The markets are overall mixed today, as investors are holding their breath, awaiting confirmation on whether Russia is going to invade Ukraine, or not. Gold jumps notably and is now eyeing 1900 handle on nervous sentiment. In the currency markets, Yen is currently the stronger one, followed by Kiwi and then Sterling. Canadian Dollar is the weakest, followed by Dollar. There isn’t a very clear direction yet.

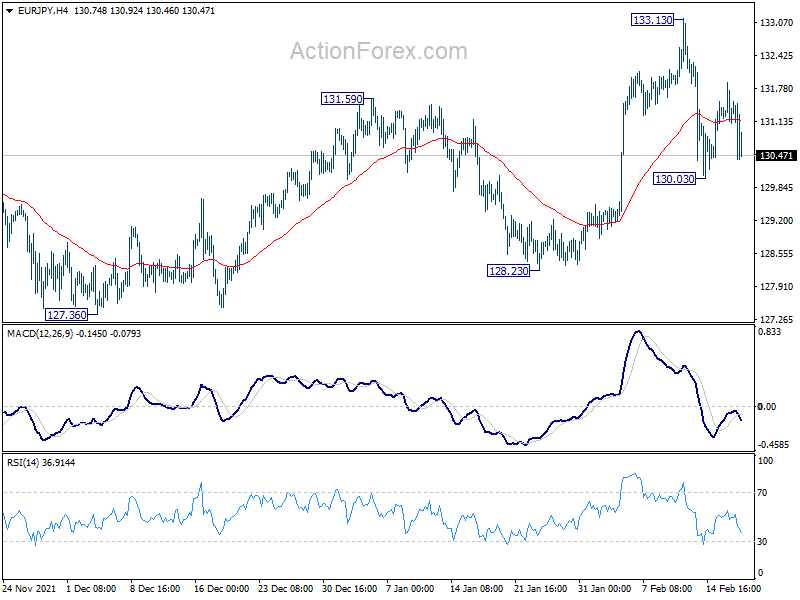

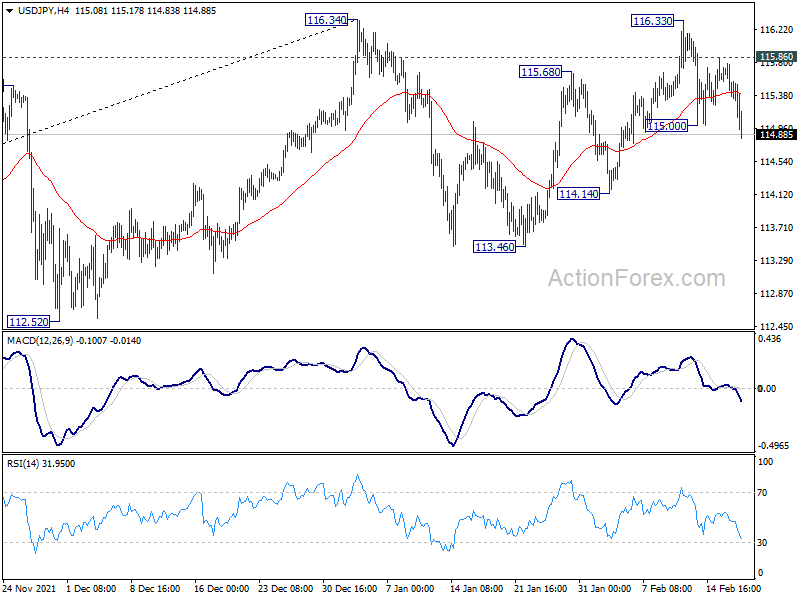

Technically, USD/JPY’s break of 115.00 temporary low is in line with the view that fall from 116.33 is still in progress, as the third leg of the corrective pattern from 116.34. Attention will be on whether EUR/JPY would follow by breaking through 130.03, and whether GBP/JPY would break 155.11.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.57%. DAX is down -0.19%. CAC is up 0.12%. Germany 10-year yield is down -0.0303 at 0.247. Earlier in Asia, Nikkei dropped -0.83%. Hong Kong HSI rose 0.30%. China Shanghai SSE rose 0.06%. Singapore Strait Times rose 0.07%. Japan 10-year JGB yield rose 0.0026 to 0.224.

