Entering into US session, markets are starting to digest the steep moves made earlier today. Euro is paring some losses and it’s indeed trading in black against Sterling, Swiss and Yen at the time of writing. Swiss Franc has apparently turned weaker, probably on concern that SNB could intervene any time market stabilizes. Nevertheless, Aussie remains the strongest one, leading other commodity currencies firm, while Dollar is mixed. In other markets, Gold is considered failing to sustain above 2000 handle for now, and turned into consolidations first. WTI crude oil is also retreating back below 120 handle.

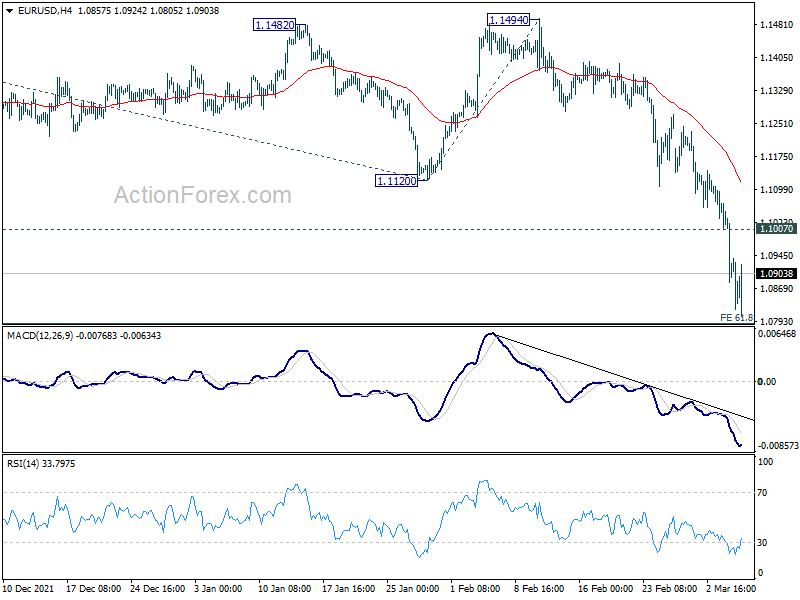

Technically, we’ll keep an eye on 1.1007 minor resistance in EUR/USD, 126.91 minor resistance in EUR/JPY and 1.0115 minor resistance in EUR/CHF. Break of these levels should indicate that selling climax in Euro has passed for the moment. That is, Euro would likely turn into consolidations first, even though near term bottoming might still be far away.

In Europe, at the time of writing, FTSE is down -0.23%. DAX is down -1.36%. CAC is down -1.14%. Germany 10-year yield is up 0.054 at -0.014. Earlier in Asia, Nikkei dropped -2.94%. Hong Kong HSI dropped -3.87%. China Shanghai SSE dropped -2.17%. Singapore Strait Times dropped -1.21%. Japan 10-year JGB yield dropped -0.0053 at 0.147.

Eurozone Sentix dropped to -7, worst fall in expectations than pandemic

Eurozone Sentix Investor Confidence dropped sharply from 16.6 to -7.0 in March, well below expectation of 5.1. That;s also the lowest level since November 2020. Current Situation index dropped from 19.3 to 7.8, lowest since May 2021. Expectations index dropped from 14.0 to -20.8, lowest since August 2012.

Sentix said: “The first economic indication after the Russian invasion of Ukraine has it all: The economy in Euroland collapses dramatically in the month of March! The assessment of the economic situation decreased by 11.5 points and the expectations decreased by 34.75 points, which is more than ever before in the history of sentix. Even the Corona pandemic or the banking crisis had not led to such a sharp drop in the future outlook!”

From Germany, retail sales rose 2.0% mom in January, versus expectation of 1.9% mom. Factory orders rose 1.8% mom, versus expectation of 1.0% mom.

Swiss foreign currency reserves dropped to CHF 938B in February.

