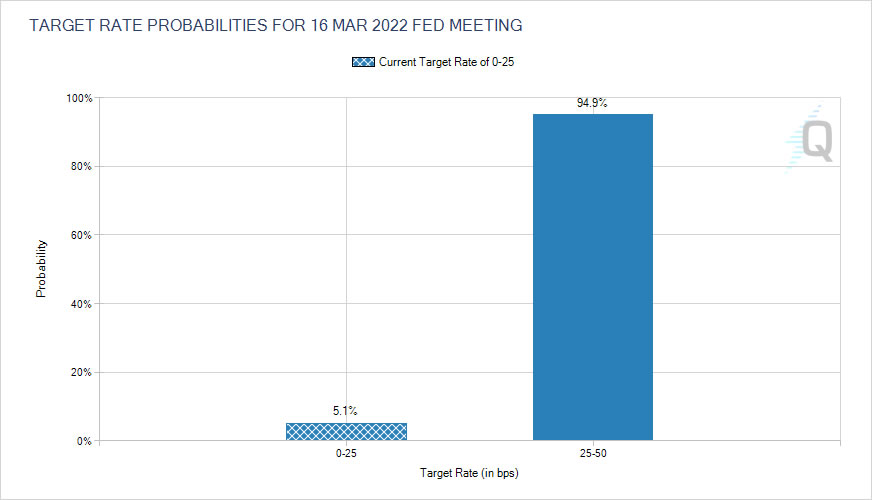

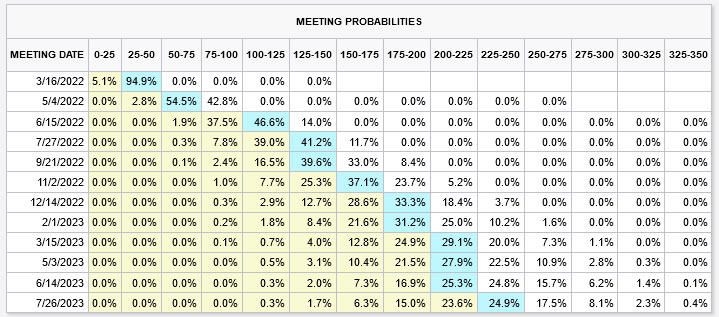

Fed to hike 25bps only, Dollar index maintains bullish tone

Talking about Dollar, the next focus will be FOMC rate decision. Traders are now pretty sure that there will only be a 25bps hike in federal funds rate to 0.25%-0.50% this week. Fed funds futures are pricing in 94.9% chance of that, with the 5.1% chance for Fed to be on hold.

{kind=link}

After that, there is 57.6% chance of rate ending up at 0.50%-0.75% in May, and 60.6% chance of rate ending up at 1.00-1.25% in June. That is, markets are expecting to stay cautious with another 25bps hike in May, and catch up with 50bps hike in June. But of course the pricing could change notably after the new economic projections accompanying this week’s rate decision.

{kind=link}

Dollar index retreated after hitting 99.41 last week, but stayed well above 96.93 resistance turned support. Near term outlook remains clearly bullish for further rally. In a less long term bullish case, DXY’s rise from 89.20 is just a leg inside the sideway pattern from 103.82 (2017 high). Further rise should be seen to test 102.99 resistance before topping.

Overall, the power of the next rally through 99.41 would depend on a couple of inter-related factors, including risk sentiment, treasury yields, and Fed’s new economic projections.