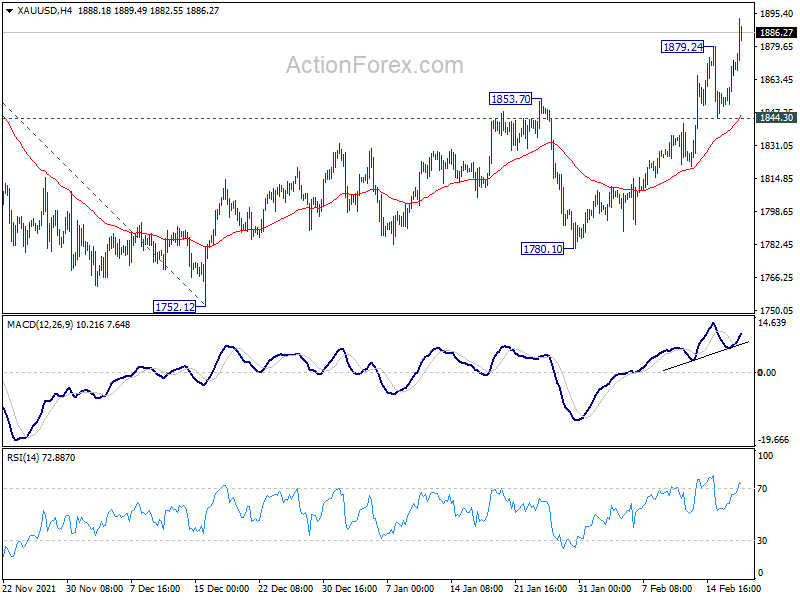

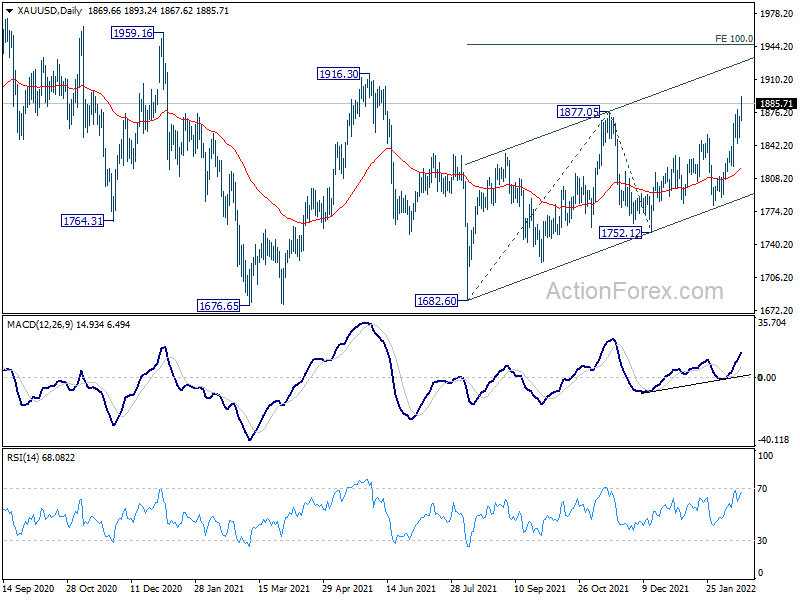

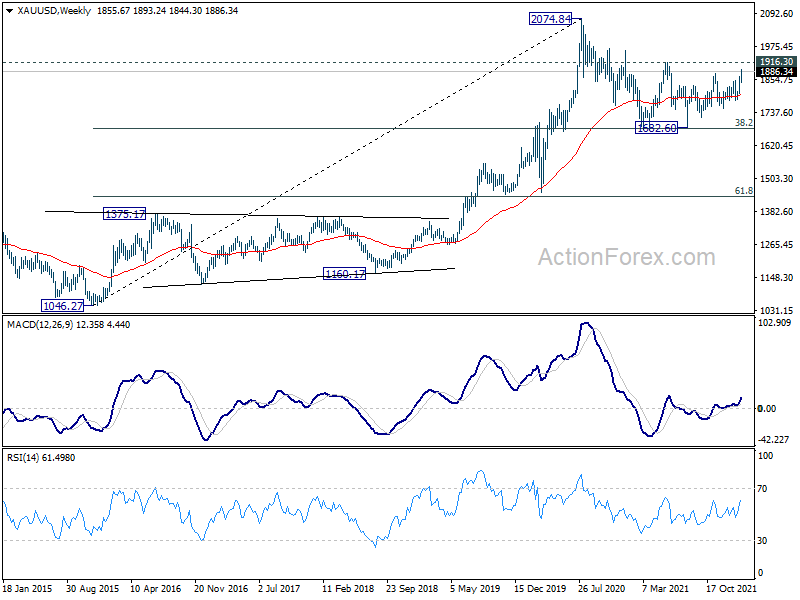

Gold to press 1900 as rally resumes

Gold’s rally resumes today by taking out 1879.24 temporary top and hits as high as 1893.24 so far, just shy of 1900 handle. Further rally is now expected as long as 1844.30 support holds. Current rise is seen as part of the whole rally from 1682.60. Gold should break through 1916.30 resistance to 100% projection of 1682.60 to 1877.05 from 1752.12 at 1946.57.

{kind=link}

{kind=link}

Meanwhile, it should be noted that firstly, firm break of 1916.30 should confirm completion of the correction from 2074.84 at at 1682.60. Secondly, further break of 1946.57 will suggest medium term up side acceleration. In this case, retest of 2074.84 high should be quickly within reach.

