Dollar rebounds broadly in early US session after stronger than expected CPI data. Treasury yields also surged with 10-year yield marching higher. 2% level for 10-year yield is getting closer. Stocks on the other hand, take some beating on concerns of a more aggressive Fed. For now, selloff is concentrating on Yen and Swiss Franc. But Europeans and commodity currencies are also weak.

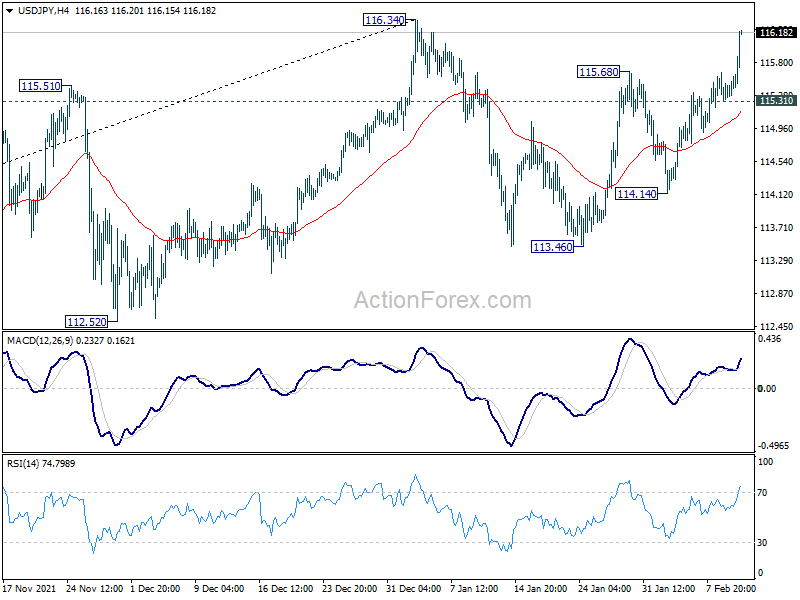

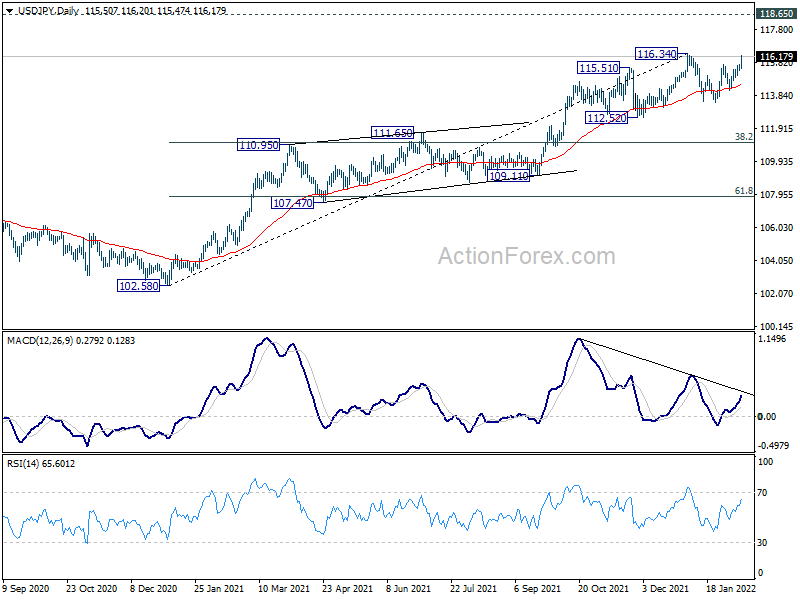

Technically, a major focus is on whether USD/JPY would break through 116.34 high to resume the medium term up trend. At the same time, attention will also be on whether EUR/JPY and GBP/JPY are heading to 134.11 and 158.19 resistance levels respectively. Break of all these levels could add extra fuel to the rally in USD/JPY.

In Europe, at the time of writing, FTSE is up 0.06%. DAX is flat. CAC is down -0.45%. Germany 10-year yield is up 0.038 at 0.249. Earlier in Asia, Nikkei rose 0.42%. Hong Kong HSI rose 0.38%. China Shanghai SSE rose 0.17%. Singapore Strait Times rose 0.23%. Japan 10-year JGB yield closed up 0.0215 at 0.230.

US CPI rose to 7.5% yoy, core CPI to 6.0% yoy, highest since 1982

Over the month, US CPI rose 0.6% mom in January, above expectation of 0.4% mom. CPI core rose 0.6% mom, above expectation of 0.5% mom.

Over the 12-month period, CPI accelerated from 7.0% yoy to 7.5% yoy, above expectation of 7.3% yoy. That’s the highest level since February 1982. CPI core jumped from 5.5% yoy to 6.0% yoy, above expectation of 5.9% yoy. That’s the highest level since August 1982.

Energy index rose 27.0% yoy while food index rose 7.0% yoy.

US initial jobless claims dropped -15k to 223k

US initial jobless claims dropped -15k to 223k in the week ending February 5, better than expectation of 230k. Four-week moving average of initial claims dropped -2k to 253k.

Continuing claims was unchanged at 1621k in the week ending January 29. Four-week moving average of continuing claims rose 16.5k to 1645k.

ECB Lane: Hold-steady approach reinforced if bottlenecks are primarily external in nature

ECB Chief Economist Philip Lane said in a blog post, “in terms of inflation dynamics, the relative price dislocations associated with bottlenecks are intrinsically short-term rather than permanent in nature.” Further, “initial increases in relative prices of categories that experienced high demand and/or low supply can be expected to level off or even reverse.”