{kind=link}

{kind=link}

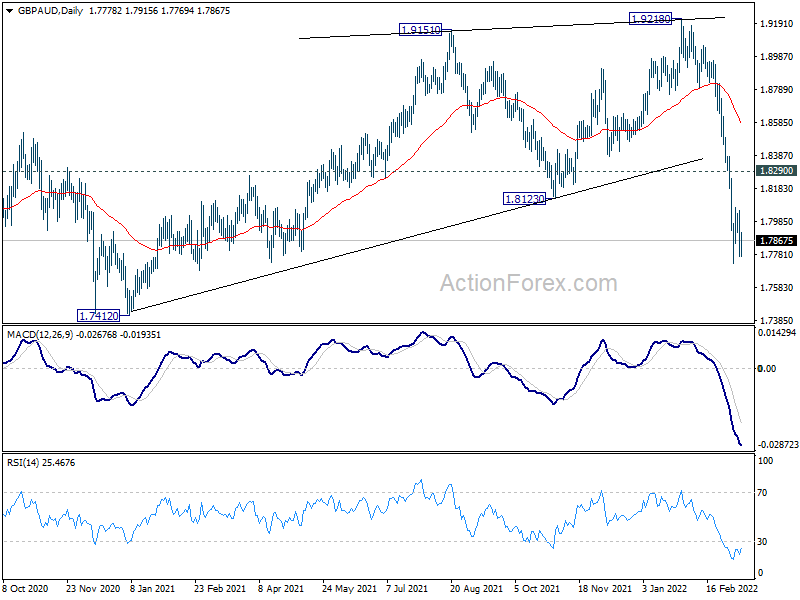

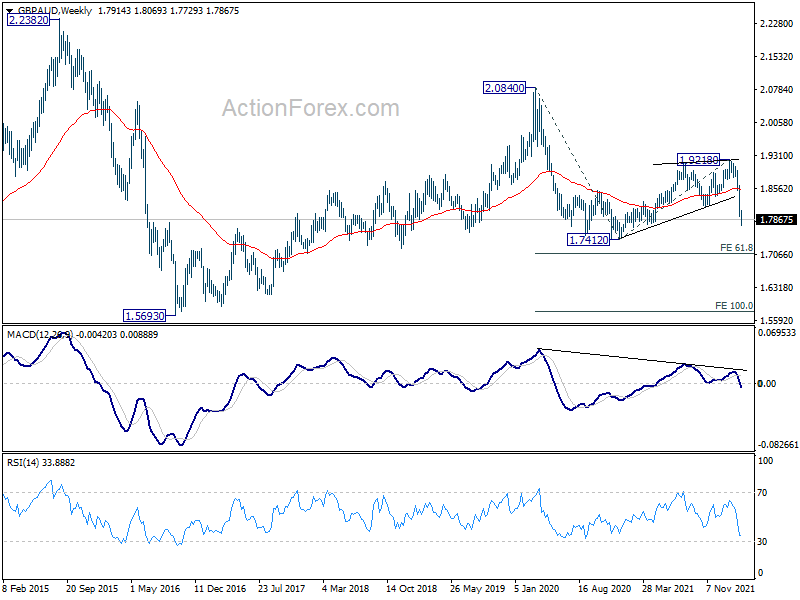

GBP/AUD staying bearish despite expectation of BoE hike

Talking about rate hikes, BoE is also expected to raise interest rate again by 25bps to 0.75% this week. However, such expectation, together with recent strong data, provided little boost to Sterling. The Pound is apparently still weighed heavily down by uncertainty over Russia invasion of Ukraine.

GBP/AUD turned sideway last week after hitting 1.7729 but recovery had be very weak. Overall outlook remains bearish as long as 1.8290 minor resistance holds. Corrective rise from 1.7421 should have completed with three waves up to 1.9218. Fall from there is possibly resuming the whole down trend from 2.0840 (2020 high). Retest of 1.7412 should be seen next. Firm break there will target 61.8% projection of 2.0840 to 1.7412 from 1.9218 at 1.7099.

