Market sentiment is generally positive in Asian session today. Australian and New Zealand Dollar are extending near term rebound. Other currencies are mixed, though. Canadian Dollar is paring some gains, after the non-eventful BoC rate decision. Sterling is trying to recover from yesterday’s selloff. Dollar and Yen are mixed.

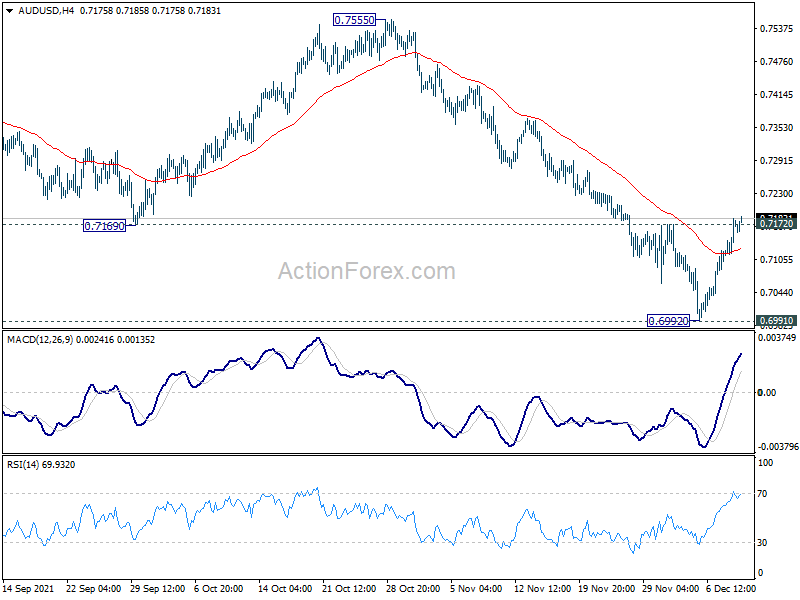

Technically, we’ll pay attention to both AUD/USD and USD/CAD today. AUD/USD is now trying to break through 0.7272 minor resistance. Sustained trading above there should confirm short term bottoming at 0.6992, just after drawing support from 0.6991 medium term support level. Stronger rise should at least be seen back to 55 day EMA (now at 0.7278, with prospect of bullish reversal.

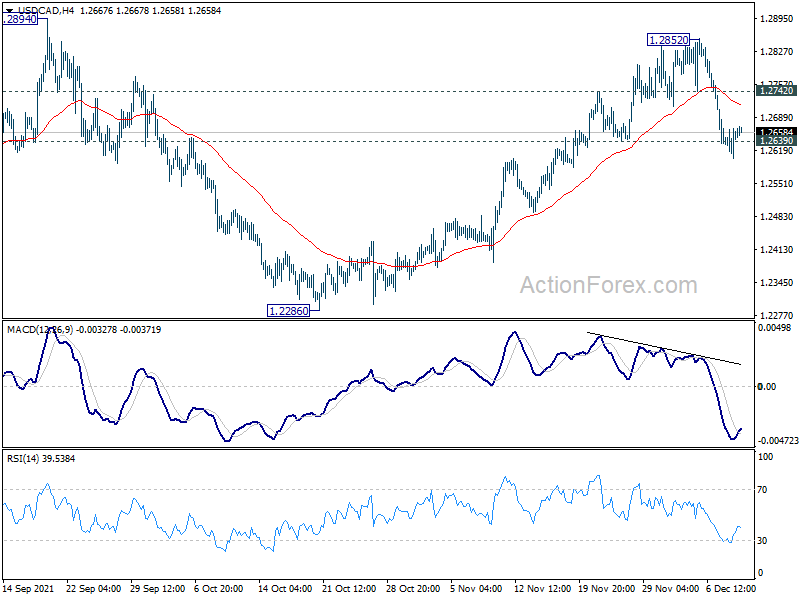

Meanwhile, sustained break of 1.2639 support in USD/CAD would argue that rebound from 1.2286 is completed at 1.2852, and deeper fall would be seen back to 1.2286 support. Both developments, if happen, could affirm that risk-on sentiment is fully back in the markets.

{kind=link}

In Asia, Nikkei closed down -0.47%. Hong Kong HSI is up 0.97%. China Shanghai SSE is up 1.24%. Singapore Strait Times is up 0.29%. Japan 10-year JGB yield is up 0.0034 at 0.053. Overnight, DOW rose 0.10%. S&P 500 rose 0.31%. NASDAQ rose 0.64%. 10-year yield rose 0.029 to 1.509.

Japan business conditions improved sharply as led by non-manufacturers

According to the Japanese government’s Business Outlook Survey, conditions for all large corporations improved notably from 3.3 to 9.6 in Q4. That’s the second quarter of positive reading. Conditions for large non-manufacturing jumped sharply from 1.5 to 10.4. Meanwhile, conditions for large manufacturers improved slightly from 7.0 to 7.9.

Conditions for mid-sized companies also rose sharply from 0.2 to 10.7. Conditions for small companies rose from -18.0 to -3.0, but stayed negative for the 31st successive quarter.