Additionally, ” it should be acknowledged that bottlenecks are not the only factor influencing the overall inflation environment, with a comprehensive monetary policy assessment taking into account a wide range of factors.”

“Since bottlenecks will eventually be resolved, price pressures should abate and inflation return to its trend without a need for a significant adjustment in monetary policy.”

“The logic underpinning a hold-steady approach to monetary policy is reinforced if the bottlenecks are primarily external in nature, caused by global disruptions in supply or a surge in global demand”.

ECB de Guindos: Inflation to decline in the course of this year

ECB Vice President Luis de Guindos said in a speech, “inflation is likely to remain elevated for longer than previously expected, but to decline in the course of this year.”

“That is the central case, but there are upside risks to that outlook,” he added. “Inflation could turn out to be higher if price pressures feed through into higher-than-anticipated wage rises, or if the economy returns to full capacity more quickly than foreseen.

“Some other central banks have either already raised rates or indicated that they will soon do so,” he said. “In making comparisons, it’s worth remembering that the euro area is at a different stage of the economic cycle, just as it was when the pandemic started. So it’s natural that central banks around the globe won’t necessarily start raising rates at the same time.”

EU downgrades 2022 Eurozone GDP forecasts, upgrades inflation

In the Winter 2022 interim forecasts, EU downgrades 2022 Eurozone GDP growth forecasts from 4.3% to 4.0%. Nevertheless, 2023 GDP growth forecast was upgraded from 2.4% to 2.7%. Eurozone 2022 HICP inflation forecast was raised from 2.2% to 3.5%. 2023 HICP inflation forecast was also upgraded from 1.4% to 1.7%.

Valdis Dombrovskis, Executive Vice-President for an Economy that Works for People said: “The EU economy has now regained all the ground it lost during the height of the crisis, thanks to successful vaccination campaigns and coordinated economic policy support. Unemployment has reached a record low. These are major achievements. As the pandemic is still ongoing, our immediate challenge is to keep the recovery well on track. The significant rise in inflation and energy prices, along with supply chain and labour market bottlenecks, are holding back growth. Looking ahead, however, we expect to switch back into high gear later this year as some of these bottlenecks ease. The EU’s fundamentals remain strong and will be boosted further as countries start to put their Recovery and Resilience Plans into full effect.”

Paolo Gentiloni, Commissioner for Economy said: “Multiple headwinds have chilled Europe’s economy this winter: the swift spread of Omicron, a further rise in inflation driven by soaring energy prices and persistent supply-chain disruptions. With these headwinds expected to fade progressively, we project growth to pick up speed again already this spring. Price pressures are likely to remain strong until the summer, after which inflation is projected to decline as growth in energy prices moderates and supply bottlenecks ease. However, uncertainty and risks remain high.”

BoJ Kuroda: No chance to debate stimulus exit in my term

BoJ Governor Haruhiko Kuroda was quoted by Mainichi newspaper saying that “as long as our current price projection lives, there’s no chance we will debate” stimulus exit before his term ends in April 2023. “We’re not engaging in any debate of an exit. Doing so is inappropriate given Japan’s price developments,” he added.

“Japan’s economic recovery is slower than that of the United States and European countries, and (consumer) inflation is just 0.5%,” Kuroda said. “As such, there’s no need to scale back monetary stimulus or shift toward policy tightening. Doing so is unlikely,”

The change of consumer inflation accelerating sharply was “very small” and “the key would be wage growth”.

Japan CGPI rose 8.6% yoy in Jan, index at highest since 1985

Japan corporate goods price index rose 8.6% yoy in January, slowed slightly from December’s 8.7% yoy, but beat expectation of 8.2% yoy. At 109.5, the index was at the highest level since September 1985.

Export prices jumped 12.5% yoy on Yen basis, 6.6% yoy on contract currency basis. Import prices surged a massive 37.5% yoy on Yen basis, and 28.0% yoy on contract currency basis.

However, consumer prices remained sluggish, with national CPI core at 0.5% yoy in December, which some economists expected to slow to 0.3% yoy in January.

BoJ officials, including Governor Haruhiko Kuroda, have indicated that it would be hard to see consumer inflation to sustainably reach 2% target without wages rise.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 115.35; (P) 115.52; (R1) 115.71; More…

USD/JPY’s rebound from 113.46 resumed by breaking 115.68 resistance. Intraday bias is back on the for 116.34 high. Firm break there will resume larger up trend from 102.58. Next target is 118.65 long term resistance. On the downside, though, break of 115.31 minor support will extend the corrective pattern from 116.34 with another falling leg, and turn bias back to the downside for 114.14 support and possibly below.

{kind=link}

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. This will remain the favored case as long as 55 week EMA (now at 111.21) holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jan | 8.60% | 8.20% | 8.50% | 8.70% |

| 00:00 | AUD | Consumer Inflation Expectations Feb | 4.60% | 4.40% | ||

| 00:01 | GBP | RICS Housing Price Balance Jan | 74% | 72% | 69% | |

| 13:30 | USD | Initial Jobless Claims (Feb 4) | 223K | 230K | 238K | 239K |

| 13:30 | USD | CPI M/M Jan | 0.60% | 0.40% | 0.50% | 0.60% |

| 13:30 | USD | CPI Y/Y Jan | 7.50% | 7.30% | 7.00% | |

| 13:30 | USD | CPI Core M/M Jan | 0.60% | 0.50% | 0.60% | |

| 13:30 | USD | CPI Core Y/Y Jan | 6.00% | 5.90% | 5.50% |