{kind=link}

{kind=link}

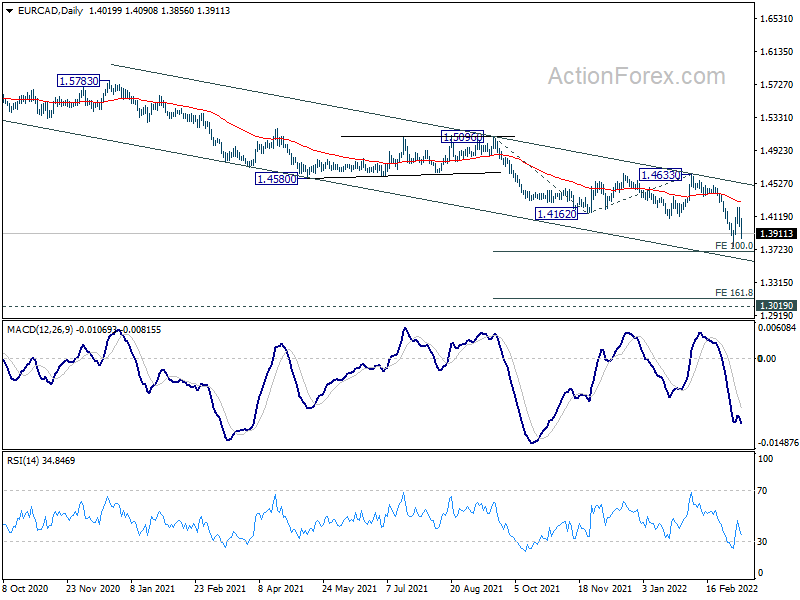

EUR/CAD staying bearish with CAD supported by strong job data

Euro attempted a rebound last week but quickly faltered despite a hawkish shift in ECB. On the other hand, Canadian Dollar was boosted by stellar job report which solidify more tightening from BoC ahead.

While EUR/CAD’s rebound from 1.3760 was stronger than expected, there is no change in the near term bearish outlook. Focus could quickly be back on 61.8% projection of 1.5096 to 1.4162 from 1.4633 at 1.3699. Firm break there will pave the way to 161.8% projection at 1.3122, as part of the down trend from 1.5991. Nevertheless, break of last week’s high at 1.4231 will open up the case for strong rebound back to 1.4633 resistance

