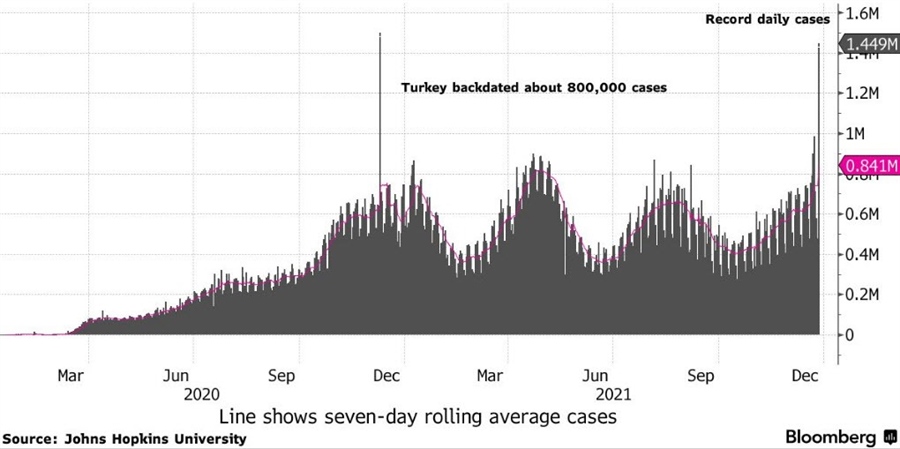

Global daily COVID-19 cases hit a new record on Monday, with more than 1.44 million infections recorded. This comes amid a surge in omicron infections and that is no surprise with the variant being the most transmissible one yet.

Of note, the 7-day rolling average of cases also jumped to roughly 841,000 – a 49% spike from a month ago.

Putting the numbers aside, the key question is does this all matter?

Well, not really. Once upon a time, the market may be spooked by the sheer magnitude of the figures. But not anymore.

The world has come to learn to live with COVID-19 and the fact that omicron appears to be less severe is allowing people, and investors too, to look past the variant’s high transmissibility.

A positive takeaway to the numbers above is that daily COVID-19 deaths has not seen as dramatic a surge as cases. Sure, there is a lag period but surely this is also a result of worldwide vaccinations.

The 7-day rolling average of deaths has stuck around 7,000 since October despite omicron’s emergence.

As such, this will be a key measure to watch in the weeks ahead (since there might be a lag) to reaffirm that omicron isn’t as fearful as anticipated when bursting onto the scene.

If anything, the market has already appeared to have made up its mind on that. The S&P 500 hit a fresh record high yesterday and in FX, AUD/JPY – a key risk barometer – has also erased its omicron losses.

Adding to that, 2-year Treasury yields jumped to its highest March 2020, nearing 0.75%.

Sure, thinner liquidity conditions are a considerable factor. So, we’ll see of any follow through next week onwards.

But for now, the numbers above are merely what they represent – just numbers. Unless of course when it comes to China, which remains the biggest wildcard to the global outlook next year at this point.