“With the severe situation caused by the impact of virus infections gradually easing, the survey results showed that (the economy) has been picking up, although some fields remain weak,” a government official told reporters.

China CPI rose to 2.3% yoy in Nov, PPI slowed from 26-yr high to 12.6% yoy

China CPI accelerated to 2.3% yoy in November, up from 1.5% yoy, but below expectation of 2.5% yoy. That’s nonethless the highest level since August 2020. PPI slowed to 12.9% yoy, down from October’s 26-year high of 13.5% yoy, above expectation of 12.6%.

“As policies to stabilise prices and ensure supply have stepped up, the rapid surge in coal, metal and other energy and raw material prices has been initially contained, leading to a slowdown in PPI,” NBS senior statistician Dong Lijuan said in a statement accompanying the release.

New Zealand manufacturing sales dropped -2.2% qoq in Q3

New Zealand Manufacturing sales dropped -2.2% qoq, or NZD 674m in Q3. When adjusted for seasonal effects, 10 of the 13 manufacturing industries had lower volumes of sales in the quarter.

The largest industry movements were: metal products (-17%), petroleum and coal products (-13%), transport equipment, machinery, and equipment (-8.8%).

“Despite sales falls in several construction related manufacturing industries, increased prices for meat and dairy cushioned the blow for total manufacturing values,” business statistics manager Evie Rolinson-Purchase said.

Looking ahead

Germany trade balance and Swiss SECO economic forecasts will be release in European session. Later in the day, US will release jobless claims and wholesale inventories.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7129; (P) 0.7157; (R1) 0.7198; More…

Immediate focus is now on 0.7172 resistance in AUD/USD. Sustained break there should confirm short term bottoming at 0.6992. More importantly, whole corrective fall from 0.8006 might be finished too after defending 0.6991 key structural support. Stronger rise should then be seen to 55 day EMA (now at 0.7275). Firm break there will target 0.7555 resistance to confirm this bullish case. On the downside, however, firm break of 0.6991 will carry larger bearish implication and extend the down trend from 0.8006.

{kind=link}

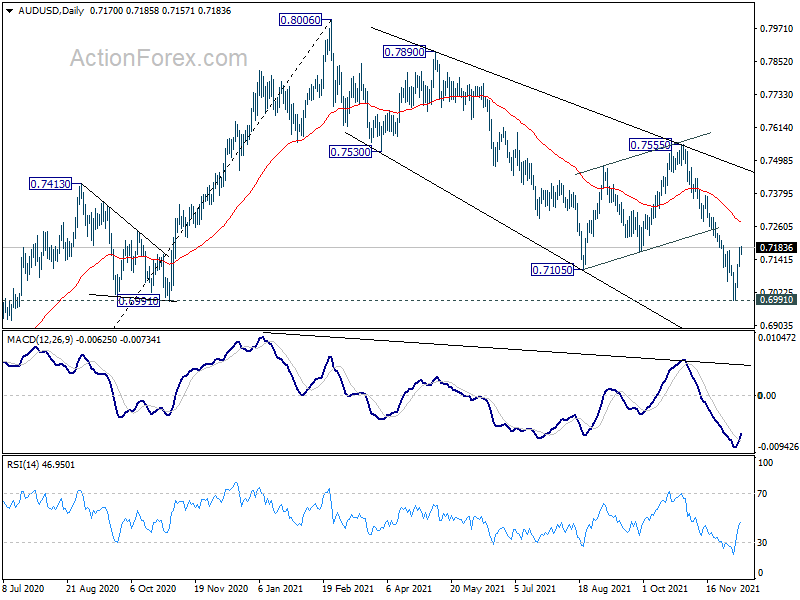

In the bigger picture, focus stays on 0.6991 key support level. Strong rebound from there will argue that up trend from 0.5506 is still intact for another rise through 0.8006 at a later stage. However, sustained break of 0.6991 will argue that the up trend is over, after rejection by 0.8135 long term resistance. Deeper decline would then be seen back to 61.8% retracement of 0.5506 to 0.8006 at 0.6461.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q3 | -2.20% | 4.20% | 3.90% | 3.70% |

| 23:50 | JPY | BSI Large Manufacturing Q3 | 7.9 | 5.3 | 7 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 4.00% | 4.40% | 4.20% | |

| 0:01 | GBP | RICS Housing Price Balance Nov | 71% | 72% | 70% | 71% |

| 0:30 | AUD | RBA Bulletin Q3 | ||||

| 1:30 | CNY | CPI Y/Y Nov | 2.30% | 2.50% | 1.50% | |

| 1:30 | CNY | PPI Y/Y Nov | 12.90% | 12.60% | 13.50% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Nov | 64.0% | 81.50% | ||

| 7:00 | EUR | Germany Trade Balance (EUR)Oct | 12.9B | 13.2B | ||

| 8:00 | CHF | SECO Economic Forecasts | ||||

| 13:30 | USD | Initial Jobless Claims (Dec 3) | 225K | 222K | ||

| 15:00 | USD | Wholesale Inventories Oct F | 2.20% | 2.20% | ||

| 15:30 | USD | Natural Gas Storage | -59B |