{kind=link}

{kind=link}

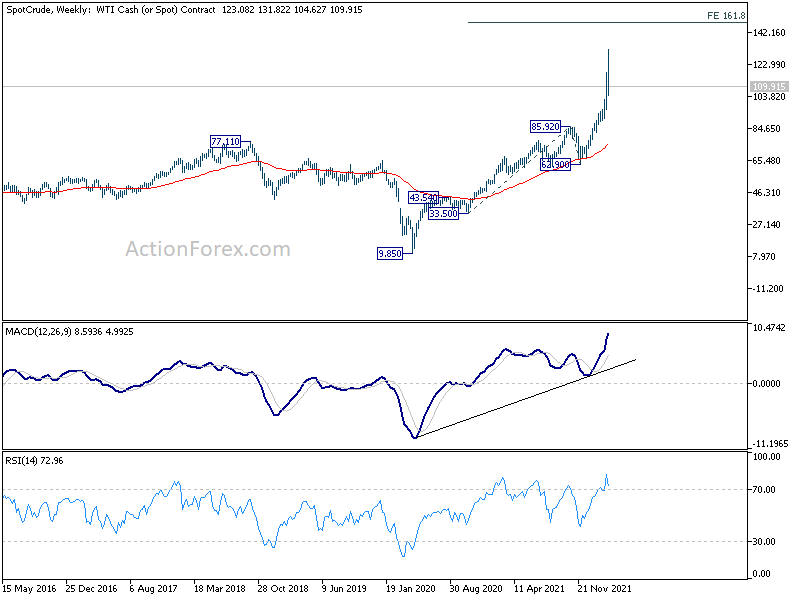

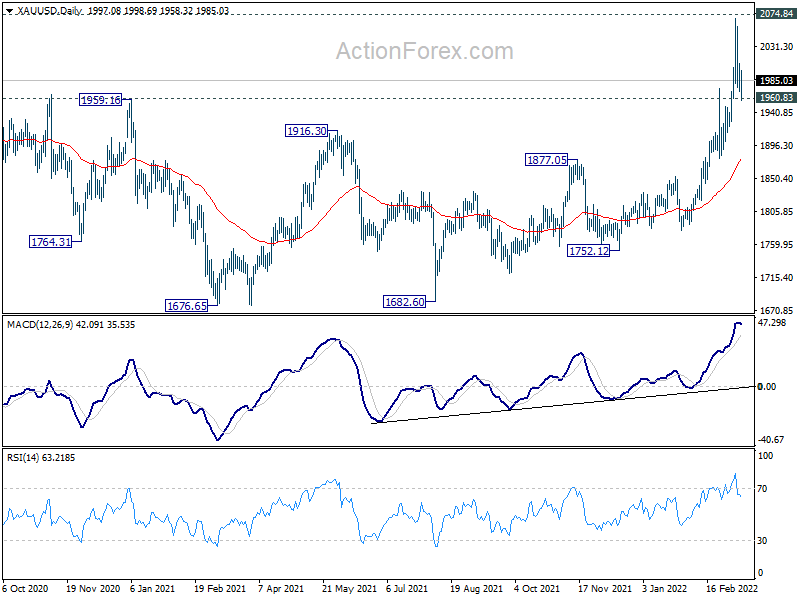

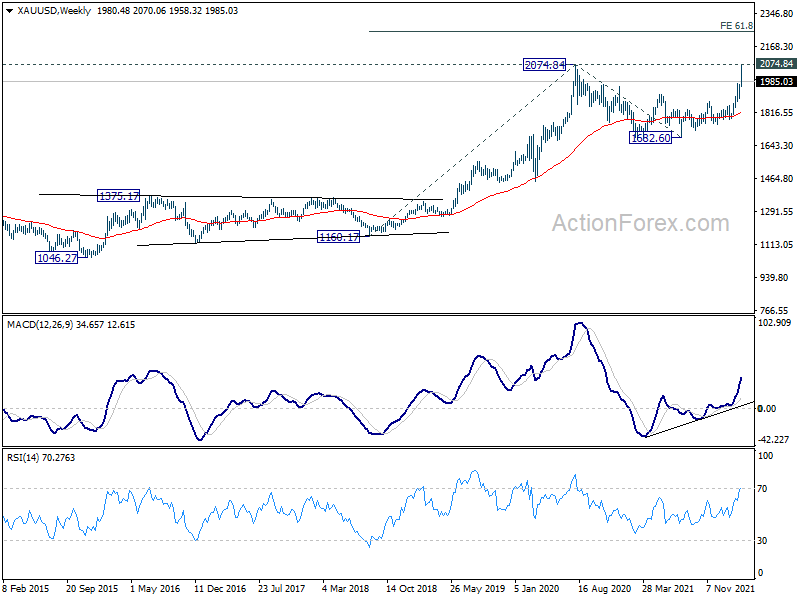

WTI oil and Gold in near term pull back after spikes

Finally, both WTI crude oil and Gold retreated notably after initial spikes last week. Such pull-backs are so far seen as knee-jerk reaction after passing initial buying climax. The stages for sizeable correction are not set yet.

As for WTI, as long 38.2% retracement of 62.90 to 131.82 at 105.49 holds, up trend should resume sooner rather than later to 161.8% projection of 33.50 to 85.92 from 62.90 at 147.71, which is close to record high made in 2008. But sustained break of 105.49 will formally start a medium term correction targeting 55 day EMA (now at 93.95).

{kind=link}

{kind=link}

As for Gold, as long as 1960.83 minor support holds, further rally is expected. Decisive break of 2074.84 will resume long term up trend to 61.8% projection of 1160.17 to 2074.84 from 1682.60 at 2247.86. However, sustained break of 1960.83 will indicate rejection by 2074.85, and bring deeper pull back to 55 day EMA (now at 1877.76) and possibly below.