{kind=link}

US initial jobless claims rose to 248k, above expectation

US initial jobless claims rose 23k to 248k in the week ending February 12, above expectation of 219k. Four-week moving average of initial claims dropped -11k to 243k. Continuing claims dropped -25k to 1593k in the week ending February 5. Four-week moving average of continuing claims dropped -8k to 1626k.

Housing starts dropped to 1.64m annualized rate in January. Building permits rose to 1.90m. Philadelphia Fed manufacturing survey dropped to 16 in February, below expectation of 21.

Japan monthly trade deficit at 8-yr high in Jan, as imports surged to record

Japan exports rose 9.6% yoy to JPY 6332B in January. Imports surged 39.6% yoy to record JPY 8523B. Trade balance came in as JPY -2191B deficit, largest single month deficit since January 2014.

Exports to China dropped -5.4% yoy, first contraction in 19 months. Imports from China rose 23.7% yoy, highest in four months. Exports to US rose 11.5% yoy.

In seasonally adjusted term, exports rose 0.1% mom to JPY 7355B. Imports rose 4.9% mom to JPY 8287B. Trade balance was at JPY -933B deficit.

Australia employment grew 12.9k driven by part-time jobs, hours worked fell

Australia employment grew 12.9k in January, better than expectation of 0k. Full-time jobs dropped -17k but part-time jobs rose 30k.

Unemployment rate was unchanged at 4.2%, but participation rate rose 0.1% to 66.2%. Monthly hours worked, however, dropped -8.8% mom.

Bjorn Jarvis, head of labour statistics at the ABS, “While we again saw higher than usual numbers of people taking annual leave – even more so than last year – the 8.8 per cent fall in hours worked in January 2022 also reflected much higher than usual numbers of people on sick leave.”

“As with earlier rapid changes in the labour market during the pandemic, hours continue to be much more affected than employment. This reflects people working reduced or no hours, without necessarily losing their jobs.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 115.28; (P) 115.53; (R1) 115.71; More…

Intraday bias in USD/JPY is back on the downside with break of 115.00 temporary low. Fall from 116.33 is seen as the third leg of the corrective pattern from 116.34. Deeper decline should be seen to 114.14 support, and then 113.46. On the upside, however, break of 115.86 will turn bias back to the upside for 116.34 resistance instead.

{kind=link}

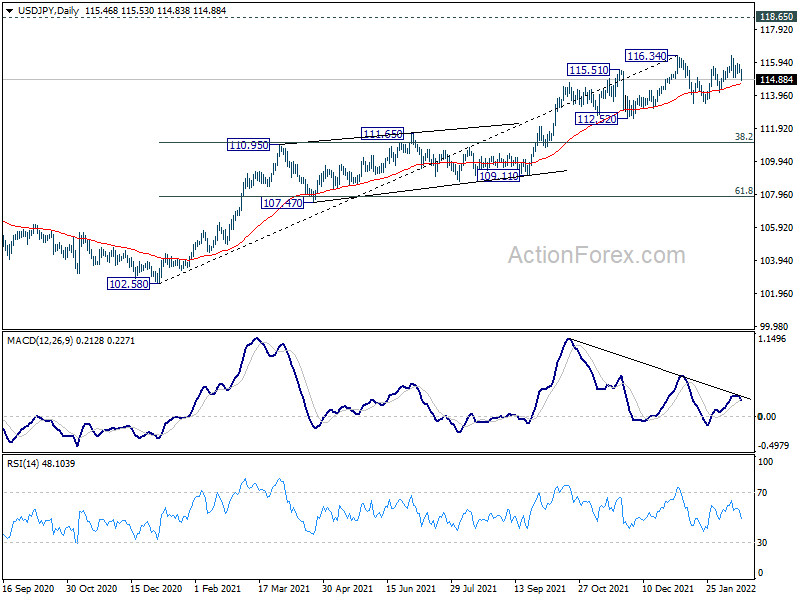

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. This will remain the favored case as long as 55 week EMA (now at 111.21) holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Jan | -0.93T | -0.46T | -0.44T | -0.55T |

| 23:50 | JPY | Machinery Orders M/M Dec | 3.60% | -1.80% | 3.40% | |

| 00:30 | AUD | Employment Change Jan | 12.9K | 0.0K | 64.8K | |

| 00:30 | AUD | Unemployment Rate Jan | 4.20% | 4.20% | 4.20% | |

| 07:00 | CHF | Trade Balance (CHF) Jan | 3.18B | 4.23B | 3.69B | 3.54B |

| 13:30 | USD | Housing Starts Jan | 1.64M | 1.70M | 1.70M | |

| 13:30 | USD | Building Permits Jan | 1.90M | 1.79M | 1.87M | 1.89M |

| 13:30 | USD | Initial Jobless Claims (Feb 11) | 248K | 219K | 223K | 225K |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Feb | 16 | 21 | 23.2 | |

| 15:30 | USD | Natural Gas Storage | -203B | -222B |