Australia AiG services rose to 60 in Feb, grew strongly

Australia AiG Performance of Services Index rose 3.8 pts to 60.0 in February. Looking at some details, sales rose 9.7 pts to 68.6. Employment dropped -2.0 to 54.7. New orders rose 3.2 to 61.1. Supplier deliveries rose 7.6 to 59.0. Input prices dropped -0.1 to 66.0. Selling prices dropped -1.9 to 60.3. Average wages dropped -1.0 to 55.9.

Innes Willox, Chief Executive of Ai Group, said: “Australian service sector businesses grew strongly in February with sales, employment and new orders all adding to the gains in the December-January period. Prices of inputs and wages were up but not as dramatically as in the manufacturing and construction sectors. Selling prices remained at a level that suggests a capacity to recover a proportion of cost increases in the market.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0855; (P) 1.0962; (R1) 1.1037; More…

Intraday bias in EUR?USD stays on the downside at this point. Sustained break of 61.8% projection of 1.2265 to 1.1120 from 1.1494 at 1.0786 will pave they way to 100% projection at 1.0349 next. On the upside, above 1.1007 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

{kind=link}

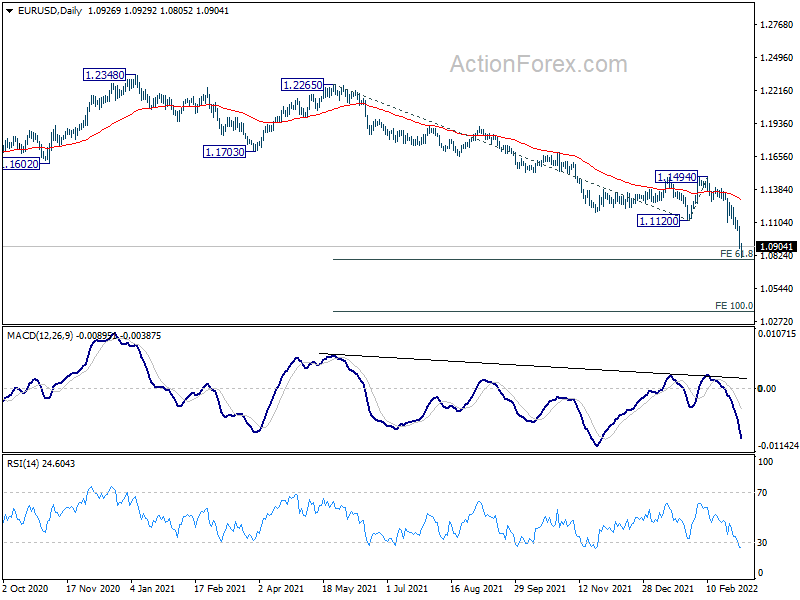

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extend range trading first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Feb | 60 | 56.2 | ||

| 02:00 | CNY | Trade Balance (USD) Jan | 115.95B | 95.5B | 94.5B | |

| 02:00 | CNY | Exports (USD) Y/Y Jan | 16.30% | 15.00% | 20.90% | |

| 02:00 | CNY | Imports (USD) Y/Y Jan | 15.50% | 16.50% | 19.50% | |

| 02:00 | CNY | Trade Balance (CNY) Jan | 738.8B | 450B | 605B | |

| 02:00 | CNY | Exports (CNY) Y/Y Jan | 13.60% | 19.10% | 17.30% | |

| 02:00 | CNY | Imports (CNY) Y/Y Jan | 12.90% | 21.30% | 16.00% | |

| 06:45 | CHF | Unemployment Rate Feb | 2.20% | 2.30% | 2.30% | |

| 07:00 | EUR | Germany Retail Sales M/M Jan | 2.00% | 1.90% | -5.50% | |

| 07:00 | EUR | Germany Factory Orders M/M Jan | 1.80% | 1.00% | 2.80% | |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Feb | 938B | 947B | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | -7 | 5.1 | 16.6 |