{kind=link}

{kind=link}

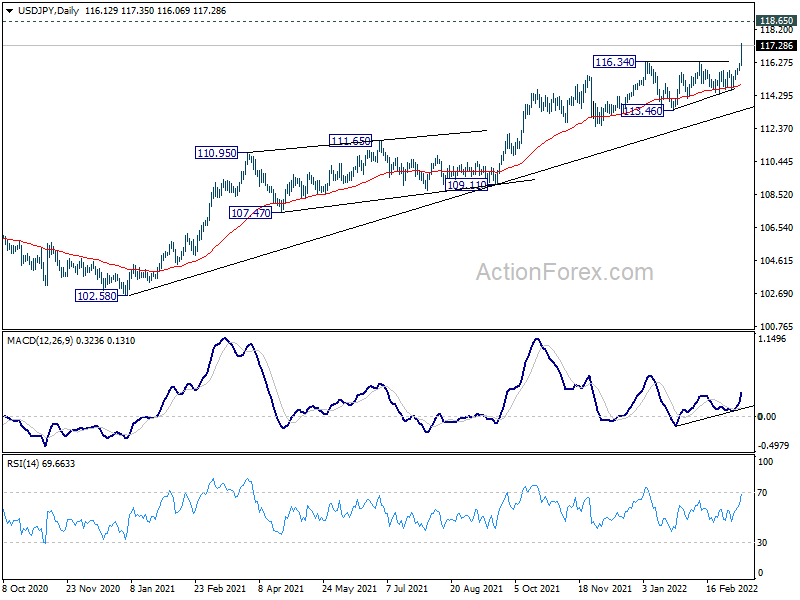

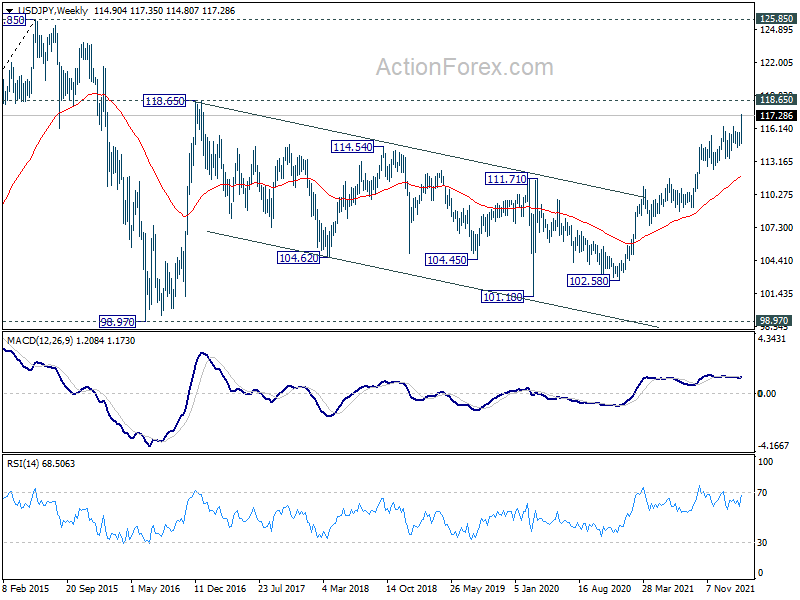

USD/JPY Weekly Outlook

USD/JPY’s strong break of 116.34 resistance confirms resumption of whole up trend from 102.58. Initial bias stays on the upside this week. Next target is 118.65 long term resistance. On the downside, below 116.73 minor support will turn intraday bias neutral and bring consolidation first, before staging another rally.

{kind=link}

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. This will remain the favored case as long as 113.46 support holds.

{kind=link}

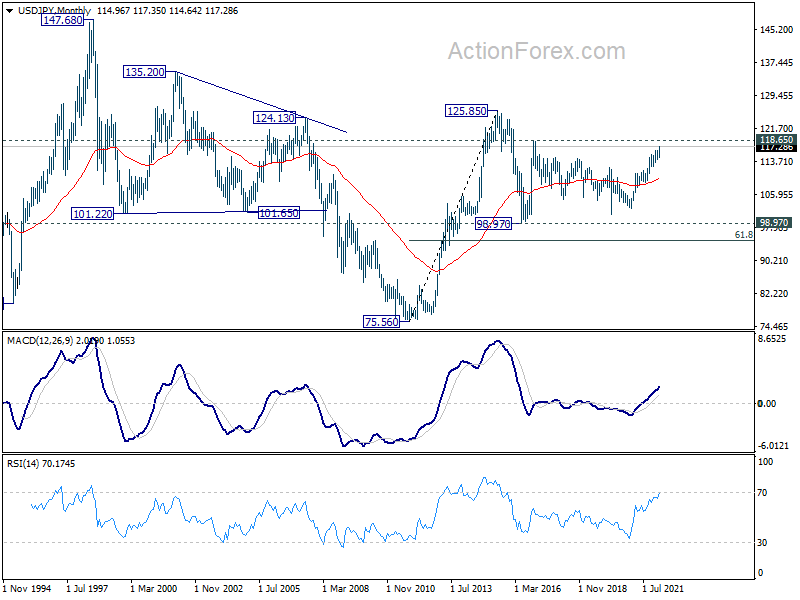

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 (2015 high) is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective pattern which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

{kind=link}

{kind=link}